How Much House Can I Afford on 60k Salary in 2026

If you are earning $60,000 a year and wondering whether homeownership is actually within reach, the honest answer is yes, it is, but only if you go in with accurate numbers rather than the oversimplified rules you will find on most financial websites.

How much house can I afford on a 60k salary is one of the most searched mortgage questions in America, and the answers most people find online range from vague to genuinely misleading. Some sites say $180,000. Others say $300,000. The real answer depends on five things: your monthly debts, your credit score, your down payment, the current mortgage rate, and the hidden costs of homeownership that almost nobody mentions until after you have already committed.

The national median home price sits at $435,285 in 2026, and the median US household income is $83,730, which means a $60,000 salary is below the national median. That context matters because it tells you straight away that a $60,000 buyer is not going to be shopping the national median price range. But in most of the country, you do not need to. There are real, livable, quality homes available in the price range your salary can support, and there are loan programs specifically designed to help buyers at your income level get there. FHA Mortgage Source

Let me walk through the actual math, the actual programs, and the actual costs so you can make a decision grounded in reality.

The 28/36 Rule Applied to a 60k Salary: Real Numbers

Before any lender calculator or pre-approval letter, you need to understand the framework lenders use to decide how much they will let you borrow. The most widely used standard is the 28/36 rule.

The 28/36 rule holds that you should spend no more than 28% of your gross monthly income on your housing payment, and no more than 36% of your gross monthly income on total debt obligations including mortgage, car payments, student loans, and credit cards. Arizonadownpaymentassistance

Applied to a $60,000 salary, the math is straightforward.

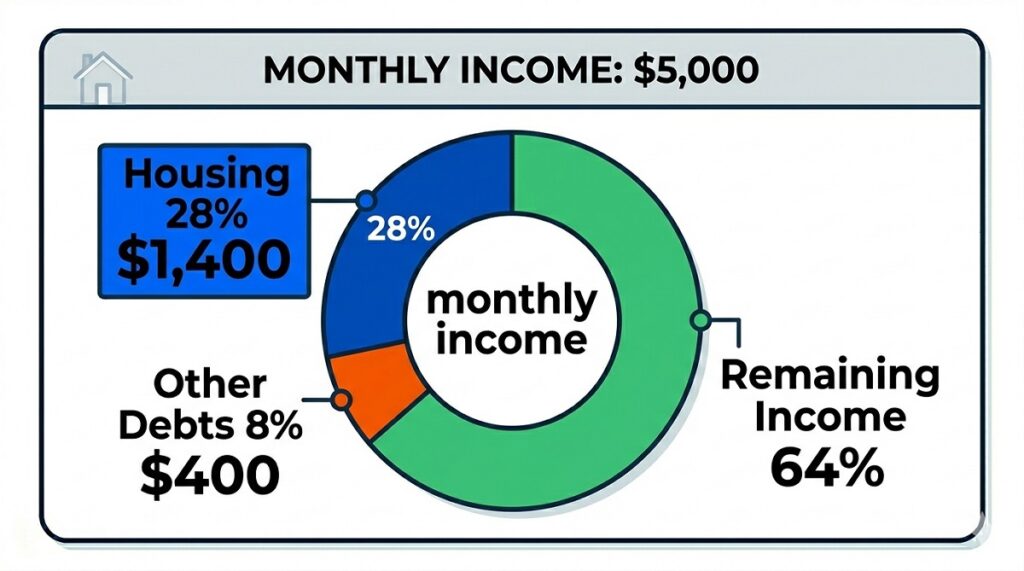

$60,000 divided by 12 equals $5,000 gross monthly income.

$5,000 multiplied by 28% equals $1,400. That is your maximum target monthly housing payment, including principal, interest, property taxes, homeowners insurance, and PMI if applicable.

$5,000 multiplied by 36% equals $1,800. That is your maximum total monthly debt obligation. If your car payment is $350 and your student loan is $200, your combined non-housing debt is $550. Subtract that from $1,800 and you have $1,250 left for your mortgage payment, not $1,400.

This is where a lot of buyers miscalculate. They see the $1,400 figure and assume that is what they can spend on housing. The 36% total debt ceiling is the binding constraint once you have existing debts. If you are carrying $500 or more in monthly debt payments, your realistic housing budget is meaningfully lower than the 28% calculation suggests.

