loanDepot Review 2026 Rates Loan Types Pros and Cons

loanDepot is one of those mortgage lenders that almost everyone has heard of but very few people actually understand before they apply. Founded in 2010, the company has grown into the second-largest non-bank mortgage lender in the United States, funding over $275 billion in home loans since it launched. That kind of scale means something: they have closed loans in every state, across nearly every loan type, in all kinds of market conditions. But scale alone does not make a lender right for you.

This loanDepot review is not a press release. I went through the actual HMDA data, read through more than 4,300 real customer reviews on Trustpilot, looked at the J.D. Power satisfaction scores, reviewed every loan product they offer, and yes, I covered the 2024 data breach because any honest review has to. By the end of this, you will know exactly who loanDepot is right for and who should keep looking.

What Is loanDepot and How Does It Work?

loanDepot is a non-bank direct lender, which means it lends its own money rather than acting as a broker connecting you to other lenders. It is headquartered in Irvine, California, licensed to originate loans in all 50 states, and operates through a hybrid model that sits between fully online lenders like Rocket Mortgage and traditional brick-and-mortar banks.

loanDepot operates over 200 branches nationwide while also offering a full digital application through its mello smartloan platform, which is the best way to describe what makes this lender distinct. You can apply entirely online, manage your documents through a centralized dashboard, communicate with your loan team by text or email, and in many states even close your loan electronically without setting foot in an office. Or, if you prefer talking to a person, you can walk into one of those 200 branches or call their loan officers directly.

That hybrid approach is genuine, not marketing. Most loanDepot customers never visit a branch. But the option matters for buyers who get anxious about managing a $400,000 financial decision entirely through a website.

loanDepot Loan Products: What They Actually Offer

This is where loanDepot genuinely stands out from most of its competitors. The loan menu is wide, and it includes several products that large banks and even some big non-bank lenders will not touch.

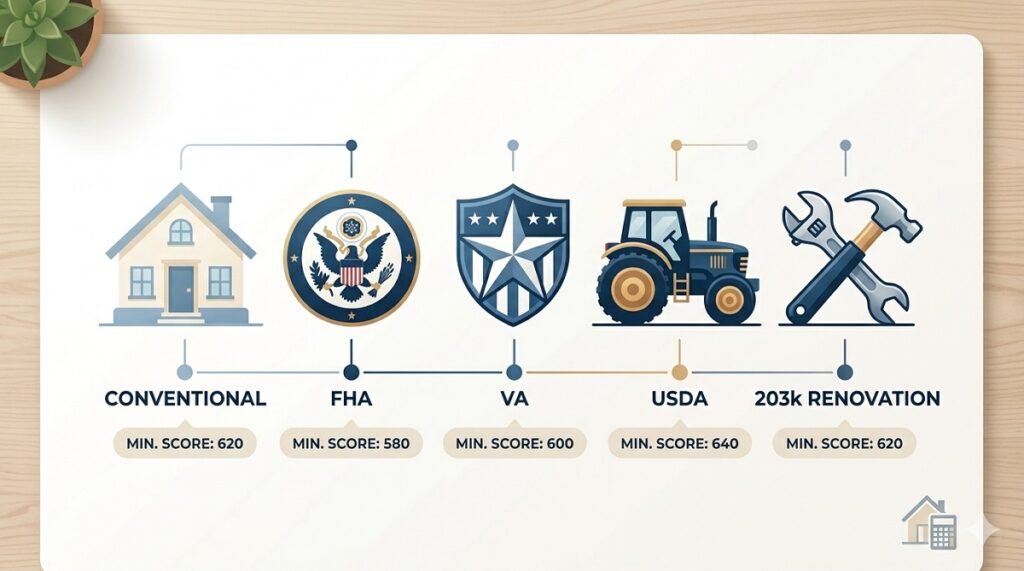

Conventional Loans

loanDepot requires a minimum 620 credit score for conventional loans with a minimum 3% down payment. Standard 30-year and 15-year fixed-rate options are available, as well as adjustable-rate mortgages (ARMs) with initial fixed periods of 3, 5, 7, or 10 years. For a buyer with a 680 credit score putting 10% down on a $380,000 home, loanDepot is a legitimate option worth getting a quote from, though not guaranteed to be the cheapest.

