MORTGAGE CALCULATOR WITH TAXES

A Complete SEO-Optimized Guide to Understanding, Calculating,

and managing your mortgage payments, including property taxes

Executive Summary

Buying a home is one of the most significant financial decisions most people will ever make in their lifetime. Understanding how a mortgage works, especially when property taxes are factored in is absolutely critical for responsible homeownership. This comprehensive guide serves as a definitive resource on the mortgage calculator with taxes, providing detailed explanations, theoretical frameworks, practical formulas, real-world examples, and actionable advice for homebuyers at every stage of the purchasing process.

Whether you are a first-time homebuyer trying to understand your monthly obligations, a seasoned investor evaluating rental property returns, or a financial advisor guiding clients through home purchase decisions, this guide will equip you with the knowledge and tools necessary to make confident, well-informed choices. From the mathematical foundations of amortisation to the nuances of local property tax systems, every dimension of mortgage calculation with taxes is covered thoroughly in the sections that follow.

1. What Is a Mortgage? Foundational Concepts

1.1 Definition and Historical Background

A mortgage is a legal agreement between a borrower (mortgagor) and a lender (mortgagee) in which the lender provides funds to the borrower for the purchase of real estate, and the borrower pledges the property as collateral for the loan. The term ‘mortgage’ originates from Old French and Latin, literally meaning ‘dead pledge’, a reference to the pledge dying when either the debt is paid or the property is taken through foreclosure.

Mortgages have existed in various forms for thousands of years, but the modern mortgage as we know it began taking shape in the early 20th century. In the United States, the Federal Housing Administration (FHA), established in 1934, played a pivotal role in standardising the 30-year fixed-rate mortgage, which remains the most popular mortgage product today. This standardisation allowed millions of Americans to achieve homeownership who would otherwise have been unable to save large enough down payments for outright purchases.

1.2 Core Components of a Mortgage

Every mortgage, regardless of its specific type, consists of several core components that determine its total cost and monthly payment structure. Understanding each component individually allows borrowers to compare different mortgage products effectively and to understand precisely where their money goes each month.

- Principal: The original amount of money borrowed from the lender. This is the purchase price of the home minus the down payment. As you make monthly payments, a portion reduces the principal balance over time.

- Interest: The cost charged by the lender for providing the loan, expressed as an annual percentage rate (APR). Interest represents the lender’s profit and compensation for the risk of lending. Early in the loan, most of each payment goes toward interest rather than principal.

- Term: The length of time over which the loan is to be repaid. Common terms include 10, 15, 20, and 30 years. Shorter terms typically come with lower interest rates but higher monthly payments.

- Down Payment: The upfront amount the borrower pays from their own funds at the time of purchase. Down payments typically range from 3% to 20% or more of the home’s purchase price, depending on the loan type and lender requirements.

- Amortisation: The process by which loan payments are structured so that the loan is fully paid off at the end of the term. An amortisation schedule shows exactly how much of each payment goes to principal and how much goes to interest.

2. The Role of Property Taxes in Mortgage Calculations

2.1 What Are Property Taxes?

Property taxes are levies imposed by local governments, typically counties, municipalities, and school districts, on real estate owners. These taxes are a primary source of funding for essential public services, including public schools, road maintenance, emergency services (police and fire departments), parks and recreation, and local government administration.

Property taxes are based on the assessed value of the property and the local tax rate, often called the mill rate or millage rate. One mill equals one-tenth of one cent, or $1 per $1,000 of assessed value. For example, if your home has an assessed value of $300,000 and the local mill rate is 20 mills (2%), your annual property tax would be $6,000.

2.2 How Property Taxes Are Integrated into Mortgage Payments

Most lenders require borrowers to pay property taxes through an escrow account as part of their monthly mortgage payment. This protects the lender’s collateral interest by ensuring property taxes are always paid on time and the property is never at risk of a tax lien or tax sale. When property taxes are included in the monthly payment, the acronym PITI is used to describe the four components of the payment: Principal, Interest, Taxes, and Insurance.

