Mortgage Points Explained 2026 What They Are and When to Buy

Mortgage points are one of those topics that most buyers nod along to when the lender mentions them and then quietly Google afterward. The lender says something like “you can buy down your rate by paying points,” hands you a loan estimate with three different rate options at three different point levels, and suddenly you are trying to do math in your head while also thinking about whether you remembered to submit your pay stubs.

Here is mortgage points explained in plain language, with real numbers and honest trade-offs, so you can make this decision confidently before you sit across from a lender.

The short version: a mortgage point is a fee you pay upfront at closing to permanently lower your interest rate. One point costs 1% of your loan amount. One point typically reduces your interest rate by about 0.25%, though this varies by lender and market conditions. Whether paying that fee makes financial sense depends entirely on how long you plan to keep the loan, and right now in 2026 that calculation requires some extra thought. Rocket Mortgage

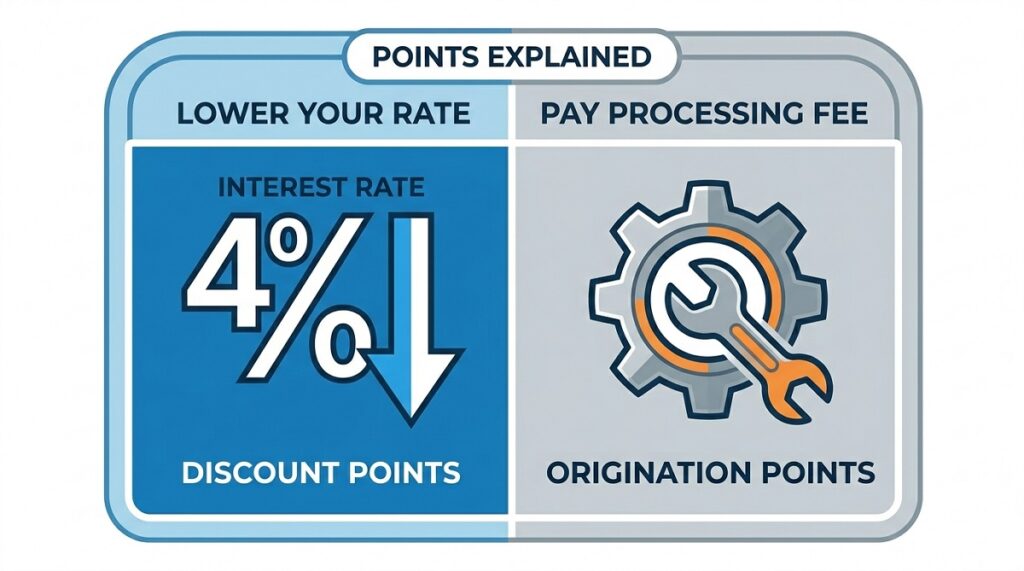

Discount Points vs Origination Points: Two Very Different Things

Before anything else, this distinction needs to be clear because lenders are not always careful about separating these two terms, and the IRS treats them completely differently.

Discount points are what most people mean when they say mortgage points. You pay them at closing specifically to lower your interest rate. They are prepaid interest. One discount point on a $350,000 loan costs $3,500 and buys you a lower rate, typically 0.25% lower, for the entire life of the loan.

Origination points are something else entirely. Origination points are charged by lenders to cover loan processing costs, and sometimes include fees for appraisals, inspections, title, attorneys, notaries, and real estate taxes. Origination points do not reduce your interest rate. They are simply a fee for originating the loan, dressed up in similar-sounding language. Reverse Mortgage

The reason this distinction matters so much: discount points are typically considered prepaid interest by the IRS and are usually tax-deductible for those who itemize deductions. Origination points are service fees and are not tax-deductible. WalletHub

When you get a loan estimate from any lender, look at Section A of the document. That is where lenders are required to separate origination charges from discount points. If the loan estimate lumps them together without breaking them out, ask your loan officer to separate them before you agree to anything.

How Mortgage Points Actually Work: Real Dollar Examples

Let me put actual numbers to this so it stops being abstract.

