")

30-Year Mortgage Rates Today 2026 (Full Expert Guide)

Opening Summary

30-year mortgage rates today in 2026 are influenced by inflation, central bank policies, and global economic conditions, generally remaining at moderate levels compared to previous years. These rates provide long-term payment stability over thirty years, making them a preferred choice for homeowners. Even small changes in interest rates can significantly impact total borrowing costs, which makes understanding these rates essential for long-term financial planning.

30-Year Mortgage Rates Today, 2026

Introduction

30-year mortgage rates today have become a key factor in financial decision-making for homebuyers, investors, and business owners in 2026. With the economy going through adjustments and inflation still playing a role, interest rates are no longer something people ignore. Borrowers now actively follow financial updates and policy changes because they understand how deeply these rates affect long-term affordability. For example, many people track updates from central banks through resources like the Bank of England official website, where monetary policy decisions directly explain why mortgage rates increase or decrease over time. This awareness has changed how people approach home buying, making research and comparison a necessary step instead of an optional one. In a competitive housing market, where every decision carries long-term consequences, understanding mortgage rates has become a critical financial skill rather than just basic knowledge.

What Are 30-Year Mortgage Rates

A 30-year mortgage rate is the interest charged on a home loan that is repaid over a thirty-year period, making it one of the most widely used mortgage options worldwide. The main advantage of this structure is lower monthly payments, which makes homeownership more accessible to a larger number of people. However, because the loan is spread over a longer time, the total interest paid is significantly higher compared to shorter-term mortgages. Fixed-rate mortgages provide stability by keeping the same rate throughout the loan period, while adjustable-rate mortgages can change depending on market conditions. To better understand how these mortgage structures work in real-life situations, many borrowers rely on financial guidance platforms such as MoneyHelper’s home buying guide, which explains different mortgage options and their long-term impact in a clear and practical way. This kind of understanding helps borrowers make decisions based on both affordability and long-term financial planning.

Factors Influencing 30-Year Mortgage Rates Today

The factors influencing today are a mix of economic conditions and personal financial profiles. Inflation is one of the biggest drivers, as rising prices usually lead to higher interest rates to control spending. Central bank policies also play a major role, as changes in base rates directly affect how much lenders charge borrowers. At the same time, global economic conditions, including energy prices and market stability, influence rate movements. On a personal level, lenders evaluate borrowers based on credit score, income stability, and debt levels, which determine the level of risk involved in lending. Borrowers who want to compare real offers and understand how rates vary between lenders often use tools like the Compare the Market mortgage comparison tool, which allows them to evaluate different options and choose the most suitable one. This combination of economic and personal factors makes mortgage rates dynamic and requires borrowers to stay informed.

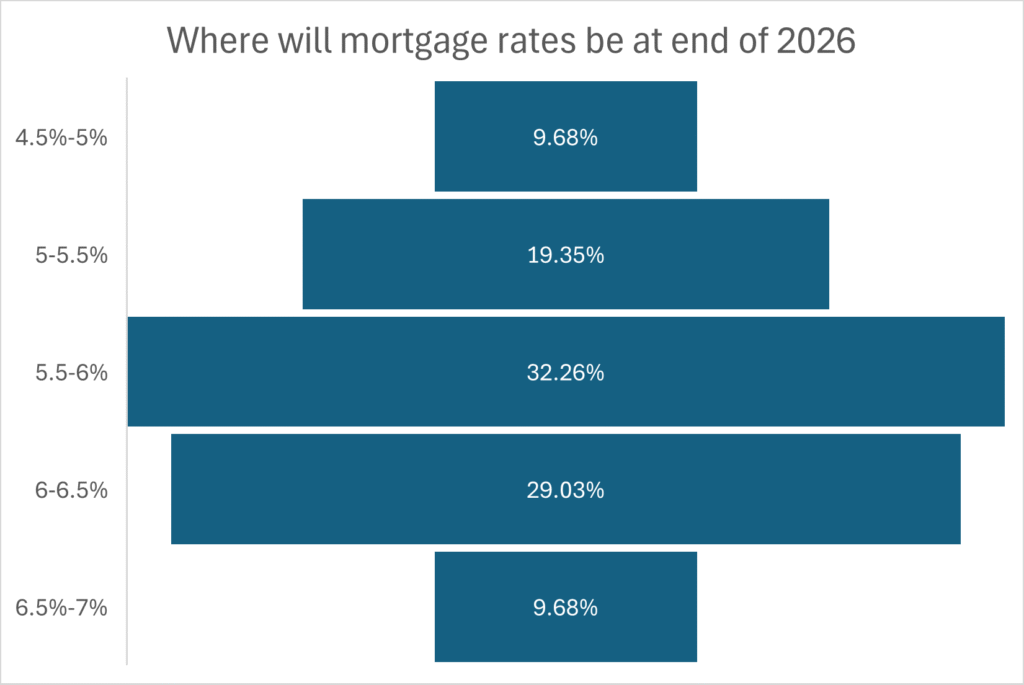

Current Trends in 2026

Mortgage interest rates in 2026 are showing signs of stability after a period of uncertainty, giving borrowers more confidence when planning long-term financial commitments. Although rates are higher than the historic lows seen in earlier years, they are now more predictable, which helps individuals make better decisions. Housing demand remains strong, especially in urban areas, which continues to influence property prices and lending strategies. Lenders are also becoming more competitive by offering flexible repayment options and digital services to attract customers. The rise of online platforms has made it easier for borrowers to access information and compare rates, reducing reliance on traditional methods. However, global economic uncertainty still exists, which means borrowers must stay updated and prepared for potential changes in the market.

Fixed vs Adjustable 30 Year Mortgage Rates

Choosing between fixed and adjustable mortgage rates is one of the most important decisions borrowers face when selecting a 30-year mortgage. Fixed rates provide stability and predictable payments, making them ideal for long-term planning. Adjustable rates offer lower initial costs but can increase over time, which introduces a level of risk. The choice depends on individual financial goals and risk tolerance. Those planning to stay in their homes for a long time often prefer fixed rates, while those expecting to move or refinance may consider adjustable options.

Impact on Monthly Payments and Total Cost

Mortgage rates have a direct impact on both monthly payments and the total cost of a loan. Higher interest rates result in higher monthly payments and significantly increase the total repayment amount over time. Even a small increase in rates can lead to thousands in additional costs over a thirty-year period. This makes it essential for borrowers to compare lenders and secure the best possible rate. Understanding this impact helps individuals plan their finances more effectively and avoid long-term financial stress.

Long-Term Financial Strategy

A 30-year mortgage requires a strong long-term financial strategy that considers future income, expenses, and economic conditions. Borrowers must evaluate their financial stability and choose a mortgage option that aligns with their goals. Fixed rates offer predictability, while adjustable rates provide flexibility but require careful monitoring. Making a larger down payment and maintaining a good credit score can also help secure better rates. Planning ahead ensures that mortgage payments remain manageable over time and supports long-term financial stability.

Conclusion

30-year mortgage rates today in 2026 play a critical role in determining the cost and affordability of homeownership. With rates influenced by economic conditions and personal financial factors, borrowers must take a strategic and informed approach when choosing a mortgage. By understanding how rates work, comparing available options, and planning for the future, individuals can make better financial decisions and achieve long-term stability.

: Compare Top Options")

: Top Picks & Reviews")