No Income Verification Mortgage Lenders 2026 Real Options Explained

If you have spent any time searching for a mortgage without W-2s or tax returns, you have probably run into two problems. The first is lenders who tell you flat out that they cannot help you. The second is websites that talk about no income verification mortgages as if they still work the way they did before 2008, when a borrower could literally state any income number on a form and a lender would approve it without asking a single follow-up question.

Neither of those experiences is particularly useful if you are a real estate investor, a retiree living on investments, a self-employed business owner with aggressive tax write-offs, or anyone else whose ability to repay a mortgage does not fit neatly into a pay stub.

No income verification mortgage lenders do exist in 2026. What they offer is not the reckless lending of the pre-crash era. It is a genuinely different approach to proving you can repay a loan, one that uses bank deposits, property cash flow, liquid assets, or a combination of these instead of a W-2. The programs are real, they close regularly, and the right borrower can access them without compromising on home quality or purchase price.

This guide explains exactly what is legal and available, what each program actually requires, which lenders are worth talking to, and where every option falls short so you go in with accurate expectations.

The Legal Reality: What No Income Verification Actually Means in 2026

Before anything else, this distinction needs to be clearly understood because it affects every conversation you will have with a lender.

The Dodd-Frank Act and the Ability-to-Repay rule from the Consumer Financial Protection Bureau require lenders to verify a borrower’s ability to repay using verifiable financial information before approving any mortgage. As a result, true no-doc loans are no longer legal for primary residences. The only exceptions are certain non-qualified mortgage products like bank statement and asset-based loans, which still require proof of repayment capacity through alternative methods. WalletHub

What this means practically: the loans that existed before 2008 where a lender took a borrower’s stated income entirely at face value and never checked anything are gone. No-income, no-job, no-assets NINJA loans became nearly nonexistent after the 2007 to 2008 financial crisis. Any lender today who offers you a genuine NINJA loan on a primary residence is operating outside the law, and you should walk away from that conversation immediately. WalletHub

What does exist in 2026 is a well-developed market of alternative documentation loans, broadly called non-QM (non-qualified mortgage) loans, that verify your ability to repay through means other than traditional employment income. Modern no-doc loans are actually alt-doc or non-QM loans. True blind approvals no longer exist in the 2026 market. Lenders still verify your ability to repay, just through non-traditional metrics such as bank deposits, liquid assets, or property cash flow rather than tax returns. Bankrate

The practical result is that a borrower who genuinely cannot produce W-2s or qualifying tax returns has multiple legitimate, federally compliant paths to homeownership. They just need to know which path fits their specific financial profile.

