FHA Loans: Understanding Federal Housing Administration Mortgages

INTRODUCTION

Federal Housing Administration loans have revolutionised homeownership in America since their inception during the Great Depression. These government-backed mortgages serve as a lifeline for millions of aspiring homeowners who face barriers to traditional lending. FHA loans fundamentally democratise homeownership by allowing borrowers with lower credit scores and minimal down payment savings to purchase their own homes.

Unlike conventional mortgages that require substantial financial reserves and pristine credit histories, FHA loans acknowledge that hard-working Americans deserve opportunity. The programme insures mortgages issued by private lenders, essentially assuming the risk and giving banks confidence to lend to borrowers deemed risky. This groundbreaking approach transformed housing markets and created generational wealth for families.

Establishment of the Federal Housing

Administration in 1934 marked a turning point in American housing history. President Franklin D. Roosevelt recognised the catastrophic collapse of the housing market during the Great Depression required immediate governmental intervention. Banks had stopped lending entirely, homeowners defaulted in record numbers, and families faced homelessness despite wanting to work and pay mortgages.

Traditional mortgages of that era demanded down payments of thirty to fifty per cent, completely unattainable for average workers. The FHA’s innovative approach didn’t create a new government lending institution; instead, it insured private mortgages, dramatically reducing lender risk. This creative solution jump-started lending and enabled thousands of families to purchase homes and rebuild lives.

