Understanding FHA Home Loans: A Comprehensive Guide to Homeownership Accessibility

Introduction: The Gateway to Homeownership

The dream of owning a home is deeply ingrained in the human psyche, representing stability, security, and a tangible investment in the future. However, for millions of individuals and families across the nation, this dream often seems unattainable due to financial constraints and credit limitations. This is where Federal Housing Administration loans emerge as a beacon of hope, transforming what many perceive as an impossible dream into a realistic and achievable goal. FHA home loans have fundamentally changed the landscape of homeownership, making it accessible to people who might otherwise never have the opportunity to purchase their own property.

Since their establishment during the Great Depression, FHA loans have served as a critical tool in democratizing homeownership. These government-backed mortgages have enabled millions of Americans to transition from renters to homeowners, creating pathways to wealth building and community stability. Understanding the nuances, benefits, and requirements of FHA loans is essential for anyone considering homeownership, particularly first-time buyers who may feel overwhelmed by the traditional mortgage process.

The Historical Context and Purpose of FHA Loans

To truly appreciate FHA home loans, one must understand their historical significance and the compelling reasons for their creation. During the economic devastation of the Great Depression, the housing market collapsed catastrophically. Banks were unwilling to lend money, and homeowners defaulted on their mortgages in unprecedented numbers. The standard mortgages of that era required substantial down payments, often ranging from thirty to fifty percent, with short repayment periods of just five to ten years. These requirements were absolutely prohibitive for average working families struggling merely to survive.

Recognizing the dire need for intervention, the federal government established the Federal Housing Administration in 1934 as part of President Franklin D. Roosevelt’s New Deal. The primary purpose was to stabilize the housing market and provide Americans with access to affordable, secure housing. The FHA didn’t lend money directly; rather, it insured mortgages issued by private lenders, essentially assuring banks that the government would cover losses if borrowers defaulted. This revolutionary approach dramatically reduced the risk for lenders and motivated them to extend credit to borrowers who previously would have been deemed too risky.

The impact was transformative. By assuming the risk, the FHA enabled lenders to offer mortgages with much lower down payments and longer repayment periods. This fundamental shift in lending practices opened the doors to homeownership for countless families who had been permanently locked out of the housing market. Today, more than ninety years later, FHA loans continue to serve a similar crucial function, helping first-time homebuyers, those with limited financial resources, and borrowers with imperfect credit histories achieve their homeownership dreams.

Who Qualifies for FHA Loans: Eligibility Requirements

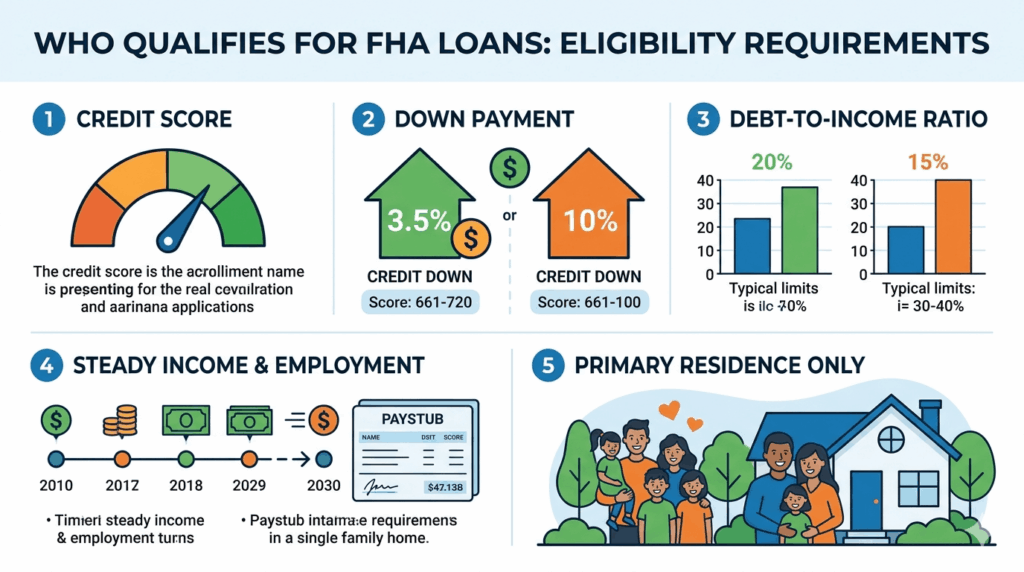

The beauty of FHA loans lies in their accessibility, but they are not without requirements. Understanding who qualifies for these mortgages is the first step in determining whether this loan type suits your situation. FHA loans are primarily designed for owner-occupied homes, meaning the borrower must live in the property as their primary residence. This requirement distinguishes FHA loans from investor mortgages and ensures that the program’s benefits genuinely serve homeowners rather than real estate speculators.