The lender collects one-twelfth of the estimated annual property tax each month along with the principal and interest payment. These funds are held in the escrow account and disbursed directly to the taxing authority when property tax bills come due typically semi-annually or annually, depending on jurisdiction. Lenders also conduct annual escrow analyses to ensure the account maintains an adequate balance and to adjust monthly payments if tax assessments change.

2.3 Property Tax Assessment Methods

Property tax assessments vary significantly across jurisdictions and can be calculated using several different methodologies. Understanding how your local government assesses property values is essential for accurately estimating your property tax liability.

- Market Value Assessment: Many jurisdictions assess property at or near full market value. Market value is typically determined by comparing recent sales of similar properties in the area, a method known as the sales comparison approach.

- Fractional Assessment: Some jurisdictions assess property at a fixed fraction of market value (e.g., 80% or 60%). The resulting fractional assessed value is then multiplied by the tax rate to calculate the tax bill.

- Income Approach: For income-producing properties, assessors may use the capitalisation of net operating income to estimate market value, which is then used as the assessed value for tax purposes.

- Cost Approach: The cost approach estimates value based on what it would cost to replace the structure, minus depreciation, plus the value of the land. This method is often used for unique properties or new construction.

3. The PITI Framework: Understanding Full Monthly Payments

3.1 Breaking Down PIT I

The PITI framework is the most complete representation of monthly housing costs for mortgaged properties. Lenders use PITI when calculating debt-to-income (DTI) ratios and determining borrower eligibility. For borrowers, understanding PITI provides a realistic picture of the total monthly cash outflow required for homeownership.

| Component | Description | Example ($400K Home) |

|---|---|---|

| Principal (P) | Portion-reducing loan balance | $680 |

| Interest (I) | Cost of borrowing (6.5% rate) | $1,717 |

| Taxes (T) | Annual tax / 12 months | $500 |

| Insurance (I) | Homeowners insurance / 12 | $150 |

| PMI (if applicable) | Private mortgage insurance | $133 |

| TOTAL PIT I | Full monthly housing payment | $3,180 |

3.2 Why Lenders Use PITI

Lenders use the full PITI payment, not just principal and interest, when evaluating a borrower’s ability to repay. The industry-standard guideline is that PITI should not exceed 28% of gross monthly income (the front-end DTI ratio), and total debt payments (PITI plus all other monthly debt obligations) should not exceed 36% to 43% of gross monthly income (the back-end DTI ratio). These thresholds vary by loan type and individual lender guidelines.

Understanding PITI also helps borrowers avoid the common mistake of shopping for homes based solely on the purchase price. A home priced at $350,000 in a high-tax jurisdiction could easily have a higher monthly PITI than a $400,000 home in a low-tax area, simply because of the difference in property tax burdens.

4. Mortgage Calculation Formulas and Mathematics

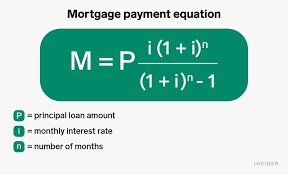

4.1 The Standard Monthly Payment Formula

The foundation of any mortgage calculator is the monthly payment formula, derived from the present value of an annuity. This formula calculates the fixed monthly payment required to fully amortise a loan over a specified term at a fixed interest rate.

Monthly Payment (M) = P × [r(1+r)^n] / [(1+r)^n – 1]

Where: P = Principal loan amount | r = Monthly interest rate (annual rate / 12) | n = Total number of monthly payments (years × 12)

