Mortgage Amortization Explained 2026 How It Works and What It Costs

Most people sign a mortgage and never look at their amortization schedule again. That is an expensive mistake. Your amortization schedule is not just paperwork the lender hands you at closing. It is the actual roadmap of where every dollar you send to your lender goes for the next 15 to 30 years, and understanding it can change how you manage your loan, how fast you build equity, and how much you ultimately pay for your home.

Mortgage amortization explained simply: it is the process of paying off your loan in fixed monthly installments, where each payment covers both the interest your lender charges and a portion of the money you originally borrowed, known as the principal. The payment amount stays the same every month, but what changes is the split between interest and principal inside that payment. In the early years, almost all of it goes to interest. By the final years, almost all of it goes to principal.

That shift sounds straightforward. The reality of what it means for your money, and how you can use it to your advantage, is what this guide is actually about.

What a Mortgage Amortization Schedule Actually Shows You

A mortgage amortization schedule is a table that shows how each monthly loan payment is divided between principal and interest payments, along with your remaining loan balance after every payment. Homeplusaz

Your lender is required to provide this schedule, and most loan origination software generates it automatically. You can also request it before closing so you know exactly what you are agreeing to before you sign anything. I would strongly recommend asking for it. Looking at month-by-month payment breakdowns on a $350,000 or $450,000 loan has a way of making the math feel very real, very fast.

Every row on the schedule includes four pieces of information: the payment number, the interest portion of that payment, the principal portion of that payment, and the remaining loan balance after the payment is applied. A standard 30-year mortgage has 360 rows. A 15-year mortgage has 180. Each row tells you exactly what that specific payment accomplished.

One thing to note upfront: the amortization schedule only covers principal and interest. Your actual monthly mortgage payment usually includes escrow contributions for property taxes and homeowners insurance. Those amounts do not appear on the amortization schedule because they are separate from the loan payoff itself. When you compare your actual monthly payment to the schedule, the numbers will not match exactly. The schedule tracks the loan. Your real payment includes everything. LendingTree

How Your Payment Splits Between Interest and Principal: The Real Numbers

This is where most buyers get a genuine shock the first time they look carefully at an amortization schedule.

Take a $350,000 loan at 6.625% on a 30-year term, which is close to current average rates. The monthly principal and interest payment on a $350,000 30-year fixed loan at 6.625% is approximately $2,241 per month. Arizonadownpaymentassistance

Here is what that first payment actually does:

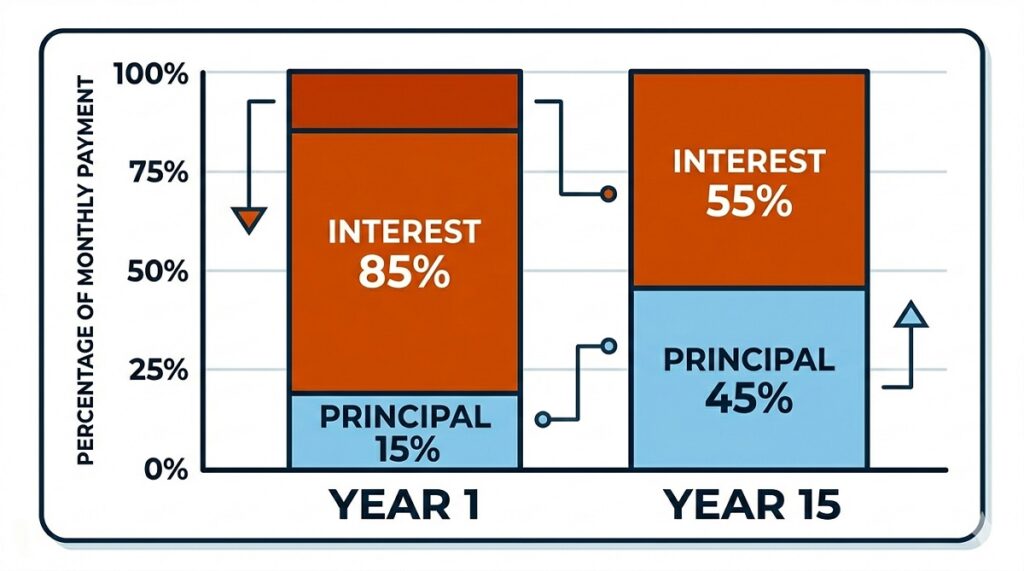

Your monthly interest charge in month one is your outstanding balance multiplied by your annual interest rate, then divided by 12. On $350,000 at 6.625%, that equals $350,000 times 0.06625, divided by 12, which comes to $1,932. So in month one, $1,932 of your $2,241 payment goes to interest, and only $309 reduces your actual loan balance.