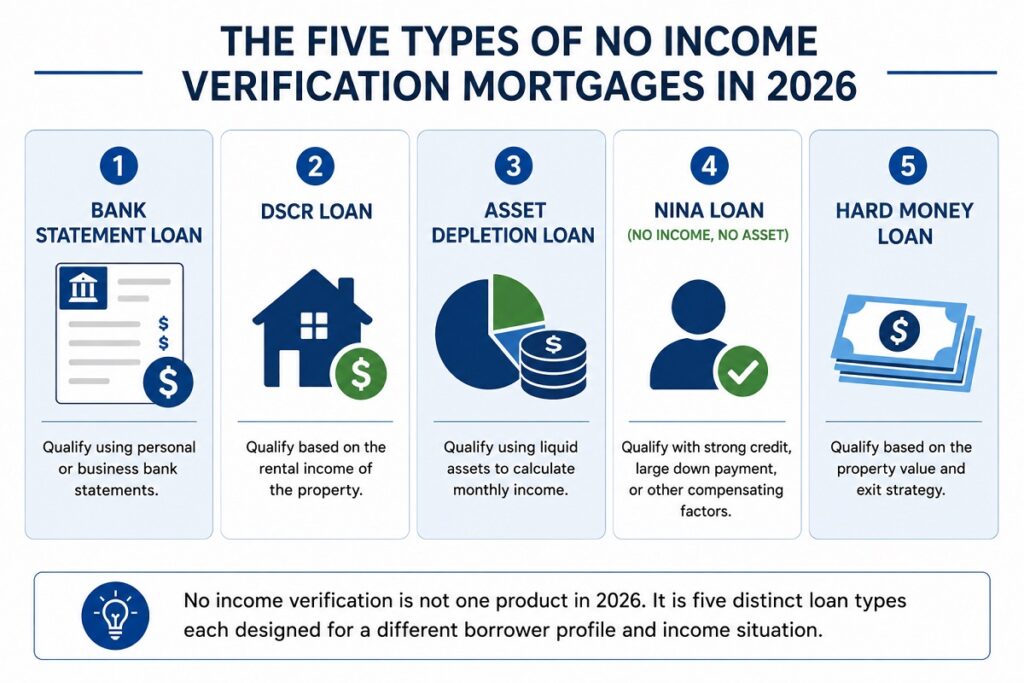

The Five Types of No Income Verification Mortgages Available in 2026

These five loan structures cover the vast majority of borrowers who need alternative income documentation. Each one serves a different financial profile.

Type One: Bank Statement Loans

Bank statement loans are the most widely used alternative documentation product for self-employed borrowers, freelancers, and gig economy workers. SIVA loans, sometimes called bank statement loans, use 12 to 24 months of bank statements instead of traditional income documents, skipping the income review in favor of verified cash flow documentation. The Truth About Mortgage

The lender reviews your monthly deposits across 12 or 24 months, applies an expense factor of 40% to 50% to account for embedded business costs, and uses the remaining figure as your qualifying monthly income. A business owner depositing an average of $14,000 per month who had $70,000 in Schedule C deductions on their tax return qualifies based on $7,000 to $8,400 in monthly income through bank statement underwriting rather than the $4,200 their tax return would show.

Bank statement loans replace W-2s with 12 to 24 months of statements and are legal, regulated non-QM loans overseen by the CFPB. They typically require a minimum 620 to 660 credit score, a down payment of 10% to 25%, and two years of documented self-employment history. Reverse Mortgage