FHA Loans

loanDepot accepts credit scores as low as 520 for FHA loans, with a 3.5% down payment required for scores of 580 and above. FHA loans (Federal Housing Administration backed loans) are designed for buyers with lower credit scores or limited savings who cannot qualify for a conventional loan. If your score is between 500 and 579, FHA technically allows you in with 10% down, and loanDepot honors that floor. Most major lenders quietly require 580 or even 620 as their internal minimum even for FHA, so the 520 floor is a genuine differentiator.

FHA 203k Renovation Loans

This is one of loanDepot’s clearest advantages. The FHA 203k renovation loan wraps the purchase price and renovation costs into a single mortgage, allowing buyers to finance repairs using the future appraised value of the home after improvements rather than just the current as-is value. A buyer purchasing a $260,000 fixer-upper in need of $40,000 in repairs can borrow against a $300,000 post-renovation value with just 3.5% down on the combined amount. Most lenders do not offer this product at all, and those that do often lack the experience to close them on time. loanDepot closes thousands of these annually.

loanDepot requires a minimum 620 credit score for its FHA 203k loans, and renovation funds are held in escrow and released to contractors as work milestones are completed.

VA Loans

loanDepot accepts credit scores as low as 520 for VA loans, which are reserved for eligible veterans, active duty service members, and qualifying surviving spouses. VA loans require no down payment and no private mortgage insurance. loanDepot’s 520 minimum for VA is significantly below what most lenders advertise (typically 620), giving recently transitioned veterans with thin credit files a real path to homeownership that competitors close off.

USDA Loans

loanDepot offers USDA loans with no down payment required and a minimum 620 credit score. USDA loans are available only for properties in designated rural and suburban areas, and borrowers must meet income limits set by the US Department of Agriculture. For buyers in qualifying areas who cannot afford a down payment, this is a zero-down option that does not carry the VA’s funding fee.

Jumbo Loans

loanDepot issues jumbo loans up to $5 million with a minimum 660 credit score required, covering purchases that exceed the conforming loan limit of $832,750 for most US counties in 2026. Jumbo loans carry stricter underwriting requirements and typically higher rates, but loanDepot’s willingness to go up to $5 million makes them a viable option for luxury buyers.

HELOC and Home Equity Loans

loanDepot offers home equity loans in 10, 20, and 30-year terms with loan amounts from $35,000 to $400,000, and HELOCs ranging from $35,000 to $400,000 for first-lien positions. The minimum credit score for home equity products is 640. One honest drawback: when your HELOC closes, loanDepot requires you to withdraw at least 75% of the funds immediately, or 100% if borrowing less than $50,000. If you want a HELOC as an emergency fund you may not need to touch, this mandatory draw policy makes loanDepot a poor choice. Pull the money only when you need it is a feature most HELOC users want, and loanDepot does not offer it.

Use our free affordability calculator to see how much home you can realistically qualify for before requesting a rate quote from any lender.

The loanDepot Lifetime Guarantee: Is It Actually Worth It?