Say you are buying a home in Texas and taking out a $400,000 mortgage. Your lender quotes you a 30-year fixed rate of 6.75% with no points, or 6.50% if you buy one discount point.

One point on a $400,000 loan costs $4,000.

At 6.75%, your monthly principal and interest payment on $400,000 is roughly $2,594.

At 6.50%, that same loan payment drops to roughly $2,528.

The difference is $66 per month.

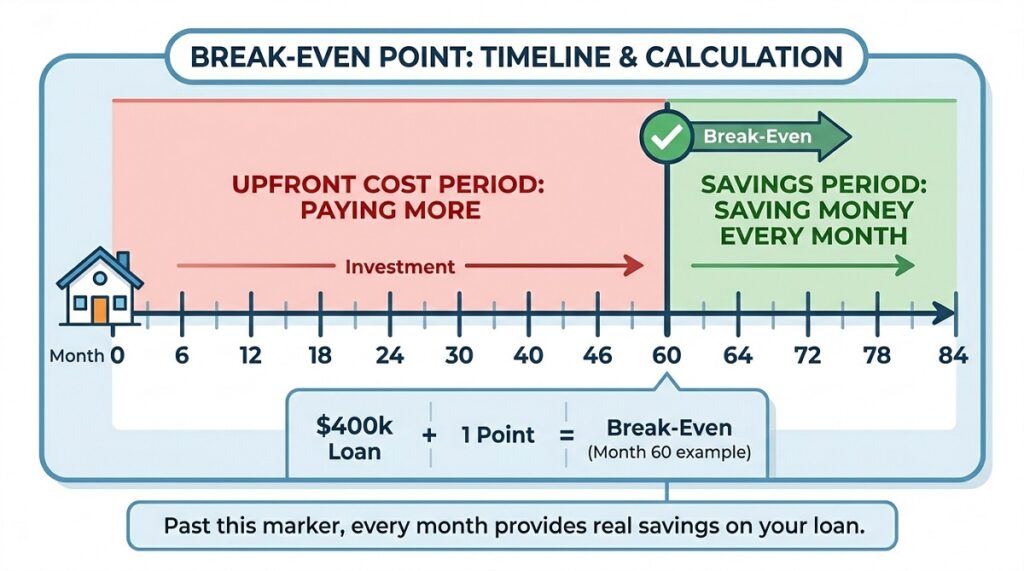

To calculate your break-even point, you divide the cost of the point by the monthly savings:

$4,000 divided by $66 equals approximately 60.6 months.

That means you need to keep this exact loan for just over five years before the monthly savings pay back what you spent upfront. Month 61 onward, you are ahead. The break-even period typically falls between four and eight years depending on the rate reduction and loan size. Rocket Mortgage

Now try the same math with two points. Two points costs $8,000 and reduces your rate by roughly 0.50%, from 6.75% to 6.25%. Your payment drops to about $2,463, saving $131 per month.

$8,000 divided by $131 equals approximately 61 months, nearly the same break-even as one point.

This is an important pattern: buying two points does not usually produce a dramatically faster break-even than one point because the cost doubles along with the savings. In most cases, one point produces the better math than two unless your lender offers an unusually aggressive rate discount on the second point. Always ask your lender to show you the numbers for zero points, one point, and two points separately and compare the break-even timelines yourself.

Use our free mortgage calculator to run payment comparisons across different rate scenarios before deciding whether any particular point purchase is worth the upfront cost.

How to Calculate the Break-Even Point on Mortgage Points

The break-even formula is simple and worth knowing by heart.

Cost of points divided by monthly payment savings equals months to break even.

To calculate the point at which you recover your outlay on the prepaid interest, divide the cost of the mortgage points by the amount the reduced rate saves you each month. Propertyprosatlanta

The harder part is being honest about your timeline. Most buyers overestimate how long they will stay in a home. The average American sells or refinances within seven to ten years of purchase, but many buyers in hot markets move sooner than they planned. Many homeowners refinance or move before reaching break-even, so paying points may not always yield savings. FHA.com

A concrete example on a $350,000 loan:

One point costs $3,500. It lowers your rate from 6.75% to 6.50%. Monthly payment drops from $2,270 to $2,213 on a 30-year term. Monthly savings: $57. Break-even: $3,500 divided by $57 equals 61 months, just over five years.

