How to Get a Mortgage With Bad Credit

A Complete, Easy-to-Understand Guide for Home Buyers

One of the most popular challenging issues that people are struggling with today is getting a mortgage with bad credit. You are not alone, whether your credit score has been lowered due to missed payments, medical expenses, job loss, or just not understanding how credit works.

This is a situation that millions of people find themselves in every year. The silver lining is that bad credit is not a total block to owning a home. Even with the correct information, adequate planning and an intelligent approach, it is possible to still be approved for a mortgage and purchase the house you desire.

In plain and easy English, this guide will take you through all you need to know by explaining the meaning of your credit score, how to find the appropriate lender, and many more.

What Is Bad Credit?

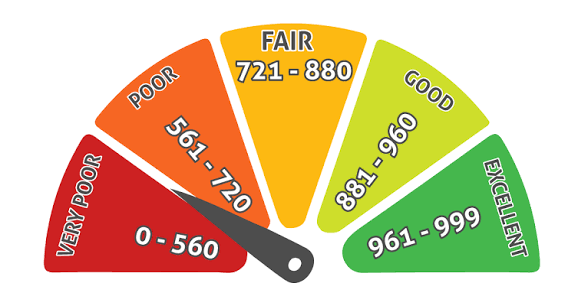

Your credit score is a three-digit figure that is in a range between 300 and 850.

This is determined by your history of financial activity, like the frequency at which you pay your bills, the amount of debt that you owe, the length of time you have held credit accounts and any bankruptcies or defaults.

Lenders determine this number so that they can decide whether it would be risky lending you money.

Here is a simple breakdown of what different credit score ranges mean:

| Score Range | Rating | Mortgage Chances | Typical Rate |

| 750 – 850 | Excellent | Very Easy | Lowest available |

| 700 – 749 | Good | Easy | Low |

| 650 – 699 | Fair | Possible | Average |

| 580 – 649 | Poor | Difficult | High |

| Below 580 | Bad / Very Poor | Very Hard | Very High |

There are very few traditional banks and mortgage lenders who will take your application into consideration unless you have an acceptable credit score of 620 or higher.

A score lower than this will put you in the bad credit mortgage category. But, as you are going to discover in this guide, there are still several ways to go.

The Reason bad credit makes Mortgages difficult and Step by step Guide

In order to see why credit scores are so important, you must put yourself in the eyes of the lender.

A bank is lending you a lot of money when it gives you a mortgage, hundreds of thousands of dollars, and it is lent to you over a very long period of time, typically 15 to 30 years.

The bank should be satisfied that you are going to repay that money month after month over decades.

The biggest indicator that the bank will use to determine that trust is your credit score. When you carry a low score, the lender is anxious that you have had debt problems previously.

Due to this worry, lenders could react by doing any of the following:

- This is by charging you a much higher interest rate to reflect the increased risk.

- Demanding more down payment, as much as 20 percent or higher.

- Requesting a lot more documentation and evidence of stable income.

- Incorporating more terms and conditions on your loan.

- Turning down your application in an outright manner, particularly at old fashioned big banks.

This will help you realize that your objective is not merely to secure a mortgage, but to minimize the perceived risk to the lender so that they are willing to say yes.

Step 1: A How-To Guide to Mortgage with Bad Credit

Check and Understand your credit Report

The first and most important thing you ought to do when requesting any mortgage is to draw up your complete credit report. Do not simply keep an eye on your score number. Look through the report. AnnualCreditReport.com allows you to receive a gratis credit report annually by each of the three larger bureaus, including Equifax, Experian, and TransUnion, in the United States.

In looking at your report, you should find the following typical problems:

- Late or missed payments that could have been reported with errors.

- Bank accounts that are not yours, and may be a sign of identity theft.

- The debts already paid but still indicated as yet to be paid.

- Wrongly-balanced accounts or credit limits.

Should you notice any mistakes, challenge them on the spot with the credit bureau. It is free and can even improve your score by 20 to 50 points in a 30 to 60 day period, merely by removing misinformation.

Step 2: Work on Improving Your Score Before Applying

A minor credit score increase will open the door to much more advantageous mortgage conditions.