Many lenders will go higher than 36% on total debt in 2026. FHA and VA loans are known for allowing higher debt ratios, with some lenders approving DTI (debt-to-income ratio, meaning your total monthly debts divided by your gross monthly income) as high as 43% to 50% for qualified borrowers. But qualifying at 50% DTI and comfortably affording your mortgage at 50% DTI are two different things. Lender approval tells you the maximum. Your actual budget tells you the sustainable number. Arizonadownpaymentassistance

Use our free DTI calculator to plug in your exact monthly debts and see your real debt-to-income ratio before talking to any lender. It takes two minutes and saves you from building a budget around a number that does not account for your actual financial picture.

What Home Price Range Can You Realistically Target on 60k

With a $1,400 monthly housing budget as the starting point, here is what that translates to in home purchase price at current 2026 rates.

The average 30-year fixed mortgage rate in 2026 is approximately 6.165% and the 15-year rate is approximately 5.477%. Using 6.5% as a working rate for planning purposes, since your actual rate will depend on credit score and lender: JVM Lending

At a $1,400 monthly payment budget with 3.5% down on an FHA loan, you can generally afford a home priced around $185,000 to $200,000 before taxes and insurance eat into your payment budget.

At a $1,250 monthly payment budget, which is more realistic if you carry $400 to $500 in monthly debts, the price range drops to approximately $165,000 to $180,000.

With a $60,000 income, you can typically afford a home priced between $194,000 and $299,000, depending on factors like debt, credit score, and down payment. The upper end of that range assumes minimal existing debt, a credit score above 700, and a meaningful down payment. The lower end is where most buyers at this income level actually land when you account for realistic debt loads and today’s rates. TruPath Home Loans

Here is a side-by-side breakdown at 6.5% on a 30-year loan showing principal and interest only, before taxes and insurance:

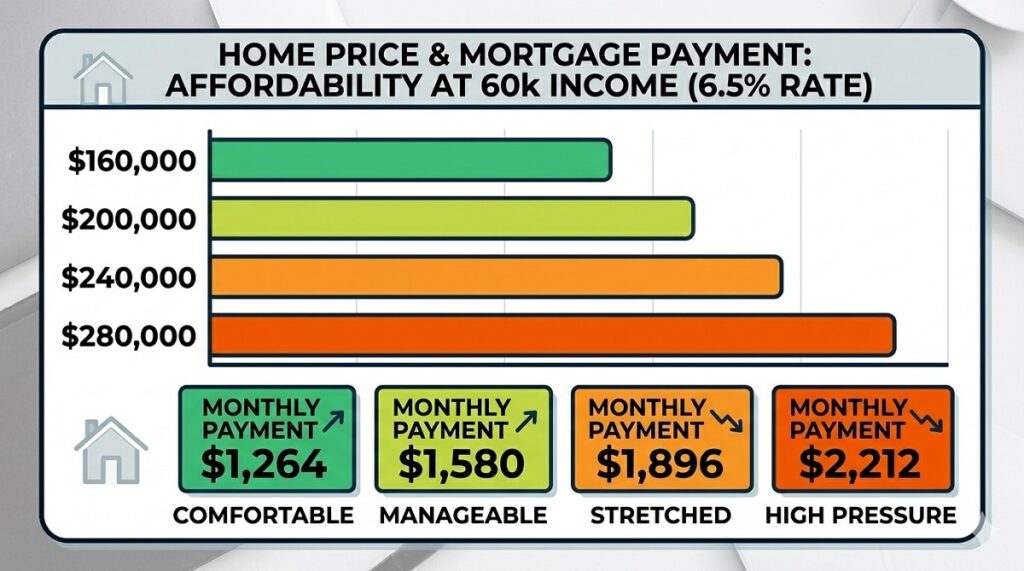

$180,000 loan: approximately $1,138 per month. Combined with $150 insurance and $180 in property taxes, total payment sits around $1,468. That is slightly above the strict $1,400 ceiling but within reach if your other debts are low.

$200,000 loan: approximately $1,264 per month. With taxes and insurance added, total payment reaches $1,600 or more. At this level, you need your other monthly debts to stay under $200 to stay within the 36% total debt ceiling.