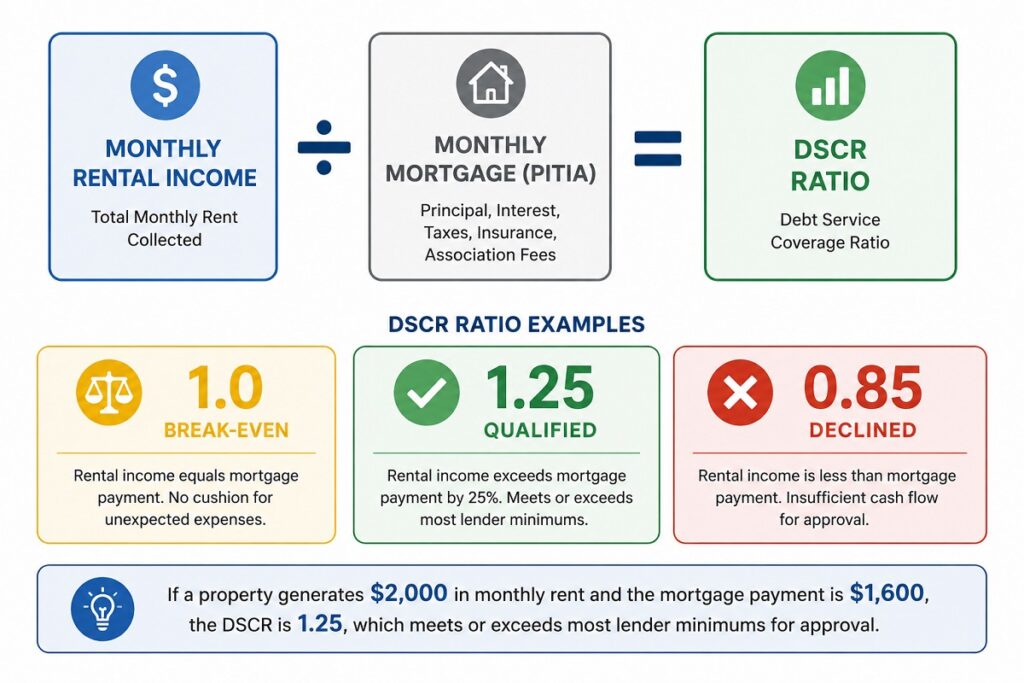

Type Two: DSCR Loans

DSCR stands for debt service coverage ratio, and this loan type is specifically designed for real estate investors. It is the closest thing to a truly income-neutral mortgage that legally exists today because it qualifies based entirely on the property being purchased rather than the borrower’s personal finances.

DSCR loans work by focusing entirely on the property’s rental income rather than the borrower’s personal finances. Lenders calculate the debt service coverage ratio by dividing the property’s gross monthly rent by its total monthly debt obligations including principal, interest, taxes, insurance, and HOA fees. No W-2s, tax returns, or employment verification are required. FHA.com

A DSCR of 1.0 means the property’s rental income exactly covers the mortgage payment. A DSCR of 1.25 means the property generates 25% more rent than it costs to carry. Most lenders require a minimum DSCR between 1.0 and 1.25, a credit score of 660 or higher, and a down payment of 20% to 25%. Current DSCR loan rates in 2026 typically range from 6.0% to 8.0% depending on credit score, LTV, and property cash flow. Atlantarealestateforum

Type Three: Asset Depletion Loans

Asset depletion loans are designed for borrowers who have built substantial wealth but show little or no documented income, primarily retirees, people who sold a business, and high-net-worth individuals who live on investment returns rather than a salary.

An asset depletion mortgage loan converts verified liquid assets into a calculated monthly income figure, allowing borrowers to qualify without W-2s, pay stubs, or tax returns. The lender does not require the borrower to actually spend down their assets. They simply use the math to prove sufficient wealth to support monthly mortgage payments over the life of the loan. Alpine Mortgage

The calculation works by dividing total eligible liquid assets by the number of months in the loan term, or a shorter divisor at some lenders. A borrower with $900,000 in liquid assets divided by 360 months produces a qualifying income of $2,500 per month. Some lenders use 240 months instead of 360, raising that figure to $3,750 per month and increasing purchase power substantially.

Asset depletion mortgages generally require higher credit scores than conventional loans. Most non-QM and portfolio lenders set a floor of 680 FICO, with the majority of competitive programs requiring 700 to 720 minimum. Borrowers with scores above 740 access the lowest available rates, currently pricing around 6.25% to 7.50% for 75% LTV scenarios in 2026. Alpine Mortgage

Type Four: NINA Loans for Investment Properties

NINA loans, meaning no income and no asset verification, require no income or asset verification and are reserved for experienced investors purchasing non-owner-occupied properties. On a NINA loan, the lender does not look at your personal income or your personal assets at all. Qualification rests entirely on the property’s rental income potential and the borrower’s credit score. The Truth About Mortgage

NINA loans are geared toward mortgages for investment properties specifically. The lender looks at the rental income potential of the property. If the rental property’s potential cash flow can cover the monthly payment, a NINA loan is a potential option. CNBC

NINA products are typically available only through specialized non-QM lenders and hard money shops. They carry higher rates and larger down payment requirements than standard DSCR loans, generally 25% to 30% or more, and are not suitable for primary residences.

Type Five: Hard Money and Private Loans

Hard money loans are asset-based bridge loans offered by private investors and specialty lenders, not traditional financial institutions. They are typically short-term loans of 6 to 24 months used for property acquisition or renovation projects.

NINJA-style loans with no documentation at all are largely limited to hard money lenders today. A hard money lender will approve based almost entirely on the property’s value and the borrower’s equity stake. Your income, your tax returns, and your employment history are essentially irrelevant. The Truth About Mortgage

The honest cost: hard money interest rates typically run 10% to 15% or higher, with origination fees of 2% to 5% of the loan amount. On a $300,000 purchase, you might pay $6,000 to $15,000 in origination fees alone plus an annual rate that produces a monthly interest payment of $2,500 to $3,750. Hard money is a tool for short-term real estate transactions with a clear exit strategy, not a long-term homeownership vehicle.