Unless you are in a desperate misery to purchase a house, you can save thousands of dollars in interest over the life of the mortgage by taking the time to improve your credit first (6-12 months).

These are the best things that you can do to improve your score within a short period of time:

- Always pay all bills on time in future. The largest component of your score is payment history, which takes 35% of the calculation.

- Clear out your credit card debts. You should strive to maintain a balance of less than 30 per cent of your credit limit on each card. This is known as your credit utilization ratio.

- You should not close old credit card accounts even when you are not using them. Age of old accounts enhances the average age of your credit report.

- Do not take out new credit cards, automobile loans, or any other borrowing prior to your mortgage application. Every application poses a difficult question that has the potential to reduce your score.

- In the event you have a collection account, attempt to negotiate a pay-to-drop agreement with the collector to delete the account off your report and pay them to do so.

Step 3: Save a Bigger Down payment

A large down payment is one of the most potent factors that bad credit borrowers have. The larger a down payment you make the less the lender has to risk and the more they are willing to ignore a low credit score.

Although the maximum down payment ranges between 5 and 10 percent of the purchase price of a home, aim at saving a minimum of 20 percent when your credit is weak.

- A down payment of 20 percent does a number of things for you.

- First, it saves on the need to have private mortgage insurance (PMI) which is the additional monthly fee.

- Second, it demonstrates to the lender that you are a serious saver.

- Third, it massively minimizes the risk assumed by the lender usually leading to the approval despite a poor credit profile.

Step 4: Discover Government-sponsored Loan Programs

Among the best-kept secrets of bad credit borrowers is the fact that there are a number of government programs that are solely created to offer homeownership to those people who find it difficult to get conventional bank loans. The following programs should be considered:

- FHA Loans: These loans are guaranteed by the Federal Housing Administration and require a credit score as low as 500 with a down payment of 10% or 580 with a down payment of a mere 3.5%.

- They are the most sought after when it comes to first-time buyers with bad credit.

- VA Loans: VA loans are open to active military members, veterans and eligible surviving spouses. No minimum credit score is established by the Department of Veterans Affairs, but individual lenders might have their own.

- These loans may not even have a down payment.

- USDA Loans: Offered to consumers who purchase properties in the countryside or suburbs.

- These loans are easy to secure credit and in some cases no down payment is even necessary to get the loan to the right low-to-moderate income buyer.

- State and Local Programs: There are numerous state, county or city first time buyer assistance programs with less stringent credit requirements.

- Browse programs in your area.

Step 5: Think of a Co-Signer or Co-Borrower

Although your credit score may not be high enough to secure a loan, the presence of a creditworthy co-signer or co-borrower can make a big difference.

The co-signer is typically a close family member or a friend that has a good credit history and is willing to assume the legal responsibility of the loan should you default on the payment.

- Lenders will consider the credit score and financial background of the co-signer in addition to yours, which can dramatically increase your chances of approval, and may even allow you to get a lower interest rate.

- Nevertheless, there is some great responsibility connected with this arrangement. Missing payments hurt the credit score of the co-signer and cause a rift in your relationship.

- Join this agreement with the understanding that you will fulfill your payments on a monthly basis.

Step 6: Shop Around and Compare Multiple Lenders

This is a very important step and one that most bad credit borrowers fail to attend to. The policies, the risk tolerance and pricing structure of various lenders vary widely. One large conventional bank may decline your loan request, and a credit union, a local bank or a specialty on-line lender may grant the very same loan with fair conditions.

There are four types of lenders to take into consideration when purchasing a mortgage:

- Credit unions: Banks owned by individual members, which often are more lenient and community-oriented than large banks.

- Community banks: Smaller local banks which can sometimes base their lending decisions on the big picture of your finances rather than your score.

- Internet mortgage lenders: There are a number of mortgage lenders that focus on bad credit or bad borrowers, and they may be able to provide good rates.

- Mortgage brokers: These are those professionals who deal with dozens of lenders and might offer the perfect solution to your needs.

Always get quotes with no less than three or five lenders, compare the interest rates, fees, closing costs and loan terms, and decide.

Step 7: Exude Financial Stability in other manners

Although your credit score is relevant, lenders also consider your big financial picture. By showing stability and responsibility in other aspects.

