")

Mortgage Debt-to-Income Ratio (Complete Guide 2026)

Introduction

When applying for a mortgage, lenders do not only look at your income or credit score. One of the most important factors they evaluate is your debt-to-income ratio, commonly known as DTI. This number helps lenders understand how much of your monthly income is already committed to paying debts and whether you can afford a new home loan.

The debt-to-income ratio plays a crucial role in mortgage approval. Even if you have a stable job and good income, a high DTI can reduce your chances of getting approved. On the other hand, a lower DTI shows that you manage your finances responsibly and can handle additional payments. In this guide, you will learn what DTI means, how it is calculated, what lenders expect in 2026, and how you can improve it to qualify for a mortgage.

What Is a Debt-to-Income Ratio?

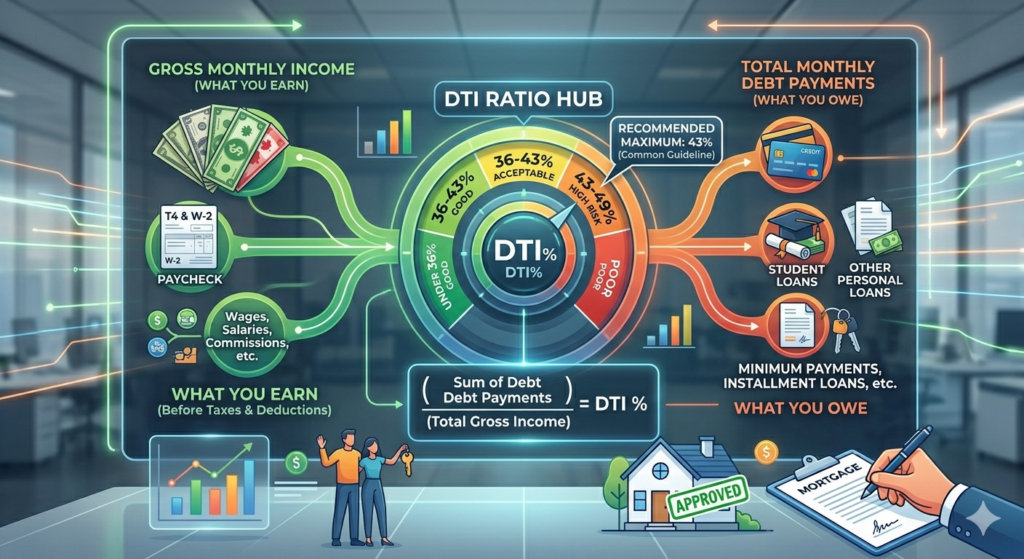

The debt-to-income ratio is a financial measure that compares your total monthly debt payments to your gross monthly income. It is expressed as a percentage and helps lenders determine your ability to repay a loan. For example, if you earn a certain amount each month and a portion of that goes toward paying debts like loans, credit cards, or other obligations, your DTI reflects how much of your income is already used. A lower percentage indicates better financial health, while a higher percentage suggests a higher financial burden.

How Mortgage DTI Works

In mortgage lending, DTI is used to assess risk. Lenders want to ensure that borrowers can comfortably make monthly mortgage payments along with their existing debts. There are two main types of DTI that lenders consider. The first is the front-end ratio, which focuses only on housing-related costs such as mortgage payments, property taxes, and insurance. The second is the back-end ratio, which includes all monthly debts such as credit cards, car loans, student loans, and the new mortgage payment. Most lenders place more importance on the back-end ratio because it gives a complete picture of your financial obligations.

How to Calculate Debt-to-Income Ratio

Calculating your DTI is simple and helps you understand your financial position before applying for a mortgage. DTI = \frac{\text {Total Monthly Debt Payments}} {\text{Gross Monthly Income}} \times 100 To calculate it, you add all your monthly debt payments and divide that number by your total monthly income before taxes. Then multiply by 100 to get the percentage. For example, if your total monthly debt payments are 1,000 and your income is 4,000, your DTI would be 25%.

What Is a Good DTI for a Mortgage?

A good DTI ratio depends on the type of loan and lender requirements, but generally, lower is always better. Most lenders prefer a DTI below 36 per cent. This indicates that you are not overburdened with debt and can manage additional payments. Some loan programmes allow higher ratios, sometimes up to 43 per cent or even 50 per cent in certain cases. However, higher DTI ratios may come with stricter conditions or higher interest rates. Keeping your DTI low increases your chances of approval and helps you secure better loan terms.

Why DTI Matters in Mortgage Approval

DTI is one of the key indicators lenders use to evaluate risk. It shows how much of your income is already committed and how much is available for new obligations. A high DTI suggests that you may struggle to keep up with payments, especially in case of unexpected expenses or income changes. A low DTI, on the other hand, indicates financial stability and responsible money management. This is why lenders use DTI along with credit score, employment history, and savings to make lending decisions.

Front-End vs Back-End DTI

Understanding the difference between these two ratios is important for mortgage approval. The front-end ratio focuses only on housing costs. This includes your expected mortgage payment, property taxes, and insurance. The back-end ratio includes all your debts, such as credit cards, personal loans, car payments, and student loans, along with your mortgage. Lenders usually prioritise the back-end ratio because it gives a more complete view of your financial situation.

How to Improve Your Debt-to-Income Ratio

Improving your DTI can significantly increase your chances of mortgage approval. One of the most effective ways is to pay down existing debts. Reducing credit card balances or closing small loans can lower your monthly obligations. Another approach is to increase your income. This can be done through side work, freelance opportunities, or salary growth. Avoid taking on new debt before applying for a mortgage, as this can increase your DTI and reduce your eligibility. Careful budgeting and financial planning also help maintain a healthy ratio.

Common Mistakes to Avoid

Many borrowers make mistakes that negatively impact their DTI. One common mistake is applying for new credit shortly before a mortgage application. This increases your debt and may lower your approval chances. Another mistake is underestimating monthly expenses. It is important to include all debts when calculating DTI. Ignoring small debts can also affect your ratio, as lenders consider all obligations. Being aware of these mistakes helps you prepare better for mortgage approval.

DT vs Credit Score

DT While both DTI and credit score are important, they measure different aspects of your financial health. DTI focuses on your ability to repay based on income and existing debt. A credit score reflects your history of managing credit and making payments on time. A strong mortgage application usually requires both a good credit score and a manageable DTI.

DTI Limits for Different Loan Types

Different mortgage programmes have different DTI requirements. Conventional loans typically prefer lower DTI ratios, often below 36 to 43 per cent. Government-backed loans may allow higher ratios depending on borrower qualifications. However, even if higher DTI is allowed, maintaining a lower ratio is always beneficial for better loan terms.

Conclusion

The debt-to-income ratio is one of the most important factors in mortgage approval. It gives lenders a clear picture of your financial health and ability to manage new debt. By understanding how DTI works and taking steps to improve it, you can increase your chances of getting approved for a mortgage and securing better terms. Planning ahead, reducing debt, and maintaining a stable income are key strategies for achieving a healthy DTI in 2026.

FAQs

What is a good debt-to-income ratio for a mortgage?

A DTI below 36 per cent is generally considered good.

How is DTI calculated?

It is calculated by dividing total monthly debt by gross monthly income.

Can I get a mortgage with a high DTI?

Yes, but it may be more difficult and come with higher interest rates.

Does DTI include all debts?

Yes, it includes credit cards, loans, and other monthly obligations.

How can I lower my DTI?

By paying off debts and increasing income.

: Top Picks & Reviews")