Mortgage Pre-Approval vs Pre-Qualification: Understanding the Key Differences in 2026

For anyone planning to buy a home, the early stages of the mortgage process can feel confusing. There are many terms that sound similar but carry very different meanings, and misunderstanding them can lead to costly mistakes. Two of the most commonly misunderstood concepts are pre-approval and pre-qualification. While both are important steps, they serve different purposes and offer different levels of certainty.

In today’s competitive housing market, being well-prepared can make a significant difference. Sellers are more selective, and buyers need to demonstrate financial readiness to stand out. Understanding how these two processes work can help you move forward with confidence and avoid unnecessary delays.

This article provides a detailed comparison to help you understand how each process works, what it involves, and when you should use it. By the end, you will have a clear picture of how to approach your home buying journey strategically.

What Is Pre-Qualification and How Does It Work

Pre-qualification is usually the first step for many homebuyers who want to explore their borrowing potential. It is a simple and quick process where a lender provides an estimate of how much you might be able to borrow based on basic financial information.

This process typically involves sharing details about your income, debts, and assets. In most cases, the information is self-reported and not thoroughly verified. Because of this, pre-qualification does not carry strong weight in the eyes of sellers or real estate agents. Instead, it serves as a starting point for understanding your budget.

One of the main advantages of pre-qualification is its convenience. It can often be completed online within a short period of time, making it an accessible option for those who are just beginning to consider homeownership. It helps you get a rough idea of your price range, which can guide your initial property search.

However, it is important to remember that pre-qualification is not a guarantee of a loan. Since the information is not verified, the final approval amount may differ significantly once a full review is conducted. This is why it should be viewed as an informational tool rather than a commitment from the lender.

What Is Pre-Approval and Why It Matters

Pre-approval is a more detailed and formal process that provides a stronger indication of your borrowing power. Unlike pre-qualification, it involves a thorough review of your financial situation, including verification of your income, credit history, and employment status.

During this process, lenders typically request documents such as pay stubs, tax returns, bank statements, and credit reports. They analyse this information carefully to determine how much they are willing to lend and under what terms. As a result, pre-approval offers a more accurate and reliable estimate.

In the context of mortgage pre-approval vs pre-qualification, pre-approval stands out as the more credible option. It signals to sellers that you are a serious buyer who has already been vetted by a lender. This can give you a competitive edge, especially in markets where multiple offers are common.

Pre-approval also helps you move faster once you find the right property. Since much of the financial review has already been completed, the final loan approval process becomes smoother and quicker. This can be a significant advantage when timing is critical.