You paid $2,241. You owe $349,691. You built $309 in equity from that payment.

In the early years of the mortgage, a larger portion of the monthly payment goes toward interest. As the loan balance shrinks over time, the interest amount decreases and more goes toward reducing the principal, even though the monthly payment stays the same. This gradual shift is what makes amortization such an important concept to understand. LendingTree

By year 15 of that same loan, your outstanding balance has dropped to around $248,000. Your interest charge that month is now $248,000 times 0.06625 divided by 12, which equals roughly $1,370. That means $871 of your payment now goes to principal instead of $309. Same payment. Completely different result.

By month 355, your outstanding balance is below $12,000. Almost your entire $2,241 payment is now reducing the principal. The lender is collecting almost nothing in interest at that point because the math no longer favors them.

To calculate amortization manually, multiply your principal balance by your interest rate, then divide by 12 to get your monthly interest charge. Subtract that from your total payment to find how much goes to principal that month. Most buyers never do this, but doing it once for your own loan removes any mystery about where your money is going. FHA.com

Use our free mortgage calculator to generate a full payment breakdown for your specific loan amount, rate, and term, and see exactly what each payment accomplishes over the life of your mortgage.

How to Read Your Amortization Schedule Without Confusion

When your lender hands you a printed amortization schedule or you pull one up online, here is what to look at and why it matters.

Look at month one versus month 60. At month 60, your five-year anniversary of homeownership, check how much your principal balance has actually dropped on a 30-year loan. Most buyers are surprised to discover that after five years of payments on a $350,000 loan at 6.625%, their balance sits around $325,000. They have paid roughly $134,000 in total payments and still owe $325,000. That is not a mistake. It is exactly how front-loaded amortization works. Most of those payments covered interest.

Look at the halfway point. On a 30-year mortgage, most buyers assume their balance is roughly half gone at year 15. It is not. Because so much of the early payments go toward interest, your loan balance at the halfway point of a 30-year mortgage is typically still around 70% of the original loan amount, not 50%. That gap between perceived progress and actual progress is one of the most important things amortization reveals. Rocket Mortgage

Look at the total interest line at the bottom. A $300,000 loan at 7% on a 30-year term accumulates over $418,000 in total interest charges across the life of the loan. That means for every $100 borrowed, the borrower pays back $239, more than double the original amount. Seeing that number before closing is worth the five minutes it takes to review the schedule. Innago

How Extra Payments Rewrite Your Amortization Schedule

This is the most practical and financially impactful section of this entire guide. Extra payments are the single most powerful tool a homeowner has to reduce total interest and pay off their loan years ahead of schedule.

Here is why: every extra dollar you pay toward principal immediately reduces the balance that future interest is calculated on. Unlike your regular payment, which the lender applies partly to interest first, an extra payment designated to principal skips the interest calculation entirely and goes straight to reducing what you owe.