You can build your application to a great extent:

- Be consistently employed: Lenders want borrowers to have worked at the same employer at least two years. In case of self-employment you have two years of tax returns.

- Demonstrate consistent income: Submit recent pay stubs, bank statements, and tax returns to prove consistent income.

- Maintain a low debt-to-income ratio: This indicates the total amount of money you pay in debt each month against the total gross amount of your monthly income. Most lenders want this below 43%. It can help to pay off a car loan or credit card first.

- Have healthy savings: Saving between 3 to 6 months of mortgage payments is a reserve that shows the lender that you can manage any unexpected financial problems.

Why a Bad Credit Mortgage will Cost you More

One should be realistic about this process. Although you can get a mortgage with bad credit, you will end up paying more than a borrower with excellent credit. The gap between the interest rates might be minimal on paper, but at the end of a Loan, this gap can be extremely large.

Here is an example based on a $200,000 home loan over 30 years:

| Credit Profile | Interest Rate | Monthly Payment | Total Interest Paid |

| Excellent (750+) | ~6.5% | ~$1,264/month | ~$255,000 |

| Fair (650) | ~7.5% | ~$1,398/month | ~$303,000 |

| Bad (580) | ~9.0% | ~$1,609/month | ~$379,000 |

As this table shows, a bad credit borrower could end up paying over $120,000 more in interest than an excellent credit borrower over the same 30-year period. This is exactly why improving your credit score even by a small amount before applying is so worthwhile.

Common Mistakes to Avoid

Some bad credit borrowers make errors unknowingly which limits their possibilities of being approved, or increases their mortgage costs.

Avoid these common pitfalls:

- Using more than one lender at a time: Every hard credit pull will decrease your score by a few points. Yet, several mortgage inquiries done within the 14 to 45 day period are usually considered a single inquiry. So implement tactically over a period of time.

- Missing out on pre-approval: It is always better to pre-approve yourself before commencing a house hunt as it saves time and it can send a strong message to the sellers that you are a serious buyer. It also gets you to know precisely how much you can borrow.

- Disregarding the debt-to-income ratio: A lot of borrowers are just interested in the credit score and ignore the fact that creditors also examine a percentage of your monthly income that is spent on paying debts. Pay off smaller debts first with an attempt.

- Failing to read the fine print: Certain lenders who have targeted bad credit borrowers have hidden fees, prepayment penalties or balloon payment written in the loan document. Make sure you read through all the terms or get a professional to read them.

How to Start a Credit Building Process After a Mortgage

Obtaining a mortgage is a big accomplishment. However, the voyage is not finished there. Take a chance to reestablish your credit using your mortgage to enhance your future finances.

In the long run, one of the most effective methods of improving your credit score is to make regular mortgage payments.

Always pay all the mortgage payments in time. A single missed payment can be extremely harmful to your credit and to your relationship with the lender.

Use your bank to make automatic payments so you do not miss a payment date. Keep the rest of your debts, credit cards, car loans, etc. to a minimum.

Check your credit score periodically (a few times a year) and see how you are improving with free apps and services like Credit Karma or your bank app.

Consider refinancing your mortgage after 12-24 months of continually on-time payments. Having a better credit rating, you might get a much lower interest rate which can save you hundreds of dollars a month.

Final Thoughts

Getting a mortgage with bad credit is not impossible it simply requires more preparation, patience, and the right strategy. While a low credit score does create additional hurdles, lenders like FHA, VA, and USDA programs exist specifically to help borrowers who do not fit the traditional mold of conventional financing.

The most important thing you can do right now is take an honest look at your credit situation. Pull your credit report, dispute any errors, pay down existing debt where possible, and avoid opening new lines of credit before applying. Even small improvements in your credit score can unlock better interest rates and lower down payment requirements saving you a significant amount of money over the life of your loan.

If your credit is not quite where it needs to be, do not be discouraged. A few months of focused effort can make a meaningful difference. In the meantime, explore all available loan options, compare multiple lenders, and consider working with a HUD-approved housing counselor who can guide you through the process at no cost.

Remember, buying a home is one of the biggest financial decisions of your life. Taking the time to strengthen your credit profile before applying is not a delay it is a smart investment in your financial future.

Bad credit may slow you down, but with the right plan, homeownership is still well within your reach.