Mortgage Lenders: Understanding Your Path to Homeownership

When you decide to buy a home, one of the most important decisions you will make is choosing the right mortgage lender. A mortgage lender is a financial institution or individual that provides the money you need to purchase a property. Understanding how mortgage lenders work and what they offer can help you make an informed decision that will benefit you for years to come.

What Are Mortgage Lenders?

Mortgage lenders are entities that loan money to borrowers who want to purchase real estate. These lenders assess your financial situation, determine how much money they are willing to lend you, and set the terms of your loan. The home you purchase serves as collateral for the loan, which means the lender can take back the property if you fail to make your monthly payments.

Mortgage lending is a significant part of the financial industry, and lenders range from large national banks to smaller local institutions. Each type of lender has different strengths and can offer various benefits depending on your personal circumstances and financial goals.

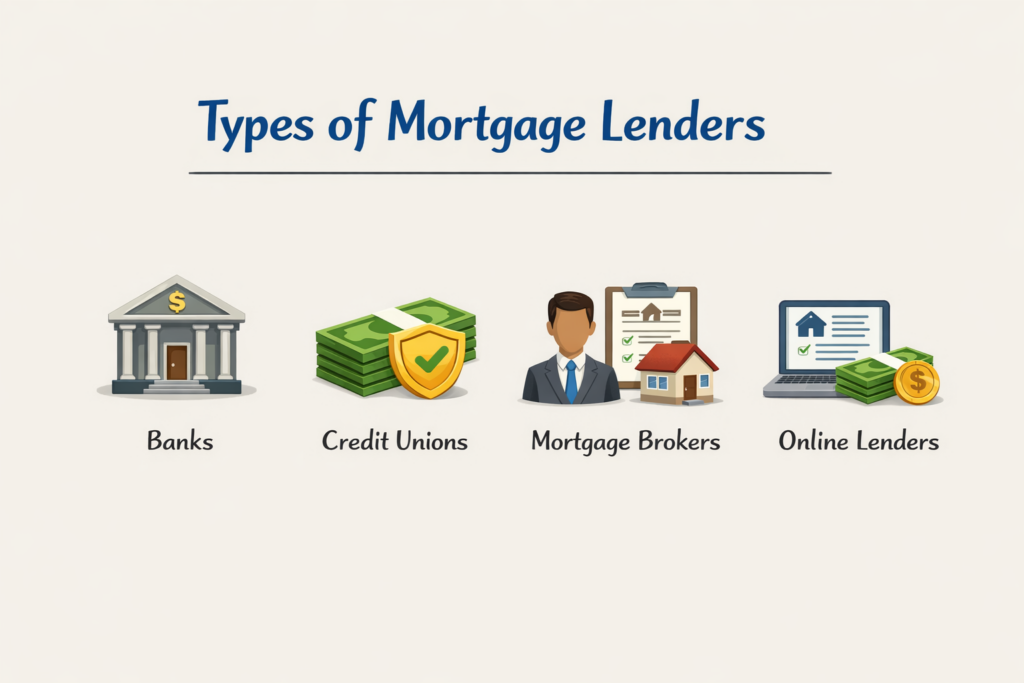

Types of Mortgage Lenders

Banks are among the most traditional mortgage lenders. They have been providing home loans for many years and often offer competitive rates, especially if you have good credit and a stable income. Banks typically require thorough documentation and follow strict lending guidelines. Working with a bank can give you peace of mind knowing you are dealing with an established institution that is regulated by government agencies.

Credit unions represent another source for mortgage lending. Credit unions are membership-based organizations that often provide loans at lower rates than banks. If you are a member of a credit union, you may qualify for better terms and more personalized service. Credit unions tend to work more closely with borrowers and may be more flexible with their lending standards.

Mortgage brokers work differently than direct lenders. Instead of lending you their own money, brokers connect you with various lenders and help you find the best loan options for your situation. Mortgage brokers have access to multiple lenders and loan programs, which can give you more choices. However, you need to be aware that brokers earn commissions from lenders, which could potentially influence their recommendations.

Online lenders have become increasingly popular in recent years. These companies operate primarily through the internet and often have lower overhead costs than traditional banks. Online lenders can sometimes offer faster approval processes and more convenient application procedures. However, you should research online lenders carefully to ensure they are legitimate and properly licensed.

How Mortgage Lenders Evaluate Your Application

When you apply for a mortgage, lenders examine several factors to determine whether to approve your loan and what interest rate to offer. Understanding these factors can help you strengthen your application.

Your credit score is one of the most important considerations for mortgage lenders. This three-digit number reflects your history of borrowing and repaying money. Lenders use your credit score to assess the risk of lending to you. A higher credit score typically means you will qualify for better interest rates and more favorable loan terms. Most lenders prefer borrowers with a credit score of at least 620, though scores above 740 usually qualify for the best rates.