Use our free mortgage rate comparison tool to see how non-QM rates compare to current conventional rates before committing to any alternative documentation program.

DSCR Loans: The Purest Form of No Income Verification Mortgage

DSCR loans deserve their own detailed section because they are the most commonly misunderstood product in this category, and the borrowers who benefit most from them often do not know the product exists.

The DSCR formula is straightforward. Monthly gross rental income divided by monthly PITIA (principal, interest, taxes, insurance, and association fees) equals your DSCR. If a property rents for $2,000 per month and the total monthly mortgage payment is $1,600, the DSCR is 1.25. Most lenders will approve this. If the rent is $1,500 and the payment is $1,600, the DSCR is 0.94, which falls below the 1.0 minimum at most lenders.

In 2026, most qualified DSCR borrowers are seeing rates in the 6.0% to 10.75% or higher range depending on credit score, down payment and LTV, DSCR ratio, property type, and loan term. A 1.3 or higher DSCR gets better pricing than a 1.05 DSCR, and a 700-plus credit score gets significantly better pricing than 620. Rocket Mortgage

One feature of DSCR loans that most lenders do not proactively mention: if your property is vacant or currently rented below market rate, lenders use an appraiser’s market rent estimate rather than the actual rent to calculate the DSCR. If your property rents for $2,200 per month but the appraiser determines market rent is $2,800, the lender uses $2,800 in the calculation. This can turn a borderline-qualifying property into a clear approval simply by demonstrating what the market supports. FHA.com

DSCR loan rates run higher than conventional mortgage rates for primary residences, reflecting the increased risk lenders associate with investment property financing and the absence of personal income verification. DSCR loan interest rates typically run 1% to 2% higher than standard conventional investment property rates. But the trade-off that serious investors consistently cite: conventional loans cap you at 10 financed properties. DSCR loans have no such limit. For investors scaling a portfolio past the conventional limit, DSCR loans are not just an alternative. They are the only path. AtlantarealestateforumLendingTree

DSCR loans require a 20% minimum down payment in most cases. Some programs allow 15% down with stronger credit and DSCR ratios. Cash reserves of 3 to 6 months of PITIA per financed property are required in liquid form after closing. HUD

Most DSCR loans come with prepayment penalties. A common structure is a 5-year step-down, meaning if you sell or refinance in the first five years, you pay a fee that decreases each year. Typically the penalty is 5% in year one, 4% in year two, down to 1% in year five. Factor this into your hold strategy before signing. Propertyprosatlanta

Use our free mortgage calculator to model the monthly PITIA on any investment property scenario before submitting to a DSCR lender, so you know whether your target property’s rent income actually supports the ratio.

Asset Depletion Loans: For Retirees and Wealth-Heavy Borrowers

The typical asset depletion borrower is someone who has done everything right financially: saved diligently, built a substantial investment portfolio, possibly sold a business, and now finds themselves asset-rich but income-poor on paper at exactly the moment they want to buy a home.

A retired couple with $1.4 million in a combination of brokerage accounts, IRAs, and savings accounts but only $36,000 per year in Social Security income would not qualify for a $450,000 mortgage through conventional underwriting. Their income-based DTI would be catastrophic. Through asset depletion underwriting, their $1.4 million divided by 240 months produces qualifying income of $5,833 per month, which supports a significantly larger mortgage with comfortable DTI margins.