$220,000 loan: approximately $1,390 per month in principal and interest. Total housing payment with taxes and insurance pushes $1,740 or above. This is genuinely tight on a $60,000 salary unless your other debts are near zero and your credit score qualifies you for the lowest available rate.

$260,000 loan: approximately $1,643 per month in principal and interest alone. Before taxes or insurance, this already exceeds the 28% ceiling by $243. This price range is only sustainable on a $60,000 salary if you have a large down payment reducing the loan amount, zero other debts, and a credit score that earns you a rate below 6%.

The honest summary: on a $60,000 salary in 2026 at current rates, the comfortable purchase price range without significant down payment assistance is roughly $160,000 to $220,000. Above $220,000 requires either substantial down payment assistance, very low existing debt, or a credit score that earns you a meaningfully below-average rate.

Use our affordability calculator to run your specific numbers including your actual debts, credit score range, and local tax estimates, and get a personalized price range before you start shopping.

How Your Credit Score Changes Everything on a 60k Income

On a $60,000 salary, your credit score has a disproportionately large impact on what you can actually afford compared to higher-income buyers. Here is why.

A higher-income buyer who qualifies for a $450,000 loan sees a 0.5% rate difference between a 680 and a 760 credit score translate to about $135 per month. On a $200,000 loan, that same 0.5% rate difference equals about $60 per month. Sixty dollars per month is the difference between a payment at 28% of your income and a payment at 29.4% of your income on a $60,000 salary. That gap determines whether you qualify for the loan at all.

For a conventional loan, most lenders require a minimum credit score of 620. FHA loans allow scores as low as 580 for a 3.5% down payment. If your score is between 500 and 579, you may still qualify for an FHA loan but will need a 10% down payment. WalletHub

In practical terms for a $60,000 buyer:

Credit score 760 and above: You qualify for the best available conventional rates, can avoid PMI with 20% down, and lenders will compete for your business. A rate around 6.0% to 6.25% is realistic at this tier.

Credit score 700 to 759: Still strong. Conventional loan rates will be slightly higher, FHA is available, and most lenders will approve you without drama. Expect rates in the 6.25% to 6.5% range.

Credit score 640 to 699: Conventional loans are available but the rate premium gets real. FHA becomes your best option at 3.5% down. Rates in the 6.5% to 7.0% range are realistic at this tier.

Credit score 580 to 639: FHA is your primary path at 3.5% down. Conventional lenders may decline or quote rates that make the loan unaffordable. Expect rates of 7.0% or above at this credit tier.

Credit score below 580: FHA with 10% down is the main option. On a $60,000 salary, saving a 10% down payment on even a $180,000 home means $18,000 in savings before closing costs. That is a realistic but long timeline for most buyers at this income level.

The takeaway is simple: if your credit score is below 680, spending three to six months improving it before applying is almost always worth the wait. A 40-point improvement from 640 to 680 on a $190,000 FHA loan at current rates can save you roughly $35 to $60 per month over the life of the loan and open up better program eligibility.

Loan Options That Actually Work for 60k Buyers

Most buyers at $60,000 income have three realistic loan paths depending on credit score, location, and military status.

FHA Loans: The Most Common Path

FHA loans, backed by the Federal Housing Administration, require a minimum 580 credit score for 3.5% down and a minimum 500 credit score with 10% down. In fiscal year 2024, over 82% of FHA purchase loans went to first-time homebuyers. That statistic alone tells you who FHA is designed for. JVM Lending

On a $190,000 home with 3.5% down, your FHA down payment is $6,650. That is significantly more achievable than the $38,000 you would need for 20% down on the same home.

The catch with FHA is mortgage insurance. FHA loans require an upfront mortgage insurance premium (MIP) of 1.75% of the loan amount at closing, plus an annual MIP of 0.55% divided into monthly payments for the life of the loan. On a $183,350 FHA loan after the 3.5% down payment on a $190,000 home, the upfront MIP adds $3,209 to your loan balance or closing costs, and the annual MIP adds roughly $84 per month to your payment permanently until you refinance to a conventional loan once you hit sufficient equity. Yelp

That monthly MIP needs to be factored into your housing budget before you commit. Your $1,400 monthly ceiling gets consumed faster than the principal and interest calculation alone suggests.