Income verification is another crucial element. Lenders want to ensure you have sufficient income to make your monthly mortgage payments. They typically review your recent tax returns, pay stubs, and employment verification. Self-employed individuals may need to provide additional documentation to prove their income stability.

The amount of money you have saved for a down payment matters significantly. Lenders generally require a down payment of between 3 and 20 percent of the home’s purchase price. A larger down payment shows the lender that you are financially committed to the purchase and reduces their risk. It can also help you avoid paying private mortgage insurance.

Your debt-to-income ratio is the percentage of your gross monthly income that goes toward debt payments. Lenders calculate this by adding all your monthly debt obligations, including the potential mortgage payment, and dividing by your gross monthly income. Most lenders prefer a debt-to-income ratio below 43 percent, though some may accept higher ratios under certain circumstances.

Employment history and job stability also influence lending decisions. Lenders prefer to see that you have maintained stable employment. Frequent job changes or gaps in employment might raise concerns about your ability to maintain steady income.

The type of property you want to purchase can affect lending decisions. Lenders may have different requirements for single-family homes, condominiums, investment properties, or other real estate types.

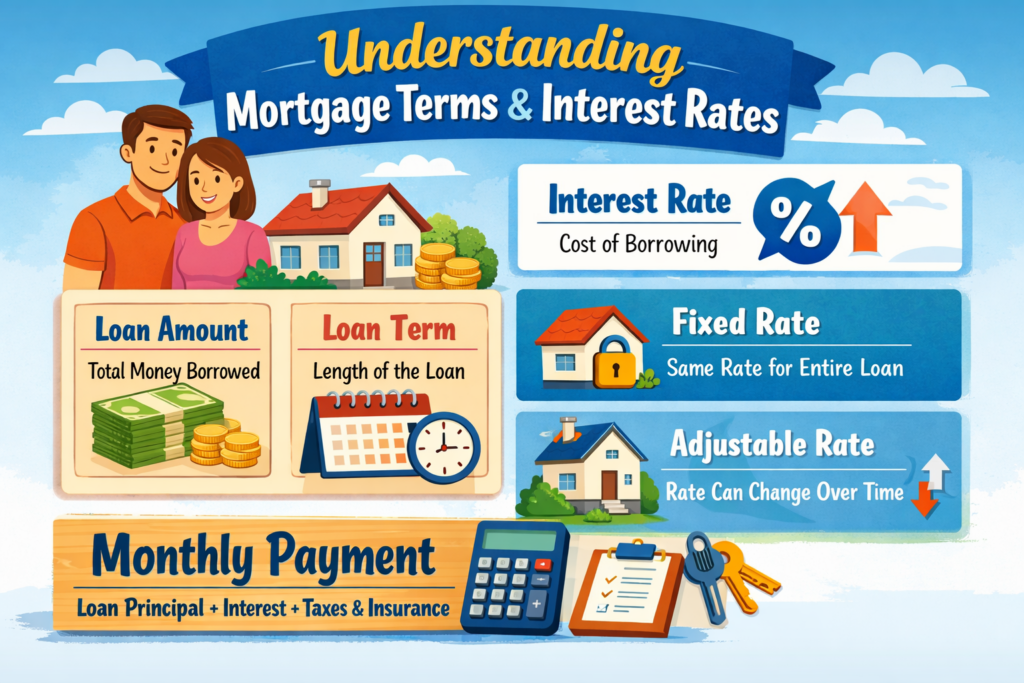

Understanding Mortgage Terms and Interest Rates

Mortgage lenders offer various loan products with different terms and interest rates. The interest rate is the percentage of your loan amount that you pay annually to the lender. This rate significantly impacts the total amount you will pay over the life of your loan.

Fixed-rate mortgages keep the same interest rate for the entire loan period. If you secure a fixed rate of 5 percent, your rate remains 5 percent for 15, 20, or 30 years, depending on your loan term. This type of mortgage provides stability and predictability because your monthly payment stays the same throughout the loan.

Adjustable-rate mortgages start with a lower initial interest rate that changes periodically based on market conditions. These loans typically offer lower initial payments, but your rate and payment could increase significantly when the adjustment period begins. Adjustable-rate mortgages are riskier for borrowers but might be appropriate if you plan to sell or refinance before the rate adjusts.

The loan term, or the number of years you have to repay the loan, is another important factor. Thirty-year mortgages are the most common, offering lower monthly payments but higher total interest paid over the life of the loan. Fifteen-year mortgages require higher monthly payments but allow you to build equity faster and pay significantly less interest overall.

What to Look for When Choosing a Mortgage Lender

Selecting the right mortgage lender requires careful consideration of several factors beyond just interest rates. Shopping around and comparing offers from multiple lenders is essential. Most lenders will provide you with a loan estimate that shows the interest rate, closing costs, and monthly payment. Comparing these estimates side by side helps you understand the true cost of borrowing from each lender.