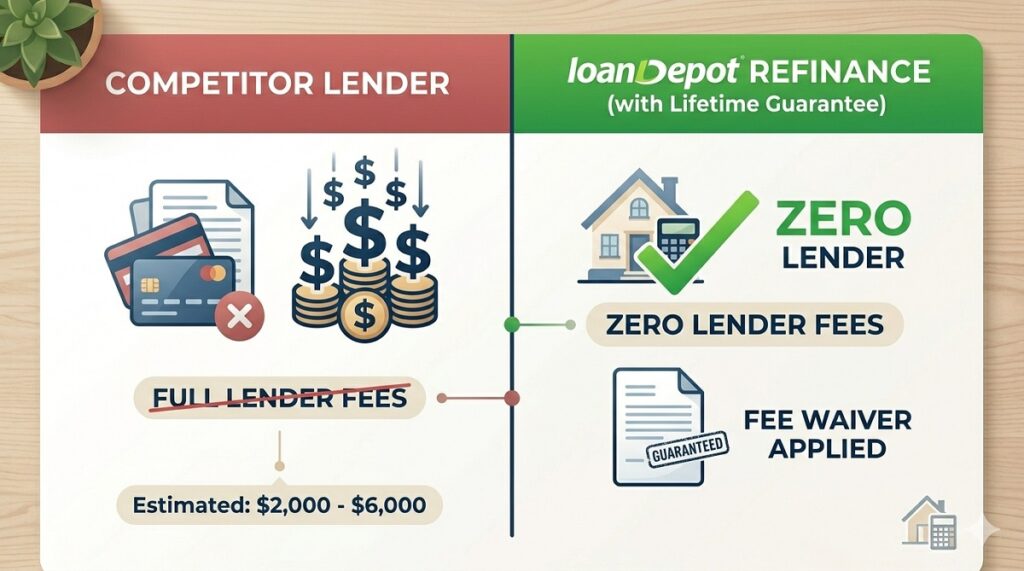

The Lifetime Guarantee is loanDepot’s most talked-about feature and genuinely the best reason to consider them over a competitor with a slightly lower rate today.

When you close your first mortgage with loanDepot, you are automatically enrolled in the Lifetime Guarantee at no extra cost. If you refinance that same property through loanDepot in the future, the company waives its lender fees, including origination charges, processing fees, and underwriting fees. You still pay third-party costs like appraisal, title, and recording fees, but the lender portion is eliminated.

On a $400,000 loan, the lender fees typically run $2,000 to $6,000, meaning the Lifetime Guarantee saves that entire amount when you refinance.

Here is when it actually makes sense. If you are buying in 2026 at today’s rates around 6.5% to 7% and you expect rates to drop to 5% to 5.5% within the next three to five years, the Lifetime Guarantee means your future refinance with loanDepot costs $2,000 to $6,000 less than refinancing with a different lender. That is real money, and it tips the scales toward loanDepot even if their rate today is 0.125% higher than a competitor.

Here is when it does NOT make sense. If you are buying in a lower-rate environment and have no realistic expectation of refinancing, the guarantee adds no value. You would be better off optimizing entirely for today’s rate and choosing whichever lender is cheapest right now.

Use our free refinance calculator to model the break-even point on a future refinance at different rate scenarios before deciding how much the Lifetime Guarantee is actually worth to you.

loanDepot Rates and Fees: The Honest Picture

This is where loanDepot gets complicated. loanDepot does not post mortgage rates on its website. To see what rate you qualify for, you must submit contact information and enter their application process. That is a genuine frustration for buyers who want to comparison shop quickly.

According to NerdWallet’s analysis, loanDepot’s mortgage rates and fees tend to run slightly higher than the average of lenders they surveyed. This is consistent with what I found across multiple sources. loanDepot is not trying to be the cheapest lender on the block. Their average origination fee as of 2023 HMDA data was approximately $4,909 per loan, which is on the higher end compared to competitors.

The practical implication is this: if you have a 760 credit score, a 20% down payment, and straightforward W-2 income, you can almost certainly find a lower rate from a wholesale broker working through UWM, or from a leaner digital lender. loanDepot’s pricing is competitive for borrowers with more complex profiles or lower credit scores who value the full-service experience, but it is mid-pack for prime borrowers.