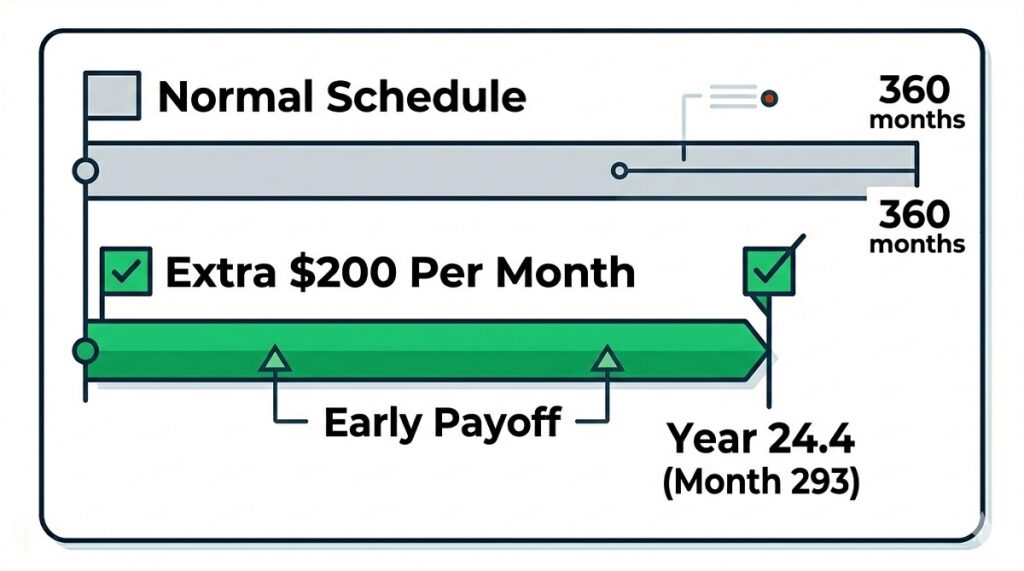

Paying an extra $200 a month on a $405,000 fixed-rate loan at 6.625% on a 30-year term could save over $115,000 in total interest and shorten the loan from 360 months down to 293 months, nearly five and a half years early. That is $200 per month producing $115,000 in savings. No investment account offers that kind of guaranteed return. FHA Mortgage Source

Here is a simpler version on a smaller loan. On a $250,000 mortgage at 5%:

Adding $50 per month saves approximately $21,298 in interest and pays the loan off two years and four months early.

Adding $100 per month saves approximately $26,500 in interest and cuts the loan term by more than four and a half years.

Adding $200 per month saves approximately $44,000 in interest and shortens the term by over eight years.

Extra payments are more valuable early in the loan. If you start making $100 extra monthly payments from year one, you save significantly more than if you start the same extra payments in year six, because the earlier you reduce the principal, the less interest compounds against a higher balance over time. Houzeo

Lump sum payments work the same way. A one-time $5,000 payment toward principal in month 13 of a 30-year loan saves roughly $10,000 in interest and removes 31 months from the loan term. The same $5,000 payment made in year six saves only $7,944 and removes 27 months. Earlier is always better. Every month you wait, the compounding interest on that unpaid balance grows larger. Houzeo

One practical strategy that requires no extra budget: biweekly payments. Instead of making 12 monthly payments per year, you make a half-payment every two weeks. Because there are 26 biweekly periods in a year, this produces 13 full payments instead of 12, essentially adding one extra payment per year with no noticeable budget impact. Making one extra mortgage payment per year on a $350,000 loan at 6.625% pays off the loan five years and nine months early compared to the standard schedule. Norada Real Estate

Before switching to biweekly payments, confirm with your lender that they accept and properly apply biweekly payments toward principal. Some servicers hold the half-payment in a holding account until the second half arrives, which eliminates any benefit from the strategy. Ask specifically how they process it.

Use our free refinance calculator to model how extra payments affect your break-even and payoff timeline, especially if you are deciding between making extra payments on your current loan versus refinancing to a lower rate.

15-Year vs 30-Year Mortgage: What the Amortization Difference Actually Costs

The choice between a 15-year and 30-year mortgage is fundamentally an amortization decision. The same loan amount amortizes on a completely different schedule depending on which term you choose, and the financial difference is enormous.

On a $350,000 loan:

The average 30-year fixed mortgage rate as of early 2026 is approximately 6.165%, and the 15-year fixed rate is approximately 5.477%. That rate difference exists because shorter-term loans carry less risk for lenders. The Truth About Mortgage