An asset depletion mortgage converts liquid assets into qualifying income by dividing verified assets over a set period, typically 60 to 84 months at some lenders and up to 360 months at others. No employment income, tax returns, or W-2s are required. U.S. News & World Report

Eligible assets typically include checking and savings accounts, money market accounts, certificates of deposit, stocks and bonds, mutual funds, and retirement accounts at a discounted percentage, commonly 60% to 70% of the account value to account for early withdrawal penalties and taxes. Real estate equity, personal property, and business holdings generally do not qualify unless they can be liquidated and documented. The Truth About Mortgage

The minimum asset threshold matters. Qualifying typically requires $500,000 to $1,000,000 or more in liquid assets depending on the desired loan amount, far more than most borrowers have. Lenders also require 3 to 12 months of reserves in addition to the assets used for income calculation, meaning you cannot deploy every dollar toward qualification. The Truth About Mortgage

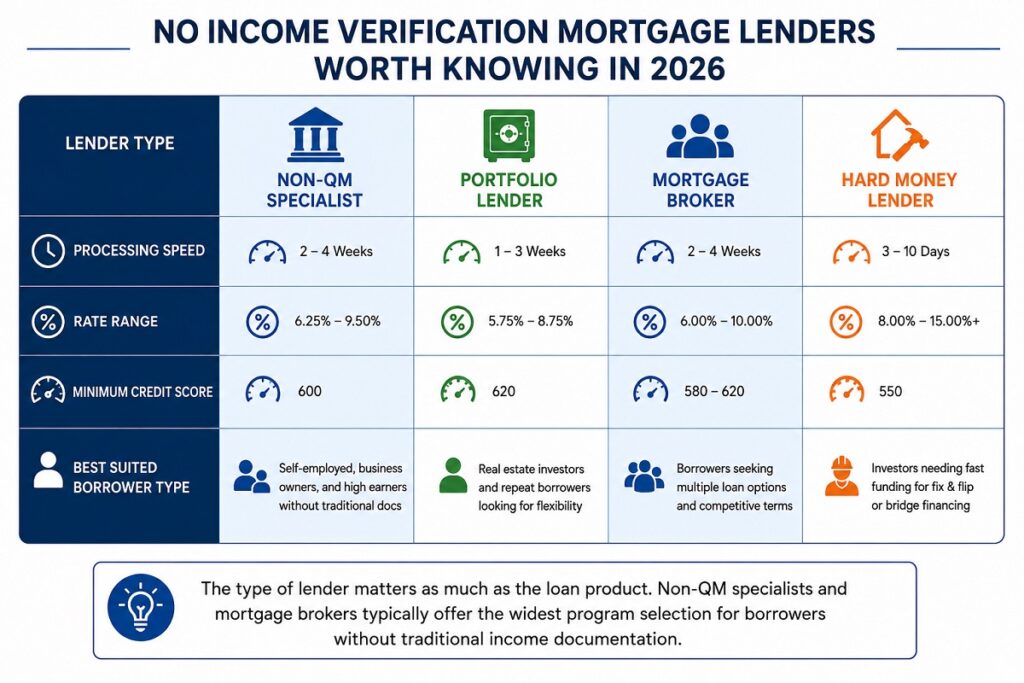

No Income Verification Mortgage Lenders Worth Knowing in 2026

These are the lender categories and specific names that consistently close alternative documentation loans. Finding the right fit depends entirely on your loan type and borrower profile.

CrossCountry Mortgage

CrossCountry is one of the most active retail lenders for non-QM products in the country. CrossCountry accepts credit scores as low as 500 for certain non-traditional mortgages, which is significantly below the 620 minimum that most non-QM lenders enforce. They offer bank statement loans, DSCR products, asset depletion programs, and 1099-only loans under one roof, with underwriters experienced in complex income structures. WalletHub

Their FastTrack underwriting process is a genuine differentiator. CrossCountry’s FastTrack review speeds up the underwriting process, allowing approved borrowers to close in as few as 10 days, which matters for investors buying in competitive markets or managing a closing timeline around a property under contract. WalletHub

Who this fits: Self-employed buyers with lower credit scores, investors needing DSCR products, and borrowers with multiple non-traditional income streams who need a single lender that handles all of them.