The reputation and reliability of a lender matters greatly. Research customer reviews, check their licensing status with state regulatory agencies, and verify they are not involved in any legal disputes. Reading feedback from other borrowers can provide valuable insights into the lender’s customer service quality and whether they deliver on their promises.

Customer service quality should not be overlooked. You will work with your lender throughout the application process and potentially for many years if you maintain your mortgage. A lender who responds promptly to your questions, explains terms clearly, and guides you through the process makes the experience much smoother.

The availability of different loan products is important if your financial situation is unique. Some lenders specialize in working with borrowers who have credit challenges, irregular income, or other special circumstances. Finding a lender with products that match your needs increases your chances of approval.

Closing costs are fees charged by the lender and third parties involved in the mortgage process. These can include appraisal fees, credit report fees, origination fees, and attorney fees. Some lenders offer better closing cost deals than others, so comparing these expenses is worthwhile. In some cases, you may be able to negotiate closing costs or have the lender cover some expenses.

The speed of the approval process can be important if you are under a tight timeline. Traditional banks may take longer to approve loans, while online lenders and some mortgage brokers may move faster. However, speed should not come at the expense of working with a reputable lender.

Common Mistakes When Working with Mortgage Lenders

Many people make mistakes that cost them money when borrowing from mortgage lenders. One common error is not checking your credit report before applying. If there are errors on your credit report, correcting them before applying can result in a better interest rate and save you thousands of dollars over the life of the loan.

Another mistake is applying for credit shortly before or during the mortgage application process. Each credit inquiry can lower your credit score slightly, and multiple inquiries can add up. It is best to avoid applying for new credit for at least six months before and during your mortgage application.

Overestimating how much you can afford is another frequent problem. Just because a lender approves you for a certain amount does not mean you should borrow the maximum. Consider your budget carefully and choose a mortgage payment that leaves you comfortable room for other expenses and savings.

Failing to understand the terms of your loan can lead to problems down the road. Make sure you fully understand whether your rate is fixed or adjustable, what your monthly payment will be, and what closing costs you will pay. Do not hesitate to ask questions about anything you do not understand.

Some borrowers ignore the importance of getting preapproved before house hunting. Preapproval shows sellers that you are a serious buyer and helps you understand your budget. It also locks in an interest rate for a certain period, protecting you if rates rise while you are searching for a home.

The Importance of Comparing Multiple Lenders

Taking time to contact multiple mortgage lenders and compare their offers is one of the best investments you can make. The difference between interest rates offered by different lenders can be significant. Even a difference of one-half percent in interest rate means thousands of dollars over a 30-year loan.

When comparing lenders, make sure you are comparing similar loan products. A 30-year fixed-rate mortgage from one lender should be compared with the same product from other lenders. Ask each lender for a detailed loan estimate that breaks down all fees and charges.

Shopping for mortgage lenders typically does not hurt your credit score significantly if you do it within a two-week period. Credit reporting agencies understand that borrowers shop around for mortgages, and they count multiple inquiries within this window as a single inquiry.

Technology and Mortgage Lending

Technology has transformed how mortgage lenders operate and how borrowers access their services. Many lenders now offer online applications that can be completed from your home at any time of day. Digital documentation reduces the amount of paperwork and speeds up the approval process.

Some mortgage lenders use technology to provide real-time loan status updates so you can track your application progress. Others offer tools that help you calculate monthly payments, compare loan products, and estimate closing costs.

However, while technology can improve efficiency, ensure that the lender you choose uses secure systems to protect your personal and financial information. Cybersecurity is essential when dealing with sensitive financial data online.

The Future of Mortgage Lending

The mortgage lending industry continues to evolve as lenders find new ways to serve borrowers more efficiently. Increased competition has driven lenders to improve their service offerings and find ways to reduce costs. Many experts expect to see continued growth in online lending as more borrowers become comfortable with digital processes.

Additionally, there is increasing focus on helping borrowers with diverse financial situations access home loans. More lenders are developing products for first-time homebuyers, self-employed individuals, and those with previous credit challenges.

Conclusion

Choosing a mortgage lender is one of the most significant financial decisions you will make. Whether you work with a traditional bank, credit union, mortgage broker, or online lender, the key is to do your research and compare offers from multiple sources. Understanding how mortgage lenders evaluate applications, what factors affect your interest rate, and what terms mean will help you make a decision that serves your financial interests.

Take time to improve your credit score before applying, gather necessary documentation, and get preapproved with multiple lenders. Compare loan estimates carefully, paying attention not just to interest rates but also to closing costs and loan terms. Ask questions about anything you do not understand, and choose a lender whose customer service and reliability match your needs.

Working with the right mortgage lender can help you achieve your goal of homeownership while keeping your long-term financial health in mind. The effort you invest in finding the right lender at the right terms will benefit you for decades to come.