Credit score requirements represent another crucial eligibility factor. While FHA loans are known for being more lenient than conventional mortgages, they still require borrowers to demonstrate some credit responsibility. The official minimum credit score for an FHA loan is typically around five hundred and eighty points, though many lenders prefer scores of six hundred and twenty or higher to reduce perceived risk. This requirement is significantly lower than conventional mortgage standards, which often demand credit scores of seven hundred or above, making FHA loans accessible to people who have experienced financial difficulties or credit challenges.

Income requirements for FHA loans are typically determined using debt-to-income ratios rather than absolute income thresholds. Generally, lenders prefer that your total monthly debt payments, including the new mortgage, do not exceed approximately forty-three to fifty percent of your gross monthly income. This flexibility allows borrowers across various income levels to qualify based on their individual financial circumstances. Self-employed individuals and those with non-traditional income sources may face additional documentation requirements, but the program remains accessible to diverse employment situations.

The concept of a gift down payment distinguishes FHA loans from many conventional mortgage products. While all loans require some down payment, FHA loans allow borrowers to put down as little as three and one-half percent of the purchase price. Perhaps more remarkably, this down payment can be a gift from a family member, friend, or charitable organization, eliminating the requirement that borrowers accumulate savings independently. This feature has been instrumental in helping young families and first-generation homebuyers overcome one of the most significant barriers to homeownership: saving enough money for a down payment.

The Financial Structure: Understanding FHA Mortgage Insurance

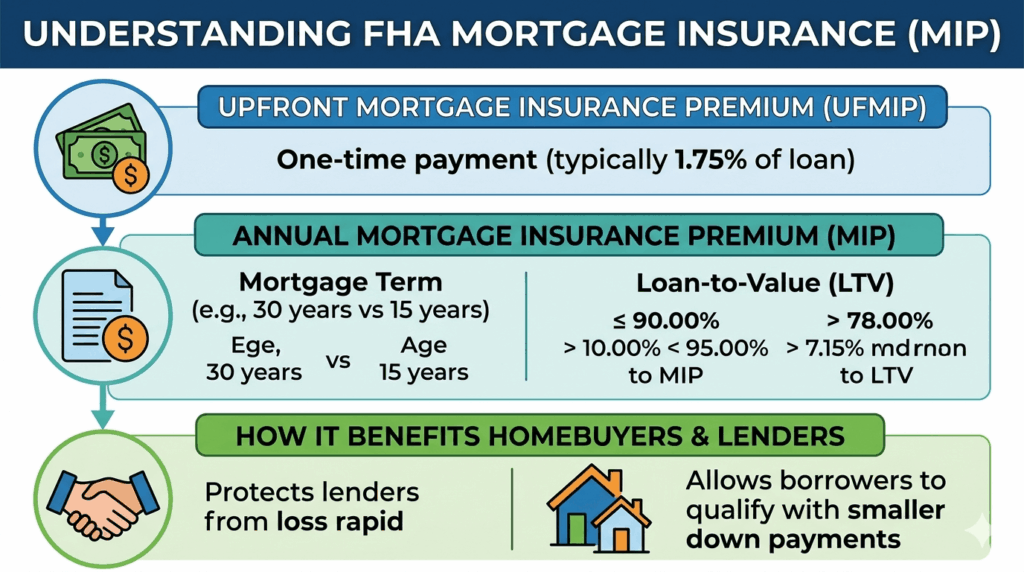

One of the most important aspects of FHA loans that borrowers must understand is mortgage insurance. Unlike conventional loans where mortgage insurance becomes unnecessary once the borrower’s equity reaches twenty percent of the home’s value, FHA loans operate differently. Understanding this distinction is crucial for calculating the true cost of borrowing.

FHA loans require two types of mortgage insurance. The first, called the upfront mortgage insurance premium, is assessed at closing and typically ranges from one to one and three-quarter percent of the loan amount. This insurance can be paid out of pocket at closing or, more commonly, rolled into the loan amount itself. The second form, called annual mortgage insurance premium, is a recurring monthly charge that continues for as long as the loan remains active. This monthly insurance premium ranges from approximately zero point five five to zero point eight five percent of the loan balance annually, divided into twelve monthly payments.

The presence of mortgage insurance significantly impacts the overall cost of an FHA loan. Borrowers must carefully calculate the total monthly payment, including principal, interest, property taxes, homeowners insurance, and mortgage insurance, to understand the true expense of the mortgage. While these insurance costs may seem like a disadvantage compared to conventional loans, they represent the enabling mechanism that allows borrowers with limited down payments and less-than-perfect credit to access homeownership. For many borrowers, this trade-off is worthwhile, transforming homeownership from impossible to achievable.

Interest Rates and Borrowing Costs

Interest rates on FHA loans typically float between competitive and slightly higher than conventional mortgages, depending on market conditions and individual borrower factors. The interest rate you receive will depend on various factors including your credit score, the loan amount, the property location, and current market conditions. While FHA borrowers might pay slightly higher rates than borrowers with excellent credit and large down payments, the rate remains favorable compared to alternative lending options available to people with similar financial profiles.