VA Loans: Zero Down if You Qualify

If you have served in the US military, a VA loan is far and away the strongest option at a $60,000 income. VA loans are backed by the Department of Veterans Affairs, require zero down payment, and carry no mortgage insurance whatsoever. On a $200,000 home, skipping the down payment and the monthly PMI or MIP saves a $60,000 buyer enormous amounts of money both upfront and monthly. AZ Big Media

The VA does charge a one-time funding fee ranging from 1.4% to 3.6% of the loan amount, which can be rolled into the loan rather than paid at closing. Even with the funding fee, a VA loan almost always outperforms FHA for eligible buyers because the absence of monthly mortgage insurance makes a substantial difference in your monthly cash flow.

USDA Loans: Zero Down for Rural and Suburban Buyers

USDA loans are backed by the US Department of Agriculture for eligible rural and suburban properties, require no down payment, and are available to buyers who meet income limits set by USDA for their county. Many suburban areas that buyers would not consider rural actually qualify for USDA financing. A $60,000 income falls within USDA eligibility limits in many counties across the country. AZ Big Media

Like VA loans, USDA loans carry no PMI in the traditional sense, though they do have a guarantee fee and annual fee that function similarly. Still, the zero-down structure makes USDA an excellent option for $60,000 buyers in qualifying areas who do not have military service.

Our FHA loans guide covers exactly which lenders work best for buyers at this income and credit profile, including which ones are most likely to approve lower credit scores without stacking on excessive fees.

Down Payment Assistance: The Option Most 60k Buyers Never Explore

This is the section most websites skim over, and it is where real money gets left on the table by buyers who do not know to ask.

Every state in the country has at least one down payment assistance program available to buyers at or below certain income thresholds. At $60,000 income, you qualify for many of them. These programs typically offer between $5,000 and $25,000 in assistance structured either as an outright grant that does not need to be repaid, or as a zero-interest deferred loan that gets paid back only when you sell or refinance.

State and local homebuyer assistance programs can help borrowers reach sufficient down payment thresholds and may offer grants, tax credits, or subsidized loans that significantly reduce the amount a buyer needs to bring to closing. Homeplusaz

A $60,000 buyer in Texas, for example, can access the TSAHC Homes for Texas Heroes or Home Sweet Texas programs offering up to 5% in down payment assistance as a fully forgivable grant after three years. On a $185,000 home, that is $9,250 that never needs to be repaid.

A first-time buyer in Georgia earning $60,000 qualifies for the Georgia Dream program offering up to $10,000 in zero-interest deferred down payment assistance. For public servants, teachers, or healthcare workers, that amount increases to $12,500.

Many local city and county programs layer additional assistance on top of state programs. A $60,000 buyer in the right city with the right profession could potentially access $15,000 to $30,000 in combined assistance that transforms what they can afford.

The only way to access these programs is to specifically ask lenders whether they participate. Many lenders will not volunteer this information if you do not ask directly. When you call a lender, say explicitly: what down payment assistance programs are available for a buyer at my income level, and which ones do you participate in?

Use our loan eligibility checker to see which loan types you qualify for, then ask participating lenders specifically about stacking state and local DPA on top of your FHA or conventional loan.