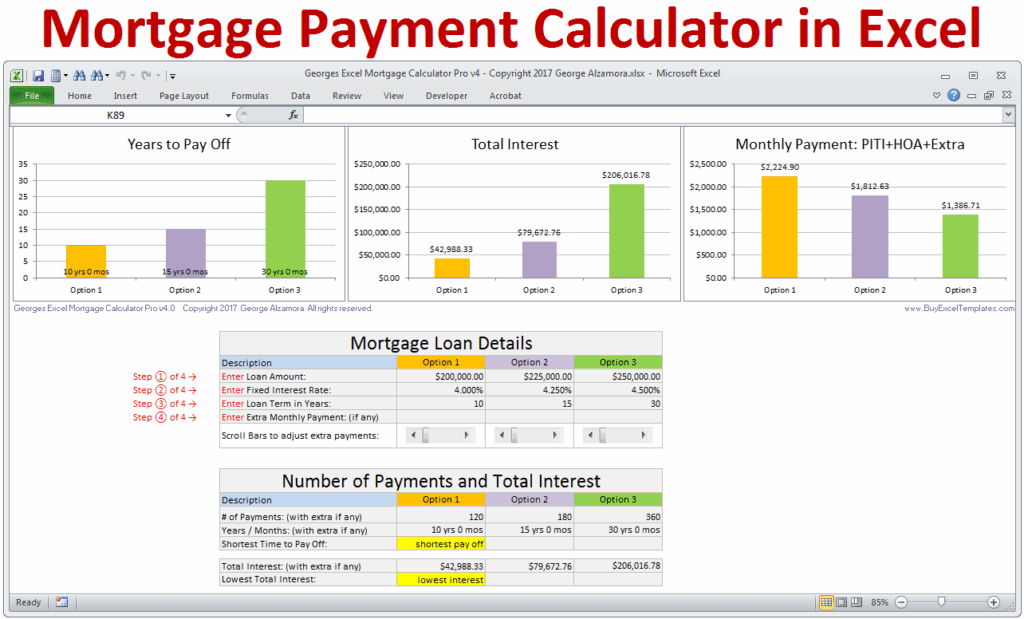

4.2 Step-by-Step Calculation Example

Let us work through a complete example to illustrate how this formula operates in practice. Assume the following scenario:

- Home Purchase Price: $450,000

- Down Payment: $90,000 (20%)

- Loan Amount (Principal): $360,000

- Annual Interest Rate: 6.75%

- Loan Term: 30 years (360 months)

- Annual Property Tax: $5,400 ($450/month)

- Annual Homeowners Insurance: $1,800 ($150/month)

Step 1: Calculate monthly interest rate: r = 6.75% / 12 = 0.5625% = 0.005625

Step 2 Calculate number of payments: n = 30 × 12 = 360

Step 3 Apply the formula: M = 360,000 × [0.005625 × (1.005625)^360] / [(1.005625)^360 – 1]

Step 4: Calculate (1.005625)^360 = approximately 7.6861

Step 5 M = 360,000 × [0.005625 × 7.6861] / [7.6861 – 1] = 360,000 × 0.04323 / 6.6861 = $2,333.44

Step 6: Add Taxes and Insurance: $2,333.44 + $450 + $150 = $2,933.44 (PITI)

4.3 Amortization Schedule Overview

An amortisation schedule is a complete table showing every payment over the life of the loan, breaking down how much goes to principal and interest each month. Early payments are heavily weighted toward interest. In our example above, Month 1 would see approximately $2,025 going to interest and only $308 reducing the principal. By Month 360 (the final payment), nearly the entire payment goes toward principal.

| Payment # | Payment Amount | Principal Paid | Interest Paid | Balance Remaining |

|---|---|---|---|---|

| 1 | $2,333.44 | $308.44 | $2,025.00 | $359,691.56 |

| 12 | $2,333.44 | $328.46 | $2,004.98 | $355,786.32 |

| 60 | $2,333.44 | $405.18 | $1,928.26 | $342,427.72 |

| 120 | $2,333.44 | $552.89 | $1,780.55 | $316,649.45 |

| 180 | $2,333.44 | $754.60 | $1,578.84 | $280,528.40 |

| 240 | $2,333.44 | $1,029.09 | $1,304.35 | $231,240.15 |

| 300 | $2,333.44 | $1,403.85 | $929.59 | $164,673.75 |

| 360 | $2,333.44 | $2,320.34 | $13.10 | $0.00 |

5. Types of Mortgages and Their Tax Implications

5.1 Fixed-Rate Mortgages

A fixed-rate mortgage is the simplest and most predictable type of home loan. The interest rate remains constant throughout the entire loan term, which means the principal and interest portion of the monthly payment never changes. This predictability makes budgeting straightforward and protects borrowers from interest rate volatility.