If you sell this home in year four to upsize for a growing family, you spent $3,500 and only recovered $2,736 in savings. You lost $764 on the transaction.

If you stay for ten years, you saved $6,840 total against a $3,500 cost. Net gain: $3,340.

The math is not complicated. The discipline is being honest about whether you are actually a ten-year buyer or a five-year buyer before you write the check.

Lender Credits: The Opposite of Buying Points

If discount points let you pay more upfront to lower your rate, lender credits work in exactly the opposite direction. Understanding both gives you real negotiating power.

Lender credits allow homebuyers to reduce their upfront closing costs in exchange for accepting a slightly higher interest rate. This reverses the points equation: you save money upfront but pay slightly more every month. WalletHub

Lender credits are sometimes called negative points, and they make sense in specific situations. If you are cash-strapped after the down payment, do not have much in reserves, or plan to sell or refinance within three to five years, taking a lender credit reduces your out-of-pocket costs at closing while accepting a modestly higher monthly payment during the period you own the home.

If you plan to sell or refinance within three to five years, negative points can be a better deal than buying discount points. The Mortgage Reports

The practical scenario: a buyer in Georgia purchasing a $320,000 home puts 5% down and has $8,000 left for closing costs. Their lender quotes them 6.75% at par, or 7.00% with a $3,200 lender credit. Taking the higher rate puts $3,200 back in their pocket at closing. If they sell in four years, they paid $38 more per month for 48 months, totaling $1,824 in extra interest. But they kept $3,200 at closing. Net benefit: $1,376 in their favor.

That is the honest math of lender credits, and it is why they make sense for buyers who are not planning a long stay.

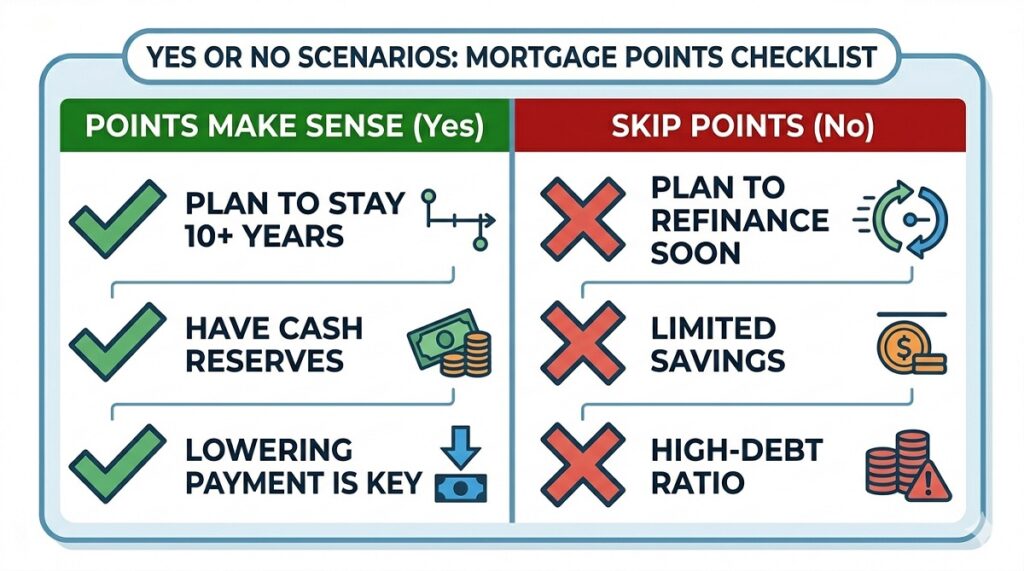

When Buying Mortgage Points Makes Sense and When It Does Not

Points make sense when three conditions align: you plan to stay in the home long past the break-even point, you have the cash to buy points without compromising your emergency fund or down payment, and the rate reduction per point is at least 0.20%. The Mortgage Reports

Points make the most sense for buyers who are purchasing what they genuinely consider a forever home or a long-term home, have already hit 20% down so PMI is not a concern, have six months or more of living expenses saved beyond the down payment and closing costs, and are confident they will not need to refinance in the near term.