Angel Oak Mortgage Solutions

Angel Oak Mortgage Solutions is one of the largest non-QM lenders nationally and focuses exclusively on borrowers who do not fit conventional boxes. Their institutional specialization in non-QM means their underwriters and loan officers deal with alternative documentation files all day, every day, rather than handling them as exceptions to a primarily conventional workflow. U.S. News & World Report

Angel Oak offers bank statement loans on both 12 and 24-month programs, asset depletion products, 1099-only loans, DSCR investment property financing, and ITIN loans for borrowers without a Social Security number. Their rates are competitive within the non-QM space and their underwriting is thorough without being unnecessarily burdensome.

Who this fits: Borrowers who have been declined at retail lenders and need a specialist who treats non-QM as core business rather than an afterthought.

Quontic Bank

Quontic is a certified Community Development Financial Institution with a mission to serve underbanked communities and is one of the few community banks offering a full non-QM product line including no income verification options. Quontic offers bank statement loans, asset depletion products, and programs for borrowers with non-traditional income including cryptocurrency holders and foreign nationals. As a regulated bank, Quontic carries FDIC backing that gives some borrowers more confidence than dealing with a non-bank lender. WalletHub

Who this fits: Buyers with non-traditional income sources including crypto, foreign income, or investment returns who want the stability of a federally regulated bank behind their loan.

Griffin Funding

Griffin Funding specializes in bank statement loans for self-employed borrowers and offers competitive non-QM programs with loans up to $3 million using 12 to 24 months of bank statements. Their loan officers are experienced specifically with self-employed borrowers and understand the nuances of how different business structures affect income calculation, from single-member LLCs to S-corps to sole proprietors. The Mortgage Reports

Who this fits: Self-employed buyers and investors who need loan amounts above $1 million and want a lender with deep experience in bank statement underwriting at the jumbo level.

New American Funding

New American Funding offers DSCR loans for investment properties requiring a credit score of 620 or higher, a down payment of 20% to 25%, and cash reserves of 3 to 12 months of mortgage payments. They are a large retail lender with the operational scale to handle complex files efficiently, and their DSCR product is one of the most accessible in the market for new investors entering the rental property space. FHA.com

Who this fits: First-time real estate investors purchasing their first rental property who want the backing of a well-capitalized retail lender rather than a smaller specialty shop.

Working with a Mortgage Broker

For no income verification borrowers specifically, working with a mortgage broker rather than a single retail lender is often the smartest approach. Mortgage brokers who specialize in non-QM products connect borrowers with wholesale lenders and can compare rates and terms across multiple lenders simultaneously. A broker who closes multiple bank statement loans monthly works with at least three to five lenders and has current knowledge of which programs are most competitive for specific borrower profiles. U.S. News & World Report

The wholesale non-QM market has significantly more pricing competition than the retail market. A broker shopping your file across eight wholesale non-QM lenders will almost always find better pricing than a single retail lender quoting their own programs. The broker’s compensation comes from the lender, not from you, so this wider search costs you nothing extra.

Our guide on private mortgage lenders covers the broker and private lending landscape in more detail if you want to understand how wholesale non-QM pricing compares to what retail lenders quote.

Honest Trade-Offs: What No Income Verification Loans Actually Cost

Every alternative documentation loan comes with real costs that borrowers need to understand before they apply.

Rate premiums are real and significant. Expect higher interest rates and a larger down payment, typically 20% or more, as trade-offs for the faster, less document-intensive process compared to conventional loans. Bank statement loans run 0.25% to 0.50% above conventional rates at the best credit tiers, and can run 1.0% to 2.0% higher for lower credit scores or more complex income structures. On a $400,000 loan, a 1.0% rate premium equals roughly $222 per month and nearly $80,000 across a 30-year term. That is a real cost that deserves real consideration. Bankrate

Down payment requirements are larger. Most non-QM programs require 20% to 25% down on primary residences, and 25% to 30% on investment properties. The days of 3.5% down on a bank statement loan are essentially gone. On a $350,000 home, 20% down means $70,000 in cash, compared to $12,250 for an FHA loan.