While the principal and interest payment is fixed, the total PITI payment can still change over time if property tax assessments are revised. In most jurisdictions, property values are reassessed periodically (annually, biennially, or on some other schedule), which can cause the tax portion of the monthly escrow payment to increase or decrease. Homeowners should be prepared for escrow payment adjustments even with a fixed-rate mortgage.

5.2 Adjustable-Rate Mortgages (ARMs)

An adjustable-rate mortgage (ARM) features an interest rate that changes periodically after an initial fixed period. For example, a 5/1 ARM has a fixed rate for the first five years, then adjusts annually based on a benchmark index (such as the Secured Overnight Financing Rate, or SOFR) plus a margin set by the lender. ARMs typically offer lower initial interest rates than fixed-rate mortgages, making them attractive to buyers who expect to sell or refinance before the adjustment period begins.

For mortgage calculation purposes with ARMs, it is essential to calculate payments both at the initial rate and at the maximum possible rate (rate cap) to understand the worst-case scenario. ARMs typically have periodic caps (limiting how much the rate can change at each adjustment) and lifetime caps (the maximum rate increase over the life of the loan).

5.3 Government-Backed Loan Programs

Several government agencies guarantee mortgage loans, allowing approved lenders to offer these products with more flexible qualifying criteria than conventional loans. The three major government-backed mortgage programmes are FHA loans (Federal Housing Administration), VA loans (Department of Veterans Affairs), and USDA loans (U.S. Department of Agriculture).

- FHA Loans: Require as little as 3.5% down payment and accept credit scores as low as 580. FHA loans require both an upfront mortgage insurance premium (UFMIP) and an annual mortgage insurance premium (MIP) regardless of down payment size, which must be factored into PITI calculations.

- VA Loans: Available to eligible veterans, active-duty service members, and surviving spouses. VA loans require no down payment and no private mortgage insurance. They do require a one-time funding fee that can be financed into the loan.

- USDA Loans: Available for homes in eligible rural and suburban areas and also require no down payment. USDA loans have income limits and geographic restrictions but offer competitive interest rates and low mortgage insurance requirements.

6. Property Tax Rates by State and Region

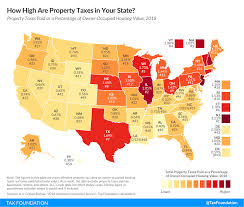

6.1 Geographic Variation in Property Taxes

Property tax rates vary dramatically across the United States and internationally. In the U.S., effective property tax rates (annual taxes as a percentage of home value) range from under 0.3% in states like Hawaii to over 2% in states like New Jersey, Illinois, and New Hampshire. Understanding your local tax environment is critical for accurate mortgage calculations.

| State | Avg. Effective Tax Rate | Median Home Value | Median Annual Tax |

|---|---|---|---|

| New Jersey | 2.13% | $389,700 | $8,300 |

| Illinois | 1.97% | $239,700 | $4,720 |

| New Hampshire | 1.89% | $295,100 | $5,580 |

| Connecticut | 1.73% | $298,800 | $5,170 |

| Texas | 1.60% | $255,600 | $4,090 |

| California | 0.71% | $568,500 | $4,040 |

| Florida | 0.80% | $294,900 | $2,360 |

| Hawaii | 0.27% | $669,200 | $1,810 |

6.2 Homestead Exemptions and Other Tax Reliefs

Most states offer homestead exemptions that reduce the taxable assessed value of a primary residence, resulting in lower property tax bills for owner-occupants. The specifics vary widely: some states offer a flat dollar exemption (e.g., Florida’s $50,000 homestead exemption), while others offer a percentage reduction or a combination of both.

Additional property tax relief programmes are commonly available for senior citizens (senior homestead exemptions, circuit breaker programs), veterans and disabled veterans, persons with disabilities, and surviving spouses of police officers and firefighters. Borrowers should research all available exemptions in their jurisdiction and account for them when projecting annual property tax costs.