FHA Loans Operate Fundamentally

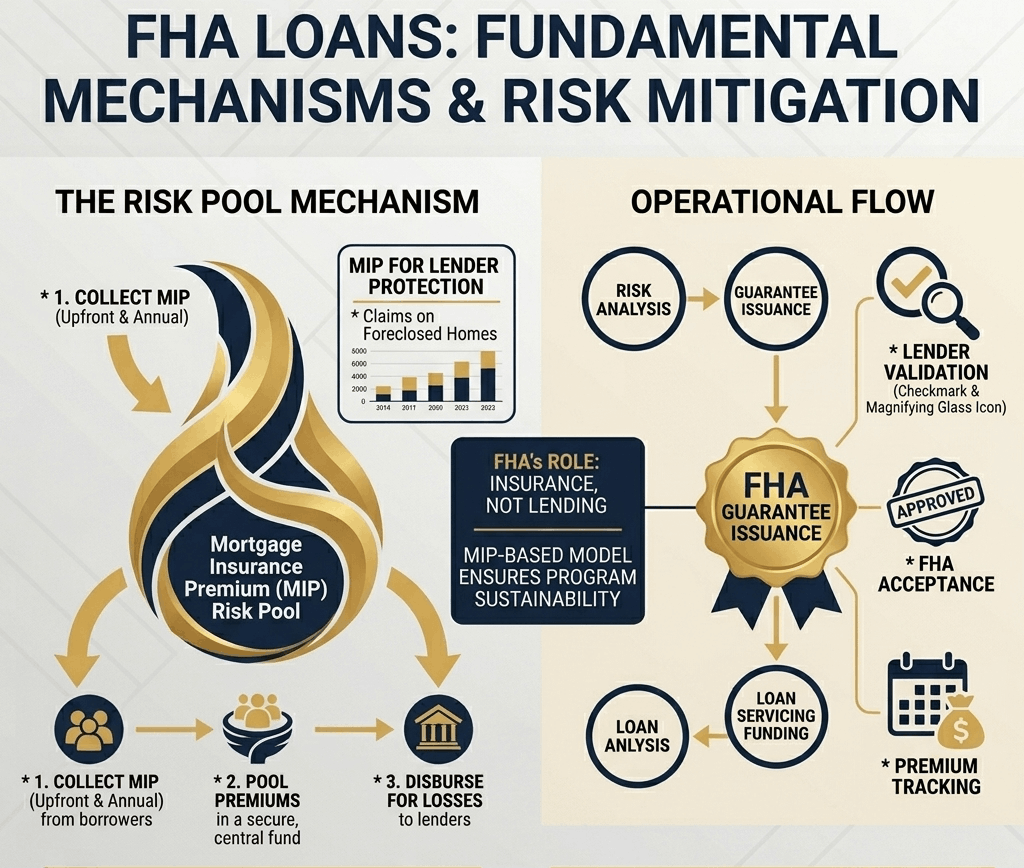

Differently from conventional mortgages in how they distribute financial risk. Rather than the lender bearing all default risk, the FHA insures the mortgage, protecting the lender’s investment. This insurance mechanism allows lenders to offer much more favourable terms than they otherwise would to borrowers with imperfect credit or limited down payment savings.

The FHA doesn’t directly lend money; private banks and mortgage companies originate the loans while FHA insurance backs them. Borrowers pay mortgage insurance premiums both upfront and annually, which fund this insurance pool. This mutual benefit structure has enabled over thirty million Americans to achieve homeownership who would have been permanently excluded from traditional lending.

Understanding FHA loan Eligibility

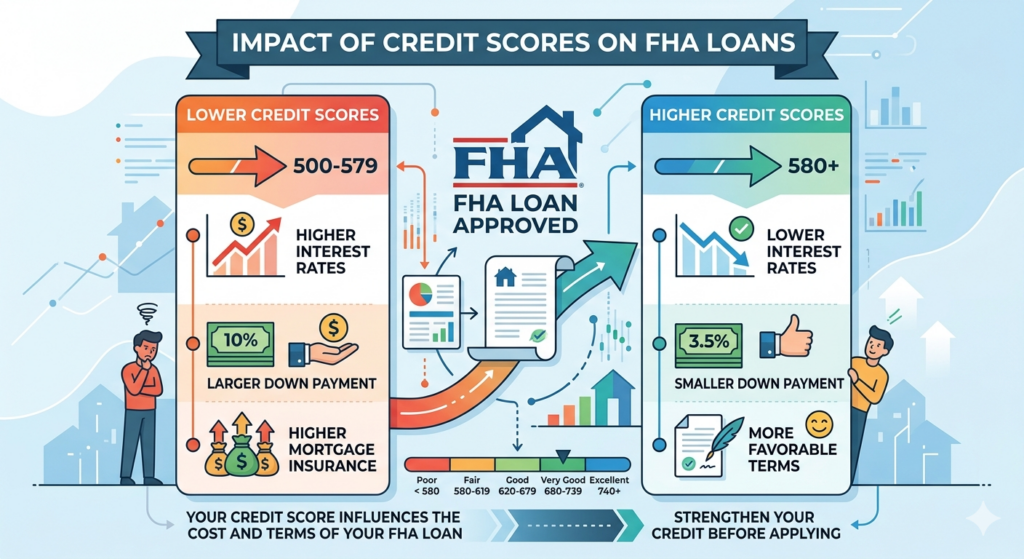

Requirements are crucial for prospective borrowers evaluating their qualification chances. The primary requirement mandates that borrowers use the property as their primary residence, distinguishing FHA loans from investment property financing. Credit score minimums typically hover around five hundred eighty points, significantly lower than conventional lending standards requiring seven hundred or higher.