Prepayment penalties are common. Most DSCR loans have a prepayment penalty with a 5-year step-down structure, meaning if you sell or refinance within the first five years, you pay a fee that decreases annually. If your plan involves refinancing to a conventional loan after two years of stronger tax returns, make sure the penalty structure on any non-QM loan does not make that refinance prohibitively expensive. Propertyprosatlanta

Fewer consumer protections apply. Non-QM loans fall outside the qualified mortgage safe harbor rules that provide lenders legal protection against ability-to-repay lawsuits. This means non-QM lenders carry more risk and pass that risk to borrowers through higher rates and stricter reserve requirements.

The refinance path is real but requires planning. Many borrowers use non-QM loans as a bridge, buying now with alternative documentation and then refinancing to a conventional loan once two years of higher taxable income are on their tax returns. Once you have two years of tax returns showing higher income, you can refinance to a conventional loan for a lower rate. Many borrowers do this after two to three years. Plan for the prepayment penalty timing when structuring this strategy. AZ Big Media

Use our refinance calculator to model the break-even point on refinancing from a non-QM loan to conventional once your income documentation improves, including the prepayment penalty cost in your total calculation.

Who Should and Should Not Use These Products

No income verification loans are genuinely the right tool for specific borrowers. They are the wrong tool for others, and being direct about this distinction saves time and money.

You are a good candidate for alternative documentation mortgage products if you are a self-employed business owner whose taxable income understates actual cash flow by 30% or more, a real estate investor purchasing rental properties whose qualifying income cannot support additional conventional loans, a retiree or high-net-worth individual with substantial liquid assets but limited earned income, or a foreign national or ITIN holder without a Social Security number who needs a domestic mortgage.

You are not a good candidate if you have W-2 or consistent 1099 income that supports conventional qualification. Conventional loans produce lower rates, smaller down payments, fewer fees, and stronger consumer protections. There is no benefit to choosing a non-QM product when you qualify conventionally unless a specific program feature like no DTI limit or unlimited financed properties is essential to your situation.

You are also not a good candidate if you cannot produce any verifiable documentation of financial capacity at all. The Ability-to-Repay rule means every legal lender in 2026 must verify something, whether that is bank deposits, liquid assets, or property rental income. A borrower who genuinely has no verifiable assets, no consistent bank deposits, and no rental income to present has no legal path to a mortgage through any regulated lender.

Use our DTI calculator to check whether your income, even using bank statement or asset depletion calculations, produces a DTI that any lender’s program will actually approve before you start the application process.

Documents You Still Need for a No Income Verification Loan

Many borrowers approach alternative documentation loans assuming they genuinely need to produce nothing. That is not accurate, and walking into a lender conversation without the right documents wastes everyone’s time.

For a bank statement loan: 12 to 24 months of business or personal bank statements in PDF format directly from your bank, a business license or CPA letter confirming two or more years of self-employment, and a simple profit and loss statement prepared or reviewed by a CPA.

For a DSCR loan: a property appraisal with a market rent analysis, a lease agreement if the property is currently rented, three months of personal bank statements confirming reserves, and a credit report authorization.

For an asset depletion loan: two to three months of statements for every qualifying asset account, documentation of account ownership, and confirmation that retirement account balances used in the calculation have been discounted appropriately for early withdrawal penalties if applicable.

For any non-QM loan: a government-issued photo ID, a complete loan application, authorization for a hard credit pull, and documentation of the down payment funds source, including a gift letter if any portion comes from family.

Use our loan eligibility checker to see which loan types align with your financial profile before gathering documents for any specific program, so the documentation you prepare matches the actual product you are applying for.

DISCLAIMER BLOCK

This article is for informational purposes only and does not constitute financial or legal advice. Mortgage program availability, rates, credit score requirements, down payment minimums, and income calculation methods change frequently and vary significantly by lender. No income verification mortgage products carry higher rates and stricter requirements than conventional loans. Always consult a licensed mortgage professional before making decisions about any alternative documentation loan product. Verify all program details directly with lenders before submitting any application.

")