The thirty-year fixed-rate mortgage has become the standard term for FHA loans, providing borrowers with predictable monthly payments and long-term payment schedules that match most people’s financial capabilities. The fixed-rate structure means that unlike adjustable-rate mortgages, your interest rate and principal payment never change throughout the life of the loan, providing crucial financial stability and predictability.

Property Requirements and Appraisal Standards

FHA loans come with specific property requirements designed to protect both the lender and the borrower. The property must be an owner-occupied single-family home, condominium, townhouse, or manufactured home that meets FHA standards. The home must serve as the borrower’s primary residence, and properties used solely for investment purposes are not eligible for FHA financing.

All FHA-financed properties must undergo FHA appraisal to ensure the property’s value supports the loan amount and that the home meets FHA property standards. The appraisal process is more stringent than conventional appraisals. The property must be in satisfactory condition, with major systems functional and in reasonable repair. FHA appraisers inspect the foundation, roof, plumbing, electrical systems, heating and cooling systems, and other critical components to ensure the property meets safety and livability standards. This requirement actually protects borrowers by preventing them from purchasing properties with hidden defects or structural problems that could compromise their investment.

Properties with FHA loans must also have clear title, meaning there are no legal claims or liens against the property that would interfere with the lender’s security interest. The title search and title insurance, included as standard parts of the FHA mortgage process, provide protection for both the borrower and the lender.

The Application and Approval Process

The FHA loan application process, while comprehensive, is designed to be thorough yet accessible. Applicants must provide extensive documentation including recent tax returns, W-2 forms, recent pay stubs, bank statements, and documentation of any other income sources. This documentation serves to verify the borrower’s financial stability and income reliability, giving lenders confidence in the borrower’s ability to meet monthly mortgage obligations.

The underwriting process, during which a lender’s underwriter reviews all application materials and verifies the information provided, is critical. The underwriter evaluates the borrower’s creditworthiness, income stability, savings history, and overall financial responsibility. They also order the property appraisal and review the appraisal results to ensure the property supports the loan amount.

Pre-approval, an initial assessment of borrowing capacity based on preliminary financial information, can often be obtained quickly, even before property selection. This pre-approval gives prospective buyers confidence in their borrowing power and strengthens their position when making offers on properties. Full approval, which comes after property selection and appraisal, represents the lender’s commitment to fund the mortgage.

Advantages That Transform Lives

The advantages of FHA loans extend far beyond mere financial mechanics. For first-time homebuyers, FHA loans represent genuine opportunity. The low down payment requirement eliminates what is often the most significant barrier to homeownership. Rather than spending years saving twenty percent of a home’s purchase price, borrowers can achieve homeownership with just three and one-half percent down, dramatically accelerating the path to homeownership.

The more forgiving credit score requirements acknowledge the reality that many responsible people have experienced credit challenges due to circumstances beyond their control. Job loss, medical emergencies, divorce, or other life disruptions can temporarily damage credit scores, but they don’t necessarily indicate that someone is a poor credit risk or unwilling to meet mortgage obligations.

The ability to use gift funds for the down payment eliminates another significant barrier, particularly for young people and first-generation homebuyers whose families may not have accumulated substantial wealth but can contribute relatively modest amounts to help a family member achieve homeownership. This feature has tremendous social significance, allowing wealth-building opportunities to extend beyond wealthy families.

Considerations and Limitations

While FHA loans offer tremendous advantages, prospective borrowers should also understand their limitations and considerations. Mortgage insurance requirements increase the total cost of the loan. The annual mortgage insurance premium, in particular, represents an ongoing expense throughout the loan’s life that conventional borrowers can eventually eliminate. The upfront mortgage insurance premium also increases the initial loan amount, meaning borrowers pay interest on the insurance premium itself.

Debt-to-income ratio limits, while more flexible than conventional standards, still constrain borrowing capacity. A borrower earning a modest income may find that FHA lending limits restrict their ability to purchase in expensive real estate markets, though this reflects practical borrowing limits rather than a limitation unique to FHA loans.

Property condition requirements, while protective, mean that certain distressed properties or fixer-uppers that might appeal to some buyers may not qualify for FHA financing. The property must meet baseline livability standards, which is genuinely protective but does limit the range of properties that borrowers can finance.

Conclusion: A Pathway to Stability and Wealth Building

FHA home loans represent one of the most significant government programs supporting American homeownership and residential stability. By insuring mortgages for borrowers who might otherwise be locked out of homeownership, the FHA has enabled millions of Americans to build wealth through property ownership, achieve residential stability, and create lasting security for their families. These loans acknowledge the reality that financial perfection should not be a prerequisite for homeownership, that people deserve opportunity to build better lives through property ownership, and that the stability of homeownership benefits not just individuals but entire communities and society.

For anyone considering homeownership but feeling discouraged by financial constraints or past credit challenges, FHA loans offer a viable, practical pathway forward. Understanding how these loans work, what they require, and what they offer positions borrowers to make informed decisions about their financial futures. The dream of owning a home is not reserved for the wealthy or those with perfect credit histories. Through FHA loans, it remains within reach for millions of hardworking Americans determined to build better lives for themselves and their families.

: Top Picks & Reviews")