7. Using a Mortgage Calculator with Taxes: A Practical Guide

7.1 Inputs Required for Accurate Calculations

A comprehensive mortgage calculator with taxes requires several key inputs to produce accurate results. Missing or incorrectly estimated inputs, particularly property taxes and insurance, can lead to significant underestimates of true monthly costs and create financial strain after purchase.

- Home Purchase Price: The agreed-upon sale price or your estimated budget. This is the starting point for all calculations.

- Down Payment: Enter as either a dollar amount or percentage. Most conventional loans require at least 20% to avoid PMI. FHA loans allow as low as 3.5%.

- Annual Interest Rate: The current market rate for your loan type and term. Always use the APR rather than the nominal rate for accurate cost comparisons.

- Loan Term: Typically 15 or 30 years. Shorter terms build equity faster but require higher monthly payments.

- Annual Property Tax: Research your county assessor’s records for the specific property, or use the jurisdiction’s average effective tax rate multiplied by the purchase price as an estimate.

- Annual Homeowners Insurance: Varies by location, age, and features of the home, size of dwelling, and coverage selected. A general estimate is 0.5% to 1% of the home’s value annually.

- HOA Fees: If the property is in a homeowners association, add the monthly dues to the PITI calculation.

- PMI Rate: If the down payment is less than 20%, add private mortgage insurance, typically 0.5% to 1.5% of the loan amount annually, divided by 12.

7.2 Interpreting Calculator Results

Once you have entered all required inputs, a mortgage calculator with taxes will typically provide several outputs. Monthly payment (PITI) is the most important figure this is the actual out-of-pocket monthly cost you must budget for. Total interest paid over the life of the loan demonstrates the true cost of borrowing and can be eye-opening. The amortisation schedule shows how your equity builds over time. The loan-to-value (LTV) ratio indicates your equity position and determines whether PMI is required.

Many calculators also provide affordability analyses comparing the projected PITI against common qualifying guidelines, loan comparison tools allowing you to compare multiple scenarios side by side, and refinancing break-even calculations if you are considering a refinance.

8. Advanced Considerations in Mortgage Planning

8.1 The True Cost of Homeownership Beyond PIT I

Even a perfectly accurate PITI calculation understates the true cost of homeownership. Savvy homebuyers budget not only for their monthly mortgage payment but also for ongoing maintenance and repairs, which financial experts recommend budgeting at 1% to 2% of the home’s purchase price annually. Utility costs, particularly in older or larger homes, can add hundreds of dollars per month. Capital expenditures on major systems and components with limited lifespans, such as HVAC systems, roofs, appliances, and water heaters, must be anticipated and saved for proactively.

8.2 Refinancing Strategy and When It Makes Sense

Refinancing involves replacing an existing mortgage with a new loan, typically to obtain a lower interest rate, change the loan term, switch from an ARM to a fixed rate, or tap home equity through a cash-out refinance. The key metric for evaluating whether a refinance makes financial sense is the break-even period: the number of months required for monthly payment savings to offset the closing costs of the new loan.

Break-Even Months = Total Closing Costs / Monthly Payment Reduction. As a general guideline, if you plan to remain in the home beyond the break-even period, refinancing is typically beneficial. However, resetting to a new 30-year term can also increase total interest paid even if the monthly payment decreases, so always calculate the total cost of both options.

8.3 Extra Payments and Loan Payoff Acceleration

Making additional principal payments whether as a regular monthly extra payment, an annual lump sum, or a bi-weekly payment strategy can significantly reduce both the total interest paid and the loan term. For example, on a $360,000 loan at 6.75% for 30 years, adding just $200 to each monthly payment reduces the loan term by approximately 4.5 years and saves over $60,000 in interest. This is one of the most powerful wealth-building strategies available to homeowners.

9. Mortgage Tax Deductions and Tax Benefits

9.1 The Mortgage Interest Deduction

In the United States, homeowners who itemise deductions on their federal tax return can deduct the interest paid on mortgage debt up to $750,000 (for loans originated after December 15, 2017, under the Tax Cuts and Jobs Act). For loans originated before that date, the limit is $1 million. This deduction reduces taxable income dollar-for-dollar, providing a meaningful tax benefit, especially in the early years of a mortgage when interest constitutes the largest portion of each payment.