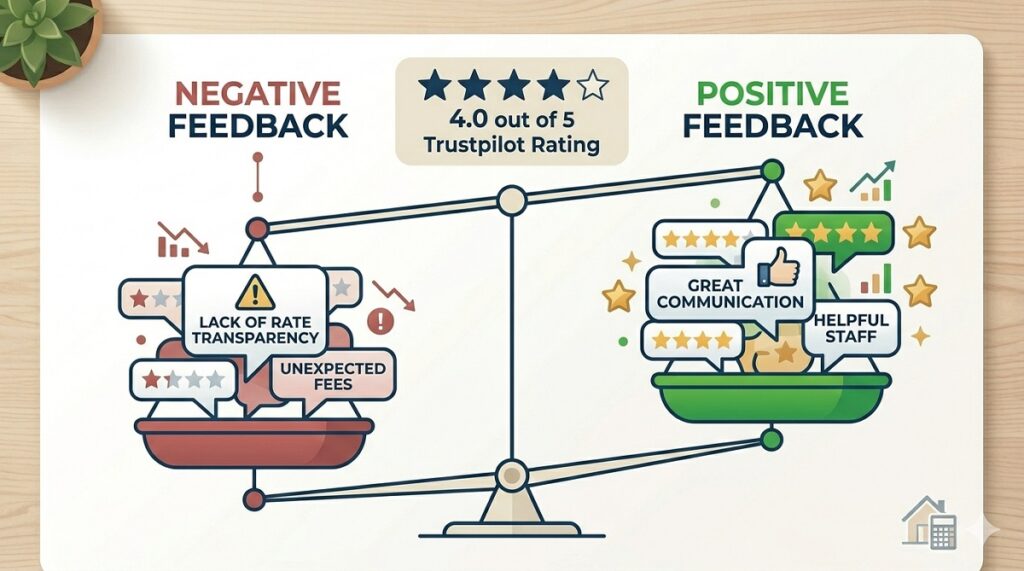

loanDepot scored 3.4 out of 5 stars from Bankrate on affordability, specifically citing the lack of APR transparency as a drawdown factor.

loanDepot Customer Reviews: What Real Borrowers Say

loanDepot holds a 4 out of 5 rating on Trustpilot based on real customer reviews, and underwrote over 70,000 mortgages with very few formal complaints logged with the CFPB. That CFPB complaint volume relative to loan count is a meaningful signal. It means the vast majority of loanDepot borrowers get through the process without a complaint serious enough to file with the federal consumer protection bureau.

The positive reviews consistently highlight responsive loan officers, smooth document management through the mello platform, and appreciation for being kept informed throughout the process. Many buyers mention that their loan officer was easy to reach by text or email, which matters more than most people realize when you are juggling a home purchase and trying to get answers quickly.

The negative reviews cluster around two issues. First, some borrowers report receiving aggressive follow-up calls and emails after submitting contact information but before formally applying. Several customers on LendingTree noted receiving multiple phone calls per day after shopping around, sometimes even after choosing a different lender entirely. If you submit your information to loanDepot expecting a quiet experience, that is not always what happens.

Second, some borrowers report communication gaps during underwriting, particularly on more complex loan files. Positive reviews highlight a smooth digital application process, but numerous customers also report frustrations with communication inconsistencies and unexplained delays near closing.

On J.D. Power’s 2025 Mortgage Origination Satisfaction Study, loanDepot scored below the industry average, while on the 2025 Mortgage Servicing Satisfaction Study, the company ranked well above average. That split is telling. Getting through the application and closing process with loanDepot is where buyers sometimes have friction. Managing the loan after closing is where loanDepot actually performs well.

The 2024 Data Breach: What You Need to Know

Any honest loanDepot review in 2026 has to address this directly.

In January 2024, loanDepot suffered a ransomware attack in which the personal data of nearly 17 million customers was stolen, including names, dates of birth, email and postal addresses, financial account numbers, phone numbers, and Social Security numbers.

The attack cost loanDepot $26.9 million in total expenses, including investigation costs, customer notifications, identity protection services, legal fees, and a $25 million class action settlement. The ransomware group ALPHV/BlackCat claimed responsibility.

loanDepot notified all affected customers and offered free credit monitoring and identity protection services after the breach was confirmed. The company has since restored its systems and says it has implemented additional security measures, though the specifics of those measures have not been publicly detailed.

Whether this affects your decision to apply with loanDepot in 2026 is a personal call. The breach happened. The data was stolen. The settlement was paid. loanDepot is still a large, fully operational lender that closed tens of thousands of loans in 2025. But if data security is a top priority for you, this is information you should have before you decide.

loanDepot vs Competitors: How It Stacks Up

Against Rocket Mortgage: Rocket has a better app, more polished digital experience, and posts rates online. loanDepot counters with the Lifetime Guarantee, a wider specialty loan menu including 203k and USDA, and VA credit score minimums that go as low as 520 versus Rocket’s typical 580 floor. For prime borrowers wanting the best digital experience, Rocket wins. For borrowers with lower scores or who plan to refinance, loanDepot often makes more sense.