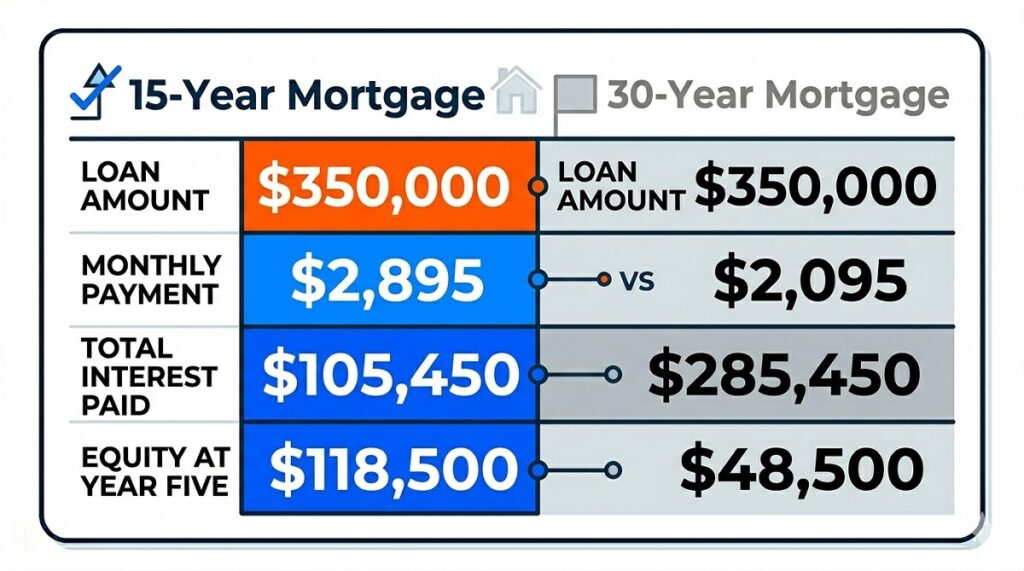

At 6.165% on a 30-year term, the monthly payment on $350,000 is roughly $2,129, and total interest paid over 30 years is approximately $416,000.

At 5.477% on a 15-year term, the monthly payment on the same $350,000 is roughly $2,861, and total interest paid over 15 years is approximately $165,000.

The 15-year mortgage costs $732 more per month. But it saves approximately $251,000 in total interest and delivers a mortgage-free life 15 years earlier.

Monthly principal and interest payments on a 15-year fixed-rate mortgage run about 30% higher than on a 30-year home loan. That 30% increase is the honest cost of the shorter term. For buyers who can comfortably absorb that higher payment within their budget and DTI (debt-to-income ratio, meaning total monthly debts divided by gross monthly income), the 15-year term is almost always the better long-term financial decision. Zillow

The 30-year term makes more sense when the monthly savings from the lower payment are genuinely needed, when a buyer plans to invest the payment difference in higher-returning assets, or when the budget simply cannot support the higher 15-year payment without financial strain. The wrong answer is choosing the 30-year term by default without running the numbers. Use our affordability calculator to see which term fits your monthly budget before deciding.

ARM Loans and Amortization: Where It Gets Complicated

Fixed-rate mortgages follow a predictable amortization path. Adjustable-rate mortgages, known as ARMs, follow a path that can shift significantly when the rate adjusts.

Amortization schedules for adjustable-rate mortgages show predictable decreases in interest during the fixed-rate period, but once the rate adjusts, the schedule recalculates based on the new rate and remaining balance. This means the principal and interest split changes at every adjustment, and total interest paid can increase substantially if rates rise. The Truth About Mortgage

A 5/1 ARM gives you five years of fixed-rate stability before adjusting annually. Your amortization schedule for those first five years looks exactly like a fixed-rate schedule. In year six, if the rate jumps from 6% to 8%, your monthly payment recalculates upward, and the interest portion of that payment jumps sharply again, temporarily slowing your principal paydown.

For buyers who plan to sell or refinance before the fixed period ends, an ARM’s amortization risk is minimal because they never reach the adjustment phase. For buyers who end up staying longer than planned, the amortization can become genuinely unpredictable.

Negative Amortization: When Your Balance Grows Instead of Shrinks

This is a concept most buyers never encounter, but it is worth understanding because certain loan structures can create this situation, and the consequences are severe.

Negative amortization occurs when a mortgage payment is not large enough to cover the monthly interest charge. The unpaid interest gets added to the loan balance instead of subtracted, meaning the borrower owes more at the end of the month than at the beginning, even after making a payment. JVM Lending

Some older loan types from the pre-2008 era, like payment option ARMs, allowed borrowers to choose a minimum payment that did not cover full interest. Balances grew for years before suddenly requiring sharply higher payments. These products largely disappeared after the 2008 financial crisis and are not common today.

However, negative amortization can still technically occur if a borrower on an ARM loan has a payment cap that prevents the payment from rising enough to cover interest when the rate adjusts significantly upward. If your ARM has a payment cap, ask your lender specifically whether your loan can negatively amortize and under what conditions.