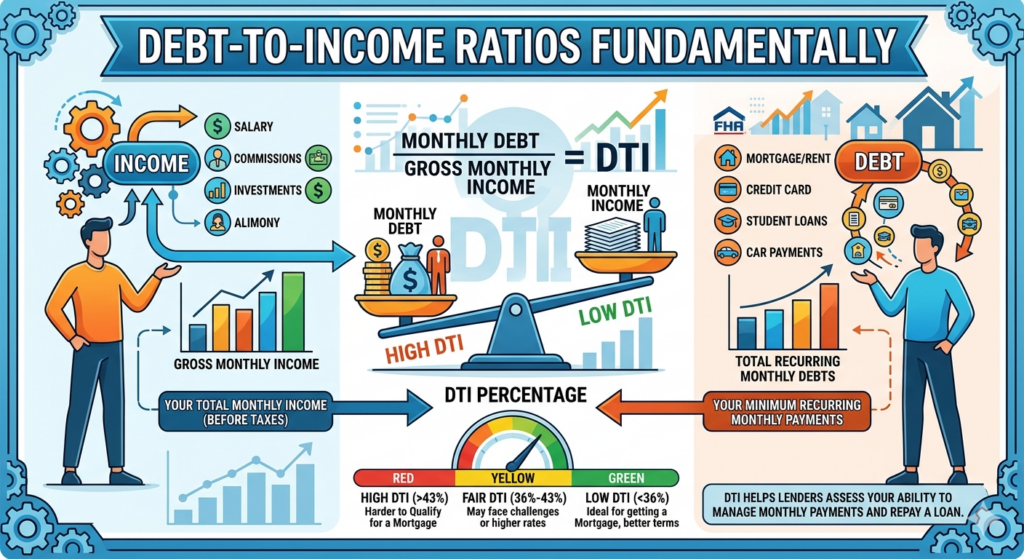

Debt-to-income ratios must generally remain below forty-three to fifty percent of gross monthly income, allowing flexibility for diverse financial situations. Income stability matters more than absolute income level, making the program accessible to modest earners. Employment history, savings patterns, and overall financial responsibility receive careful evaluation. These criteria balance risk management with accessibility.

Down payment Requirement Represents

One of FHA loans’ most revolutionary features enabling homeownership accessibility. Borrowers need only three and one-half percent of the purchase price as down payment, dramatically lower than conventional mortgage requirements of typically ten to twenty percent. This reduced requirement eliminates years of saving struggles for many families, accelerating the path to homeownership significantly.

Even more remarkably, the down payment can be a gift from family members, friends, or charitable organizations rather than the borrower’s own accumulated savings. First-generation homebuyers and young families particularly benefit from this feature. Gift letter documentation requirements ensure transparency but remain straightforward. This innovation specifically targets people historically excluded from wealth-building homeownership opportunities.

Mortgage insurance within FHA

Loans Comes in two distinct forms that borrowers must understand to calculate true borrowing costs accurately. The upfront mortgage insurance premium is assessed at closing, typically ranging from one to one point seven-five percent of the total loan amount. Most borrowers roll this insurance cost into their loan balance rather than paying it separately at closing, spreading payments across the loan term.

The annual mortgage insurance premium continues monthly throughout the loan’s entire life, ranging from zero point five-five to zero point eighty-five percent annually. Unlike conventional mortgages where insurance drops upon reaching twenty percent equity, FHA insurance persists permanently. Understanding these ongoing costs is essential for realistic budget planning and comparing total borrowing expenses across loan types.

Interest Rates on FHA Mortgages Typically

Remain competitive with conventional loans, varying based on current market conditions and individual borrower factors. Credit scores, loan-to-value ratios, property locations, and economic conditions influence the rates lenders offer. Borrowers with stronger credit histories generally receive better rates than those with marginal scores, though FHA borrowers consistently enjoy better rates than alternative lending options available to similar credit profiles.

The thirty-year fixed-rate mortgage has become standard for FHA loans, providing predictable monthly payments throughout the loan term. Fixed rates protect borrowers from interest rate fluctuations that plague adjustable-rate mortgages. Economic stability and financial predictability make fixed-rate mortgages ideal for most homebuyers planning long-term residency. Rate shopping among multiple lenders can save thousands in interest charges.

FHA properties Must Meet Specific Standards

Requirements designed to protect both lenders and borrowers from problematic investments. The property must be an owner-occupied single-family home, condominium, townhouse, or manufactured home meeting FHA construction standards. Investment properties, vacation homes, or rental properties do not qualify for FHA financing, restricting usage to primary residences. All properties undergo FHA appraisal by certified appraisers evaluating condition and market value thoroughly.