Points make much less sense in 2026 specifically. In 2026, buying two or more points is rarely recommended given the high likelihood of refinancing as rates fall, and a seller-paid buydown should almost always be accepted if offered since it is essentially free money that reduces your first two years of payments significantly. Arizona Department of Housing

Think about it this way: if you lock in at 6.75% and pay $8,000 in points to get to 6.25%, and then rates drop to 5.75% in 2027 making a refinance attractive, you just paid $8,000 to own a rate you are going to refinance away. Every dollar you spent on points gets wiped out the moment you refinance.

If buying points reduces your down payment, that alone is reason enough to reconsider. A lower down payment raises your interest rate and may increase PMI costs, creating a situation where the points purchase actually makes your overall loan more expensive, not less. Homeplusaz

Who should almost certainly skip buying points right now: buyers who are not 100% certain of a long stay, buyers who have under 20% to put down, buyers who are depleting their savings to cover the down payment and closing costs, and buyers on FHA or VA loans who already benefit from lower rates and may refinance to conventional later.

Mortgage Points and Taxes: What the IRS Actually Says

This section trips up a lot of buyers, and the rules are genuinely confusing.

Discount points paid on a home purchase mortgage for your primary residence may be fully deductible in the year you pay them, according to IRS rules outlined in IRS Publication 936. Origination points, however, have different rules and are generally not deductible. Yelp

To deduct discount points in full in the year of purchase on a primary home, the IRS requires that the loan be secured by your main home, the points are calculated as a percentage of the loan principal, paying points is a standard practice in your area, the points are clearly listed on your Closing Disclosure as prepaid interest, and you did not borrow the funds for the points from the lender.

For 2026, the standard deduction is $32,200 for married couples filing jointly and $16,100 for single filers. The loan amount for deductibility purposes must be $750,000 or less if the mortgage originated after December 15, 2017. U.S. News & World Report

That standard deduction number matters because it determines whether itemizing even makes sense for you. You only benefit from the points deduction if your total itemized deductions exceed the standard deduction. If not, the tax advantage from buying points effectively disappears. AZ Big Media

For refinances, the rules are different. If you paid $5,000 in points on a 30-year refinance, you generally cannot deduct the full amount in year one. Instead, you must spread the deduction over 360 months, which works out to roughly $167 per year. That is a meaningful difference from the purchase scenario. AZ Big Media

For investment properties and second homes, points must always be amortized over the life of the loan. You cannot deduct them all in year one regardless of how the points are structured.

Always confirm your specific situation with a tax professional before assuming any deduction applies to you. The IRS rules have enough conditions attached that what works for one buyer does not automatically work for another.

Temporary Rate Buydowns: The 2-1 Buydown Explained

Temporary buydowns are showing up more often in 2026 as builders and sellers use them as incentives to close deals in a high-rate environment. They are not the same as discount points and are worth understanding separately.

A temporary buydown lowers your interest rate for a set period, usually paid for by the lender, seller, or builder rather than the buyer. The most common structure is a 2-1 buydown, where the rate is 2% lower in year one, 1% lower in year two, and then returns to the full contracted rate from year three onward for the rest of the loan. Propertyprosatlanta

On a $350,000 loan at a contracted rate of 6.75%, a 2-1 buydown means you pay at 4.75% in year one and 5.75% in year two. The seller or builder deposits the difference into an escrow account at closing to make up what you do not pay during those first two years.

A seller-paid 2-1 buydown should almost always be accepted if it is offered during negotiations because it reduces your actual out-of-pocket costs in the fmortgage points explained, discount points mortgage, buy down mortgage rate, mortgage points 2026, mortgage points break even, should I buy mortgage points, mortgage points tax deductible, origination points vs discount points, lender credits mortgage, negative mortgage pointsirst two years at zero cost to you. Arizona Department of Housing

The caution: a temporary buydown is not the same as a permanent rate reduction. Your rate comes back to full in year three. If you are budgeting based on the year-one payment without accounting for the year-three jump, you can find yourself in payment shock when the escrow subsidy runs out.