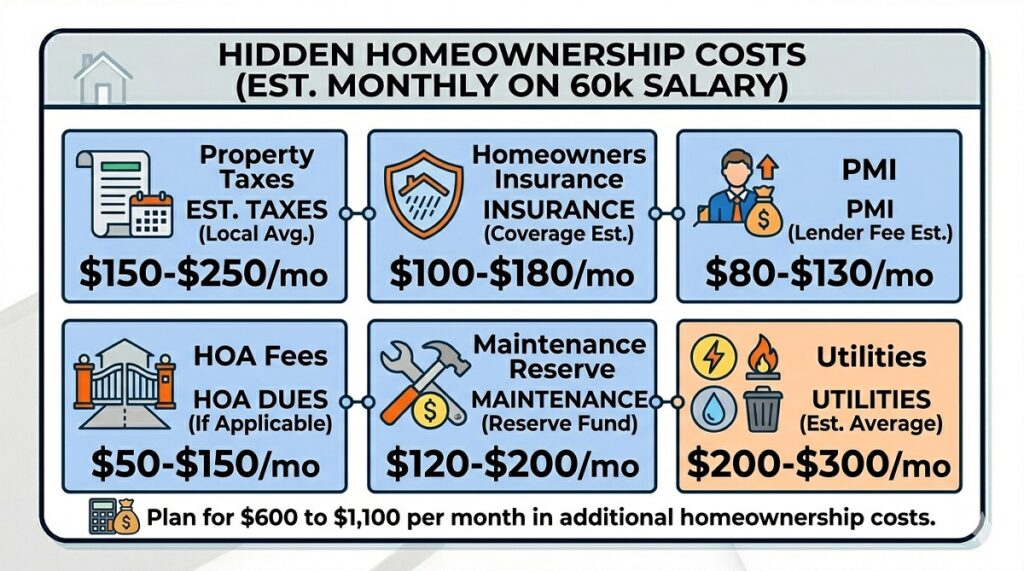

The Hidden Costs That Catch 60k Buyers Off Guard

This is where first-time buyers at every income level get blindsided, but it hits $60,000 buyers particularly hard because there is less financial cushion to absorb surprises.

A Zillow and Thumbtack analysis found that homeowners pay an average of $14,155 per year, or roughly $1,180 per month, in hidden costs related to owning a home beyond the mortgage payment itself, including utilities, property taxes, insurance, and maintenance. That number is not universal. It varies widely by location and home size. But the direction is accurate: your true monthly housing cost is almost always $400 to $900 higher than the mortgage payment alone. Arizonadownpaymentassistance

Here is what those costs look like on a realistic $185,000 home purchase in a mid-cost market:

Property taxes: The national average effective property tax rate is approximately 1.1% of assessed value annually. On a $185,000 home, that equals $2,035 per year, or $170 per month added to your mortgage payment through your escrow account. In high-tax states like New Jersey, Illinois, or Texas, this number can be two to three times higher.

Homeowners insurance: Expect $100 to $200 per month depending on location, home age, and coverage level. Coastal areas, flood zones, and states with high storm risk like Florida, Louisiana, and Oklahoma can push this well above $200 per month.

PMI on an FHA loan: As noted above, roughly $84 per month on a $183,000 loan. On a conventional loan with 5% down and a 680 credit score, PMI typically runs $75 to $150 per month. PMI costs between 0.46% and 1.50% of the original loan amount annually, and must be automatically cancelled by your lender when your loan balance drops to 78% of the original purchase price. Top Consumer Reviews

Maintenance and repairs: Financial advisors recommend budgeting 1% to 3% of your home’s value annually for maintenance and repairs. On a $185,000 home, that is $1,850 to $5,550 per year, or $154 to $463 per month in a dedicated savings reserve. A $60,000 buyer who does not budget for this will face their first major repair, a water heater, a roof section, an HVAC failure, without the funds to cover it. FastExpert

HOA fees: Nearly 44% of homes are now subject to monthly HOA fees, with the median reaching $135 per month in 2025. Condos and townhouses, which are often the most affordable entry points for $60,000 buyers, almost always carry HOA fees. Factor this in before falling in love with a property. Saferate

Utilities: Budgeting $150 to $300 per month for gas, electric, water, and trash is realistic for a modest home in most markets.

Add all of this up and a realistic total monthly housing cost on a $185,000 home for a $60,000 buyer looks like this: mortgage principal and interest around $1,175, property taxes around $170, homeowners insurance around $130, FHA MIP around $84, maintenance reserve around $175, and utilities around $225. Total: approximately $1,959 per month.

That is $39 below 47% of your gross monthly income. It is above the 28% ceiling for housing alone. For a $60,000 buyer this is manageable if it represents the total debt picture, but it leaves very little margin for error. Anyone entering homeownership at this income level needs to know this number going in, not after closing.

Strategies to Increase Your Buying Power on a 60k Salary

You are not stuck at the numbers above. Several legitimate strategies can meaningfully increase what you can afford without increasing your income.

Pay down existing debt first. This is the highest-return move available to most buyers at this income level. Eliminating a $350 per month car payment increases your mortgage budget by $350 per month, which on a 30-year loan at 6.5% translates to approximately $55,000 in additional home purchase power. One car paid off can move you from a $185,000 price range to a $235,000 price range.