However, it is important to note that the Tax Cuts and Jobs Act also nearly doubled the standard deduction, which means that fewer taxpayers benefit from itemising deductions and thus the mortgage interest deduction than was the case prior to 2018. Homeowners should work with a qualified tax professional to determine whether itemising produces a greater tax benefit than taking the standard deduction.

9.2 Property Tax Deductibility

Homeowners who itemise can also deduct state and local taxes paid, including property taxes, up to a combined limit of $10,000 ($5,000 if married filing separately) under the SALT (State and Local Tax) deduction cap introduced by the Tax Cuts and Jobs Act. This cap particularly impacts homeowners in high-tax states where property taxes alone can exceed $10,000 annually.

9.3 Capital Gains Exclusion on Sale

When you sell your primary residence, you may exclude up to $250,000 ($500,000 if married filing jointly) of capital gains from federal income tax, provided you have owned and lived in the home as your primary residence for at least two of the five years preceding the sale. This exclusion can be a powerful tax benefit and represents one of the most favourable tax treatments available to individual taxpayers.

10. Frequently Asked Questions About Mortgage Calculators with Taxes

Q1: Why does my actual mortgage payment differ from the calculator result?

Calculator discrepancies most often arise from differences in how property taxes are estimated, HOA fees that were omitted, PMI that was not included, homeowners insurance cost variances, or lender-specific fees that affect the monthly payment. Always verify property tax amounts directly with the county assessor’s office and get insurance quotes before finalising your budget.

Q2: Can property taxes increase after I purchase the home?

Yes, property taxes can and frequently do increase after purchase. Assessment increases tied to rising property values, voter-approved tax increases for school districts or other public services, loss of a previous owner’s exemptions that did not transfer, and reassessment triggered by the sale itself can all cause property tax increases. Budget conservatively by assuming some level of property tax growth over time.

Q3: How does an escrow shortage affect my monthly payment?

If your escrow account has insufficient funds to cover projected tax and insurance payments – a condition known as an ‘escrow shortage’ – your lender will increase your monthly payment to replenish the account. Lenders typically allow borrowers to either pay the shortage in a lump sum or spread it over 12 months with higher payments. Monitoring your annual escrow analysis statement helps you anticipate and plan for these adjustments.

Q4: Should I put 20% down to avoid PMI?

The answer depends on your specific financial situation, opportunity cost of the funds, and time horizon. Putting 20% down eliminates PMI and reduces your monthly payment, but it also means tying up more capital in a relatively illiquid asset. In some markets, investing that additional down payment capital in a diversified portfolio could generate returns that outpace PMI costs. Model both scenarios carefully with a financial advisor to determine the optimal strategy for your circumstances.

Conclusion

A mortgage calculator with taxes is far more than a simple mathematical tool; it is the foundation of sound financial planning for one of the most significant purchases of a lifetime. By understanding the full PITI payment, the mechanics of property tax assessment and escrow, the mathematics of amortisation, and the tax implications of homeownership, borrowers are empowered to approach the homebuying process with clarity, confidence, and financial discipline.

The information presented in this guide provides a comprehensive theoretical and practical foundation for understanding mortgages with taxes. However, every individual’s financial situation is unique, and the specific details of local tax rates, lender requirements, loan programs, and market conditions vary significantly by location and over time. Always work with qualified real estate professionals, mortgage advisors, and tax consultants who have current, jurisdiction-specific knowledge to ensure that your mortgage and homeownership decisions align with your long-term financial goals.

Homeownership remains one of the most reliable paths to wealth accumulation for the average family but only when approached with clear eyes, rigorous analysis, and a complete understanding of all costs involved. Use the frameworks, formulas, and insights in this guide as your starting point, and continue educating yourself as you navigate the mortgage process from application through closing and beyond.

: Top Picks & Reviews")

: Compare Top Options")

: Top Picks & Reviews")