What Is a No-Down-Payment Mortgage? Full Explained 2026

Introduction

What Is a No-Down-Payment Mortgage? Pros and Cons of a No-Down-Payment Mortgage: Should You Get One? Used to Jn Down Phase Explained. Payment for Mortgage? How to Get a Down Alternatives to a Down Mortgage

Quick Answer

A no-down-payment mortgage is a type of home loan that offers 100% financing, meaning you’re not required to pay anything at closing beyond closing costs. A no-down-payment mortgage, also called a zero-down mortgage, is a type of home loan that offers 100% financing on your home purchase.

No-down-payment mortgage loans can make it easier for first-time and low-income borrowers to buy a home. However, they can be more expensive and come with added risk. If you’re considering a mortgage loan with no down payment requirement, here’s what you need to know before you apply.

What Is a No-Down-Payment Mortgage?

Most mortgage programmes require you to make a down payment when buying a home, with many lenders requiring that you put down at least 3% to 5% of the purchase price or more in some cases. With a no-down-payment mortgage, however, you don’t need to put any money down at closing, though you’ll still need to pay closing costs set by your lender.

Compare mortgage rates

Check today’s rates to find the best loan offers. Staying updated on current rates helps you secure a competitive mortgage and save more over time. Looks like we’re having some trouble showing offers from our partners right now. In the meantime, you can sign in or create a free Experian account to unlock tools that can help you reach your financial goals.

Pros and Cons of a No-Down-Payment Mortgage

Buying a home with no down payment can be beneficial for certain borrowers, but it’s important to understand the costs and potential risks. Here’s what you need to know.

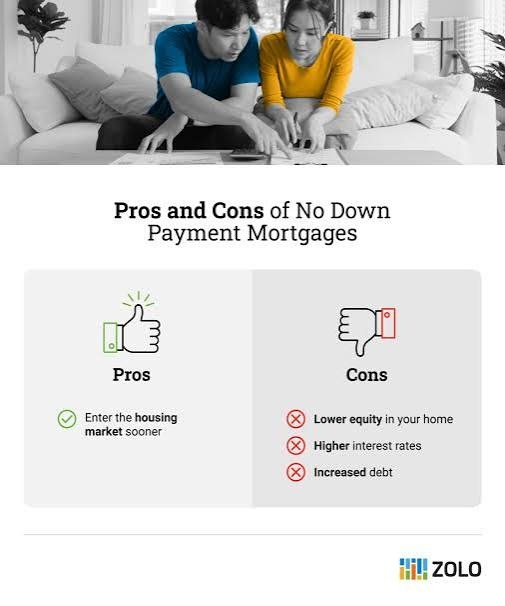

Pros

- Saves money upfront: Having no down payment can minimise your upfront costs when buying a house.

- As an example, the median sales price of a home in the U.S. is $419,200, according to fourth-quarter 2024 data from the Federal Reserve Bank of St.

- Louis. With a 3% down payment requirement, you’d have to pay $12,576 in addition to closing costs.

- A zero-down mortgage saves you that money.

Helps you buy a home sooner: It can take several months and often years to save up enough money for a down payment on a home. With a no-down-payment home loan, you can become a homeowner more quickly.

Helps preserve your savings: Buying a home is an expensive endeavour, and the costs go beyond your upfront expenses and monthly payments. You’ll also want to maintain reserves for moving costs, maintenance and repairs, which can be difficult if you also have to make a sizeable down payment.

Cons

- No home equity upfront: With 100% financing, you’re starting out with no equity.

- This can increase your chances of being underwater on your mortgage or owing more than the home is worth.

- What’s more, if you have to sell after living in the home for only a short time, you may take a loss on the sale.

- Higher mortgage payment: With no money down, you’re borrowing more money, resulting in a higher monthly payment.

- Additionally, no-down-payment mortgages tend to have higher interest rates, which further increases your monthly payment.

- Higher interest costs: Between a higher interest rate and a larger mortgage balance, you’ll end up paying more in interest over the life of the loan.

Should You Get a No-Down-Payment Mortgage?

It’s important to understand your situation, needs and goals to determine whether a zero-down mortgage loan is right for you. That said, here are some general situations where it could make sense:

You qualify for a loan program with no down payment requirement. You want to buy a home soon but have limited savings. You need to preserve your savings for closing costs, moving expenses, maintenance, repairs and other costs of homeownership. You don’t expect home prices to decline in the near future. You can afford a higher monthly payment.

In contrast, here are some scenarios where it could make sense to think twice about a zero-down mortgage loan:

You don’t qualify for a no-down-payment home loan programme. You have sufficient savings to cover your closing costs, moving expenses and other homeownership costs. You want to minimise your monthly mortgage payment. You expect home prices to decline in the near future, and you’re concerned about being underwater on your loan. You’re willing to take the time to save up for a down payment.

as little as 3% down. Good Neighbour Next Door (GNND) programme: If you’re a full-time law enforcement officer, pre-kindergarten through 12th grade teacher, firefighter or emergency medical technician, you may be eligible for the GNND programme, run by the U.S. Department of Housing and Urban Development (HUD).

It offers a minimum down payment of $100 and a discount of up to 50% on the purchase price of the property. Down payment assistance: Some government agencies and community organisations offer down payment assistance in the form of a grant, forgivable loan, deferred payment loan, low-interest loan or matched savings programme. They’re typically available to first-time homebuyers, but some repeat buyers may qualify.

The Bottom Line

It’s generally recommended for homebuyers to put some money down on their home purchase. However, it can be difficult for some to come up with enough cash to make that happen.

If you’re considering a zero-down mortgage, review your credit report and check your credit score first to evaluate your chances of qualifying for a loan with a good interest rate. While there’s no minimum credit score, lenders typically require a credit score of 620 or higher. Then, if necessary, take steps to get your credit in the best shape possible before applying for a mortgage loan.

Curious about your mortgage options?

Explore personalised solutions from multiple lenders and make informed decisions about your home financing. Leverage expert advice to see if you can save thousands of dollars.

")