Improve your credit score before applying. Moving from a 640 to a 700 credit score reduces your FHA and conventional mortgage rate enough to save $30 to $60 per month on a $185,000 loan. More importantly, it expands which lenders will work with you and which programs you qualify for.

Save a larger down payment. Every additional dollar toward the down payment reduces the loan amount, reduces or eliminates PMI, and lowers the monthly payment. Saving an additional $5,000 beyond the minimum on a $185,000 home reduces your monthly principal and interest by roughly $32 and shrinks the loan balance faster.

Look for homes in lower-tax counties or cities. Property taxes vary enormously not just by state but by county. Two homes 20 miles apart in the same state can carry property tax bills that differ by $3,000 per year. This is a real affordability lever that most buyers overlook.

Explore down payment assistance programs aggressively. As covered above, there are programs specifically designed for buyers at your income level. A $10,000 grant or deferred loan changes the math substantially and may be the difference between staying a renter and becoming a homeowner this year.

Use our mortgage rate comparison tool to benchmark what different lenders are offering for your credit profile and loan type. At a $60,000 income, every 0.25% difference in rate is felt immediately in your monthly payment and your ability to qualify at all.

What Lenders Actually Look at Beyond Your Income

Your $60,000 salary is the starting point, not the ending point, of any lender’s affordability analysis. Here is what else they examine.

Employment history: Lenders want two years of continuous employment in the same field. Job changes are acceptable if they are in the same industry or represent a clear step up. Gaps in employment trigger questions.

Reserves after closing: Most lenders want to see that you will have at least one to two months of mortgage payments remaining in savings after the down payment and closing costs. On a $1,400 monthly payment, that means $1,400 to $2,800 in reserves at minimum. FHA technically allows closing with minimal reserves, but conventional lenders are stricter.

Payment history: A single 30-day late payment in the last 12 months on any account can affect both your credit score and your lender’s willingness to approve you. Lenders look for no late payments 30 days or greater in the last 12 months and no derogatory marks on the credit report for the strongest approval. AZ Big Media

Consistent income sources: If part of your $60,000 comes from overtime, bonuses, or side income, lenders average the last two years of that income rather than using the current annualized figure. If your overtime was high two years ago and lower now, your qualifying income may be less than $60,000.

Large recent deposits: Any large bank deposit that is not a paycheck or an obvious transfer will trigger a paper trail request from underwriting. Lenders want to know the source of funds used for down payment and closing costs. Gift money from family is acceptable on most loan types but requires a gift letter and documentation.

The Realistic Picture: What a 60k Buyer Can Actually Buy in 2026

The honest summary for a $60,000 buyer in 2026 is this.

In lower-cost markets, states like Ohio, Indiana, Michigan, Missouri, Alabama, Mississippi, Arkansas, and parts of Texas and the Southeast, a $60,000 salary can comfortably buy a genuine home in good condition in a decent neighborhood. The math works without heroic effort.

In mid-cost markets, states like Georgia, North Carolina, Tennessee, Arizona, and most of the Midwest, you can buy a starter home with the right loan program and down payment assistance. It requires more discipline and more patience to find the right property at the right price, but it is realistic.

In high-cost markets, California, New York, Massachusetts, Colorado, Washington state, and similar, a $60,000 salary alone does not produce a viable buyer without extraordinary down payment assistance, a second income on the loan, or a willingness to buy far from urban centers. This is not pessimism, it is arithmetic.

The right move before anything else is to get a real preapproval from a lender who will tell you honestly what you qualify for, then use our affordability calculator alongside our mortgage calculator to build a full monthly budget that includes taxes, insurance, PMI, and maintenance. That combination tells you whether the home you are considering is genuinely affordable for your life, not just for your loan application.

DISCLAIMER BLOCK

This article is for informational purposes only and does not constitute financial or legal advice. Mortgage rates, loan limits, income requirements, and program eligibility change frequently. All payment figures are estimates based on assumed interest rates and standard loan terms. Your actual rate, qualification, and payment will vary based on your credit profile, lender, location, and current market conditions. Always consult a licensed mortgage professional before making any home buying decisions.

")