For the vast majority of today’s buyers using standard fixed-rate or straightforward ARM products, negative amortization is not a risk. But if you are looking at any loan that offers a minimum payment option below the standard calculated payment, read the terms carefully before signing.

How Amortization Affects When You Can Drop PMI

Private mortgage insurance, or PMI, is a monthly fee conventional borrowers pay when their down payment is less than 20% of the home’s purchase price. Amortization directly determines when you can legally request its removal.

Under the federal Homeowners Protection Act, lenders must automatically cancel PMI when your loan balance reaches 78% of the original purchase price based on your scheduled amortization. You can request cancellation earlier, at the 80% threshold, either through scheduled payments reaching that level or through your home appreciating in value and a new appraisal confirming it.

On a $350,000 home purchased with 10% down, your starting loan balance is $315,000. To reach 80% of the original $350,000 purchase price, you need to get your balance down to $280,000. On a 30-year loan at 6.625%, your amortization schedule shows that reaching $280,000 takes roughly 12 to 13 years of standard payments. Making even modest extra payments toward principal can significantly accelerate that milestone.

Knowing your amortization schedule lets you identify exactly which month you cross the 80% threshold and plan your PMI cancellation request strategically rather than waiting for the lender to cancel it automatically at 78%.

Use our DTI calculator to see how dropping PMI affects your debt-to-income ratio once your balance hits the 80% threshold, which can be useful information if you are planning any future refinancing or borrowing.

Amortization and Refinancing: What Most Homeowners Miss

Refinancing resets your amortization schedule. That sounds neutral. It is not always good news.

When you refinance a 30-year mortgage in year eight and replace it with a new 30-year loan, you start over at the front of a new amortization schedule where most of your payment goes to interest again. You have effectively given up eight years of principal-building progress and committed to another 30 years.

That does not mean refinancing is wrong. If you drop your rate from 7.25% to 5.75%, the monthly savings can far outpace the cost of restarting the amortization clock. But the break-even calculation has to account for both the rate savings and the additional interest cost of extending your total repayment period.

The smarter approach when refinancing is to choose a term shorter than your remaining balance. If you have 22 years left on your current mortgage, refinancing into a 20-year loan at a lower rate captures the rate savings without significantly extending your payoff date. You still restart the amortization schedule at the front-loaded interest stage, but the shortened term limits the total interest exposure.

Understanding amortization allows you to estimate long-term costs, know how fast you will build equity, and make informed decisions about loan types and repayment strategies. Nowhere is that truer than in a refinancing decision. The Truth About Mortgage

Use our free refinance calculator to model the true long-term cost of any refinance scenario, including the effect of restarting your amortization schedule, before committing to a new loan.

And if you want to see your current mortgage rate versus what is available today, our mortgage rate comparison tool shows you exactly where market rates sit right now so you can judge whether a refinance even makes sense to pursue.

A Quick-Reference Summary

Amortization is the process of paying off a loan in fixed monthly installments, with each payment split between interest and principal.

In month one of a $350,000 loan at 6.625%, roughly $1,932 goes to interest and only $309 reduces your balance.

By the end of the loan, almost the entire payment reduces principal because the balance has shrunk so much.

Your amortization schedule shows every payment across the life of the loan. Ask your lender for it before closing.

Extra payments toward principal immediately reduce future interest because they lower the balance that interest is calculated on.

Adding $200 per month to a $405,000 loan at 6.625% saves over $115,000 and cuts 5.5 years from the term.

A 15-year mortgage pays roughly $251,000 less in total interest than a 30-year mortgage on the same $350,000 loan at current rates, but costs about $732 more per month.

Refinancing resets your amortization schedule. Factor in the cost of restarting front-loaded interest when calculating whether a refinance truly saves money.

PMI drops when your balance reaches 80% of the original purchase price. Your amortization schedule tells you exactly which month that happens.

DISCLAIMER BLOCK

This article is for informational purposes only and does not constitute financial or legal advice. Mortgage rates, loan limits, and program requirements change frequently. All calculations shown are estimates based on fixed-rate assumptions and standard amortization formulas. Always consult a licensed mortgage professional before making decisions about your loan term, refinancing, or repayment strategy.