Structural integrity, roof condition, plumbing systems, electrical systems, heating and cooling functionality, and overall livability receive detailed assessment. Properties must be in satisfactory condition with no major defects threatening safety or habitability. This rigorous appraisal process protects borrowers from purchasing problematic properties while helping ensure property values support loan amounts.

FHA appraisal process Differs

Significantly from conventional appraisals in scope and stringency, reflecting the government’s investment in loan viability. Appraisers examine foundations for cracks or settling, inspect roofs for leaks or deterioration, and verify all major systems function properly. Properties with outstanding code violations, hazardous conditions, or environmental concerns may fail appraisal entirely. Minimum property requirements address livability, safety, and structural integrity comprehensively.

The appraisal also determines property value relative to the purchase price, ensuring the loan amount doesn’t exceed property worth. This protective mechanism prevents borrowers from overpaying for properties or taking loans exceeding real estate values. Clear title without liens or legal claims must also be verified before approval, ensuring the property belongs to the seller.

Pre-approval represents an Important

First step in the FHA mortgage process, providing valuable borrowing capacity information before property shopping begins. Lenders conduct preliminary financial reviews examining credit reports, income documentation, and savings history to estimate maximum borrowing power. Pre-approval strengthens buyers’ negotiating positions when making offers, demonstrating serious financial capability to sellers.

This initial assessment is not a final loan commitment but rather a preliminary indication of likely approval pending property appraisal and full underwriting. Pre-qualification differs from pre-approval as it’s less formal and doesn’t require documentation verification. The pre-approval letter typically remains valid for ninety days, allowing sufficient time for property search and negotiation. Obtaining pre-approval early in the homebuying process streamlines subsequent steps significantly.

Formal application process initiates

Serious FHA loan proceedings and requires comprehensive financial documentation from borrowers. Applicants submit recent tax returns typically covering two years, W-2 forms documenting employment history, recent pay stubs proving current income, and bank statements showing savings and financial stability. Self-employed borrowers provide additional documentation including profit-and-loss statements and business tax returns.

Explanation letters address any credit blemishes, income gaps, or unusual financial circumstances requiring clarity. Authorization forms allow lenders to verify employment and obtain credit reports. The application itself requests detailed personal, financial, and employment information used throughout underwriting. Accuracy and honesty in applications are paramount, as false information can result in loan denial or legal consequences.

Underwriting represents the critical phase

Where lenders thoroughly evaluate borrower creditworthiness and loan viability before committing funds. Underwriters review all submitted documentation, verify employment and income, and analyze credit reports for payment history patterns. They calculate precise debt-to-income ratios considering all monthly obligations and proposed mortgage payments.

Property appraisals are ordered during underwriting, and results are carefully reviewed against purchase prices. Asset verification confirms savings, investments, and down payment source legitimacy. Underwriters may request additional documentation addressing concerns or clarifications. Underwriting timelines typically span five to ten business days, though complex situations may require additional time. Clear underwriting approval provides loan commitment and moves borrowers toward closing significantly.

Credit scores significantly impact FHA loans

Approvals and the interest rates borrowers receive, making credit understanding important for applicants. The minimum five hundred eighty score requirement still allows approval for borrowers with challenging credit histories, though higher scores receive better terms. Credit reports document payment history, outstanding debts, accounts in collection, and other financial behaviors lenders analyze. Recent delinquencies, bankruptcies, and foreclosures require explanation through letter documentation.

Lenders understand that financial hardships sometimes affect credit temporarily, particularly job loss, medical emergencies, or divorce. Explaining circumstances honestly and demonstrating subsequent financial responsibility strengthen applications. Borrowers should request free credit reports, verify accuracy, and dispute errors before applying. Improving credit scores before application sometimes makes approval easier or secures better rates.

Debt-to-income ratios fundamentally

Determine borrowing capacity within FHA lending parameters and vary based on individual lender requirements. The maximum debt-to-income ratio typically hovers around forty-three per cent, though some lenders extend it to fifty per cent for compensating factors. This ratio divides total monthly debt obligations, including the proposed mortgage, by gross monthly income.

