7 Key Insights About Mortgage Interest Rates Today 2026

Opening Summary

Mortgage interest rates today, in 2026, are influenced by inflation trends, central bank policies, and global economic conditions, typically ranging between moderate and high levels compared to previous years. These rates directly affect borrowing costs, monthly payments, and long-term financial commitments for homeowners and investors. Understanding how mortgage rates work, what impacts them, and how to choose the right option is essential for making smart financial decisions in today’s market.

INTRODUCTION

Mortgage interest rates today play a central role in shaping the housing market and financial planning decisions for individuals and businesses. In 2026, these rates reflect a balance between economic recovery efforts and inflation control measures, making them more stable than previous volatile periods but still highly sensitive to global conditions. Borrowers are now more aware that even a small change in interest rates can significantly impact the total cost of a mortgage over time. For example, a difference of just one per cent can add thousands to the overall repayment amount, especially on long-term loans. This has made it essential for buyers to understand not only the current rates but also the factors that influence them. In a competitive property market, where demand remains strong, interest rates also affect affordability and buying decisions. For entrepreneurs, freelancers, and SMEs, managing mortgage commitments alongside fluctuating income streams requires careful planning, making it even more important to stay informed and strategic when entering into long-term financial agreements.

What Determines Mortgage Interest Rates

Mortgage interest rates are shaped by a complex combination of economic indicators and individual financial factors. One of the most important influences is the central bank’s base rate, which directly affects how much it costs lenders to borrow money. Institutions like the Bank of England regularly adjust these rates to control inflation and stabilise the economy, which in turn impacts mortgage pricing. You can explore how this works in more detail on the Bank of England website, where monetary policy decisions are explained in depth. In addition to central bank policies, inflation levels play a crucial role, as higher inflation typically leads to higher interest rates. On a personal level, lenders assess borrowers based on credit score, income stability, employment history, and debt levels. A strong financial profile can result in lower rates, while higher risk profiles lead to increased costs. Loan-specific factors such as deposit size and loan duration also influence the final rate offered. Understanding these factors allows borrowers to improve their financial standing and negotiate better mortgage terms.

Types of Mortgage Interest Rates Available

Mortgage interest rates come in several forms, each designed to meet different financial needs and preferences. Fixed-rate mortgages remain one of the most popular options because they offer stability by locking in the same interest rate for the entire loan term. This makes budgeting easier and protects borrowers from market fluctuations. On the other hand, variable or adjustable-rate mortgages offer lower initial rates but can change over time depending on market conditions. These are often chosen by borrowers who plan to move or refinance within a few years. Hybrid mortgages combine both features, providing a fixed rate for an initial period before switching to a variable rate. Each option has its own advantages and risks, making it important to choose based on long-term goals rather than short-term savings. For a clearer comparison of these options, platforms like MoneyHelper provide detailed insights and tools that help borrowers evaluate different mortgage types effectively and choose what suits their financial situation best.

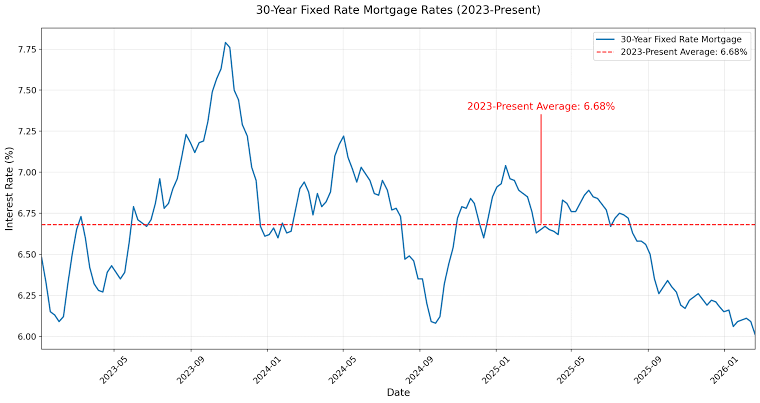

Current Mortgage Trends in 2026

The mortgage market in 2026 is showing signs of stability after several years of uncertainty and fluctuation. Interest rates are no longer at historic lows, but they are becoming more predictable, which allows borrowers to plan more effectively. Housing demand continues to remain strong, particularly in urban and developing areas, which keeps pressure on property prices and indirectly influences lending conditions. At the same time, lenders are competing to attract borrowers by offering flexible repayment options and competitive packages. Digital transformation has also made a significant impact, with online platforms allowing users to compare mortgage rates and apply for loans more easily than before. Tools like Compare the Market have become popular for comparing different mortgage deals and understanding cost variations. Despite these advancements, borrowers must remain cautious, as global economic changes, including inflation and geopolitical factors, can still affect interest rates. Staying informed and regularly reviewing options is key to making the best financial decisions.

Impact of Mortgage Rates on Monthly Payments

Mortgages have a direct and significant impact on monthly payments, making them one of the most important factors for borrowers to consider. Even a slight increase in the interest rate can lead to higher monthly payments, which can affect overall affordability and financial stability. For example, a borrower taking a long-term loan will pay considerably more in interest over time if the rate is higher, even by a small margin. This makes it essential to calculate not just the immediate monthly cost but also the total repayment amount over the life of the loan. Borrowers should also consider how changes in variable rates could affect future payments, especially in uncertain economic conditions. Understanding this impact helps individuals plan their budgets more effectively and avoid financial strain. It also highlights the importance of comparing different lenders and negotiating better terms to secure the most favourable rate possible.

Long-Term Financial Strategy and Mortgage Planning

Mortgage decisions should always be approached as part of a long-term financial strategy rather than a short-term commitment. Since most mortgages span decades, borrowers must consider how their financial situation may change over time, including income growth, career changes, and economic conditions. Choosing the right type of interest rate, whether fixed or variable, plays a crucial role in managing risk and ensuring stability. Fixed rates offer predictability, while variable rates may provide initial savings but carry uncertainty. Borrowers should also consider making larger down payments where possible, as this can reduce interest rates and overall loan costs. Planning ahead and understanding future financial goals helps in selecting the most suitable mortgage option. For business owners and freelancers, this becomes even more important, as income variability requires a more cautious and strategic approach to long-term financial commitments.

Conclusion

Mortgage interest rates today in 2026 are a critical factor in determining the cost and affordability of homeownership. With rates influenced by economic conditions, central bank policies, and individual financial profiles, borrowers must take a comprehensive approach when evaluating their options. Understanding the different types of mortgage rates, staying informed about market trends, and considering long-term financial goals are essential steps in making the right decision. While the current market offers stability compared to previous years, uncertainty still exists, making it important to remain flexible and proactive. By carefully analysing available options and planning strategically, borrowers can secure better mortgage terms and achieve financial stability over the long term.

FAQs

1. What are mortgage interest rates today in 2026?

They vary depending on lenders and market conditions but are generally moderate compared to previous years.

2. What affects mortgage interest rates the most?

Central bank policies, inflation, and borrower financial profiles are the main factors.

3. Are fixed or variable rates better?

It depends on your financial goals and risk tolerance.

4. How can I get a lower mortgage rate?

Improve your credit score, increase your deposit, and compare lenders.

5. Do mortgage rates change daily?

Yes, they can fluctuate based on market conditions.

6. Is now a good time to get a mortgage?

It depends on market trends and personal financial readiness.

7. How do interest rates affect monthly payments?

Higher rates increase monthly payments and total loan cost.

8. Can I refinance my mortgage later?

Yes, refinancing is possible if better rates become available.

: Compare Top Options")