Use our DTI calculator to confirm your debt-to-income ratio at the full contracted rate, not the buydown rate, before agreeing to any temporary buydown structure. Qualifying comfortably at year-three payment levels is what matters for long-term stability.

Mortgage Points on FHA VA and USDA Loans

Points work the same mechanical way on government-backed loans, but there are a few things worth knowing specifically.

Discount points are available on FHA, VA, and USDA loans. The mechanics stay the same: pay 1% of the loan amount per point to lower the rate. Research found that FHA borrowers with credit scores below 640 were especially likely to buy points, with nearly 77% purchasing them, suggesting lenders may use points to help these borrowers qualify by lowering monthly payments and improving their debt-to-income ratio. Homeplusaz

If your DTI is sitting right at the edge of qualification on an FHA loan, buying one point to lower the payment by $50 to $80 per month can be the difference between approval and denial. In that specific scenario, points serve a qualification purpose beyond just saving money over time.

For VA buyers, the zero-down-payment structure means many VA borrowers close with limited cash reserves. Spending $3,000 to $6,000 on discount points when cash is already tight can leave you without an emergency fund in your first year of homeownership. The monthly savings from the lower rate rarely justify that risk.

Our FHA loans guide covers how lenders use points within FHA loan structures and which lenders handle this most transparently.

How to Compare Lender Quotes That Include Points

This is where buyers get confused most often and where real money gets left on the table.

When you receive quotes from multiple lenders, the rates they advertise are almost never apples-to-apples comparisons. One lender may quote 6.375% with one point included. Another may quote 6.625% with zero points. On the surface, the first lender looks cheaper. In reality, you are comparing a rate that cost $3,500 extra upfront against one that cost nothing.

To compare fairly, always ask every lender to give you the rate with zero points, one point, and two points. This gives you a consistent baseline across lenders. Then use our free mortgage rate comparison tool to see where current market rates actually sit before any lender’s quote can mislead you.

Consider also that the cash required for points could often be better spent paying off high-interest credit card or student loan debt, building an emergency fund, or investing in assets that yield a higher rate of return. A 0.25% rate reduction on a $350,000 mortgage saves you about $57 per month. If you have a credit card charging 24% interest on a $3,500 balance, paying off that card saves you roughly $840 per year in interest. The points purchase does not come close to that return. Arizonadownpaymentassistance

The honest framework for deciding: calculate your break-even, be realistic about your timeline, confirm you have reserves left after buying points, and ask yourself whether the same dollars put toward the down payment instead would eliminate PMI and produce a better outcome overall.

A Quick-Reference Summary on Mortgage Points

One discount point costs 1% of your loan amount. One point on a $350,000 loan costs $3,500.

One point typically lowers your rate by 0.25%, though this varies by lender and market.

Break-even formula: cost of points divided by monthly savings equals months to break even. Typical break-even falls between 48 and 84 months depending on loan size and rate reduction.

Discount points are typically tax-deductible in the year of purchase on a primary residence if you itemize and meet IRS requirements. Origination points are not tax-deductible.

Lender credits are the opposite of discount points. Accept a higher rate, pay less at closing. Best for buyers with short timelines or limited cash.

Temporary buydowns like the 2-1 structure are paid by sellers or builders and reduce your rate temporarily. Not the same as permanent discount points.

Before buying or skipping points, run the break-even math yourself using our affordability calculator and confirm the scenario makes sense given your actual expected timeline in the home.

DISCLAIMER BLOCK

This article is for informational purposes only and does not constitute financial or legal advice. Mortgage rates, points pricing, tax rules, and program requirements change frequently. Tax deductibility of mortgage points depends on your individual circumstances. Always consult a licensed mortgage professional and a qualified tax advisor before making decisions about buying discount points or structuring your loan.