Existing debts like auto loans, credit cards, student loans, and other obligations count toward debt calculations. Eliminating or reducing existing debts before applying can improve debt-to-income ratios significantly. Part-time income and bonuses may be included if documented and demonstrated as stable. Overtime income requires careful documentation proving consistency and likelihood of continuation. Self-employed borrowers face more rigorous income verification requirements.

Gift funds for down payments offer

Tremendous advantage for first-generation homebuyers and young families establishing initial property ownership. Parents, grandparents, or other relatives can gift down payment funds without expectation of repayment, differentiating gifts from loans. Gift letter documentation must state the gift nature, amount, and relationship between giver and recipient. Most lenders prohibit loans disguised as gifts, making honest disclosure essential.

The gift must come from identified sources, typically family members or charitable organizations. Donor account statements may be required verifying available funds and demonstrating legitimate source. Gifts dramatically reduce required borrower savings, enabling homeownership when saving twenty percent down payments would require years. This feature particularly benefits younger generations and those from modest economic backgrounds.

Closing represents the final FHA loan

Stage where all documents are signed, funds transfer, and property ownership changes hands officially. Title companies or closing attorneys coordinate closing procedures, ensuring all legal documents are properly executed. Borrowers review and sign the promissory note obligating loan repayment, mortgage documents securing the lender’s interest in property, disclosure documents revealing loan terms and costs, and numerous other required paperwork.

Final loan cost disclosure documents itemize all fees including origination charges, appraisal costs, title insurance, and insurance premiums. Homeowners insurance proof is required before closing, protecting lender interest in the property. The down payment and closing costs are wired to escrow accounts, remaining there until all conditions are satisfied. After all signatures and fund transfers complete, the borrower receives keys and becomes the owner officially.

FHA loans offer significant advantages

Compared to conventional mortgages for borrowers facing credit or financial challenges. The lower credit score requirements make approval possible for those with imperfect payment histories from past difficulties. Reduced down payment obligations eliminate the need to accumulate twenty or thirty percent of purchase prices. Gift fund eligibility removes savings barriers for many working families. More flexible debt-to-income ratios accommodate those with student loans or other obligations.

Fixed-rate mortgages provide payment stability and protection from interest rate increases. Government insurance backing creates lender confidence in providing favorable terms. These combined advantages have enabled millions of Americans to achieve homeownership and build generational wealth. For many households, FHA loans represent the only realistic pathway to property ownership.

Limitations and considerations of FHA loans

Deserve honest acknowledgment alongside their significant advantages and accessibility benefits. Mortgage insurance premiums increase total borrowing costs substantially compared to conventional loans without insurance. Annual insurance premiums persist throughout the loan term unlike conventional insurance that eventually lapses.

The upfront insurance premium adds to the initial loan amount, meaning borrowers pay interest on this additional cost. Debt-to-income ratio limits, while flexible, still constrain maximum borrowing amounts for lower-income borrowers. Property condition requirements eliminate opportunities to purchase fixer-uppers needing significant renovation. Maximum loan limits vary by geographic area, potentially restricting purchases in expensive real estate markets. Understanding these trade-offs helps borrowers make informed decisions about whether FHA loans suit their circumstances.

Conclusion

Future homeownership success with FHA loans depends on responsible financial management and realistic budget planning from the outset. Borrowers should calculate total monthly obligations including principal, interest, property taxes, homeowners insurance, and mortgage insurance premiums realistically. Building an emergency savings fund covering three to six months of expenses provides security against unexpected hardships.

Maintaining consistent mortgage payments demonstrates financial responsibility and builds equity steadily. Avoiding additional debt accumulation helps maintain healthy debt-to-income ratios and financial stability. Staying current on all obligations protects credit scores and demonstrates reliability to lenders. Regular property maintenance preserves the home investment and prevents costly future repairs. FHA loans represent the beginning of the homeownership journey, not the finish line, requiring ongoing commitment and responsible stewardship.

: Compare Top Options")