Against CrossCountry Mortgage: CrossCountry has more flexibility for self-employed buyers and non-QM (non-qualified mortgage) loan options. loanDepot is the stronger choice for FHA 203k renovation loans and has more branch locations for buyers who want occasional in-person access.

Against a local credit union: A local credit union will almost always beat loanDepot on rate for borrowers with strong credit. Where loanDepot wins is speed, loan variety, and the Lifetime Guarantee. If you are buying in a competitive market and need to close in 21 days, a credit union that takes 45 days is not the right tool.

Who Should Use loanDepot in 2026

loanDepot makes the most sense for a specific type of borrower.

Buyers in a high-rate environment who expect to refinance within three to five years get genuine long-term value from the Lifetime Guarantee that offsets paying a slightly higher rate today. A buyer locking in at 6.75% today who refinances at 5.25% in two years and saves $4,000 in lender fees has come out ahead of the borrower who went with the cheaper lender at 6.625% and paid full closing costs on both loans.

Buyers with credit scores between 520 and 580 who need an FHA or VA loan and are finding most lenders turning them away at 580 have a real path through loanDepot’s lower floors.

Buyers purchasing fixer-uppers who need an FHA 203k loan are well served by loanDepot’s experience and volume in this product category.

Buyers who want digital convenience with the safety net of in-person access find the hybrid model appealing. Not everyone is comfortable managing a major transaction entirely through a website.

Check our private mortgage lenders guide if you are considering alternatives outside traditional lender options, and use our mortgage rate comparison tool to benchmark whatever rate loanDepot quotes you against the current market before you commit.

Who Should NOT Use loanDepot

Being direct here saves you time.

If you have a 740-plus credit score, a 20% down payment, and straightforward W-2 income, you can almost certainly get a lower rate from a wholesale broker, a leaner digital lender, or a credit union. loanDepot’s mid-pack pricing is not where prime borrowers get the best deal.

If you need weekend customer service, loanDepot’s phone lines are only available Monday through Friday, 10am to 9pm ET. loanDepot’s customer service line is not available on weekends. For buyers in active negotiations over a weekend who need immediate lender responses, this is a genuine gap. Texas State Affordable Housing Corporation

If you want to compare rates without entering a marketing funnel, loanDepot will frustrate you. You cannot see a rate without submitting contact information and receiving follow-up calls. If that process bothers you, start with a lender that posts rates publicly.

If you need a HELOC as a true emergency reserve and want to draw funds only when needed, loanDepot’s mandatory 75% initial draw requirement makes them the wrong product for that use case.

Use our loan eligibility checker to see what loan types and amounts you realistically qualify for before approaching any lender, including loanDepot, so you walk in with accurate expectations.

loanDepot Quick-Reference Summary

Founded: 2010, Irvine, California. Available in all 50 states and Washington DC. Over 200 branch locations nationwide.

Minimum credit scores: 620 for conventional, 520 for FHA, 520 for VA, 620 for USDA, 660 for jumbo, 640 for HELOC and home equity loans.

Minimum down payments: 3% for conventional, 3.5% for FHA, 0% for VA, 0% for USDA.

Loan types: Conventional, FHA, FHA 203k renovation, VA, USDA, jumbo, HELOC, home equity loans, cash-out refinance, rate-and-term refinance, doctor loans, ITIN loans, interest-only loans, reverse mortgages, and loans for self-employed borrowers.

Standout feature: Lifetime Guarantee waiving lender fees on future refinances.

Trustpilot rating: 4.0 out of 5 from over 4,300 reviews.

J.D. Power origination score: Below average. J.D. Power servicing score: Above average.

Rates posted online: No. You must submit contact information to receive a rate quote.

DISCLAIMER BLOCK

This article is for informational purposes only and does not constitute financial or legal advice. Mortgage rates, loan limits, fees, and program requirements change frequently. Always verify current details directly with loanDepot and consult a licensed mortgage professional before making any financial decisions.

: Compare Top Options")