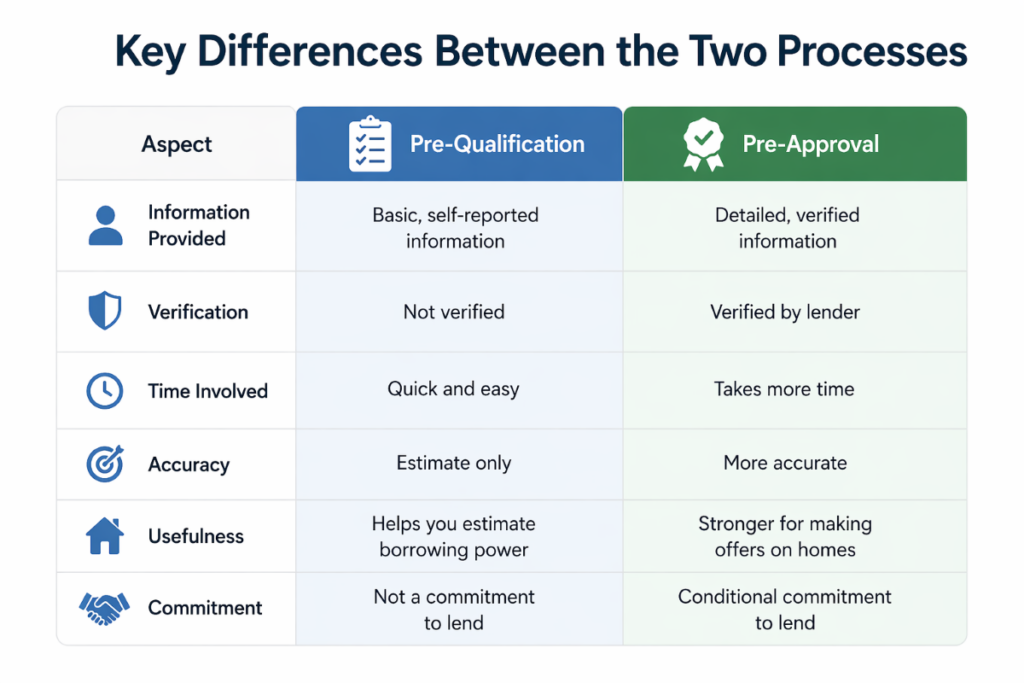

Key Differences Between the Two Processes

Although pre-qualification and pre-approval may seem similar at first glance, they differ in several important ways. Understanding these differences can help you decide which option is right for your situation.

Pre-qualification is based on unverified information, while pre-approval involves a detailed review of your financial documents. This makes pre-approval far more reliable and accurate. In addition, pre-qualification is usually quick and informal, whereas pre-approval requires more time and documentation.

Another key difference lies in how each is perceived by sellers. Pre-qualification does not carry much weight in negotiations because it does not guarantee that a lender will approve the loan. On the other hand, pre-approval demonstrates financial readiness and increases your credibility as a buyer.

In terms of commitment, pre-qualification is simply an estimate, while pre-approval is a conditional commitment from the lender. This distinction is crucial when you are competing for a property in a fast-moving market.

When Should You Choose Pre-qualification?

Pre-qualification is best suited for the early stages of your home buying journey. If you are still exploring your options and want to understand your budget, this process provides a quick and easy way to get started.

It is particularly useful if you are unsure about your financial readiness or if you are planning to buy a home in the future rather than immediately. By getting a general idea of how much you can afford, you can begin to set realistic expectations and plan accordingly.

Pre-qualification can also help you identify areas where you may need improvement. For example, if the estimated loan amount is lower than expected, you can take steps to increase your income, reduce debt, or improve your credit score before moving forward.

However, relying solely on pre-qualification when making an offer on a property is not recommended. Since it does not carry much weight with sellers, it may put you at a disadvantage compared to buyers who have already secured pre-approval.

When Should You Choose Pre-approval?

Pre-approval is the right choice when you are serious about buying a home and are ready to take the next step. It provides a clear understanding of your borrowing capacity and demonstrates to sellers that you are financially prepared.

In the discussion of mortgage pre-approval vs pre-qualification, pre-approval is often the preferred option for active buyers. It gives you confidence in your budget and allows you to focus on properties that match your financial situation.

Another advantage of pre-approval is that it reduces uncertainty during the buying process. Since your financial information has already been verified, there are fewer surprises when it comes time for final approval. This can make the entire process less stressful and more predictable.

Pre-approval is especially important in competitive markets where multiple buyers may be interested in the same property. Having a pre-approval letter can strengthen your offer and increase your chances of success.

Common Mistakes to Avoid

Many homebuyers make mistakes during the early stages of the mortgage process that can affect their chances of approval. Being aware of these pitfalls can help you navigate the process more effectively.

One common mistake is confusing pre-qualification with pre-approval and assuming that both carry the same level of credibility. This misunderstanding can lead to disappointment when an offer is not taken seriously by sellers.

Another mistake is making significant financial changes after getting pre-approved. Taking on new debt, changing jobs, or making large purchases can affect your financial profile and potentially impact your loan approval.

It is also important to provide accurate and complete information during the application process. Any discrepancies or missing details can delay the process or lead to complications later on.

By avoiding these mistakes, you can ensure a smoother and more successful home buying experience.

Conclusion

Understanding the difference between pre-qualification and pre-approval is essential for anyone entering the housing market. While both serve important roles, they are not interchangeable and should be used at different stages of the buying process.

Pre-qualification offers a quick and simple way to estimate your borrowing potential, making it ideal for early planning. Pre-approval, on the other hand, provides a more accurate and reliable assessment, giving you a strong position when making an offer on a property.

By using these tools strategically, you can approach the home buying process with confidence and clarity. Being well-prepared not only improves your chances of securing a mortgage but also helps you make informed decisions that align with your long-term financial goals.