Mortgage Debt-to-Income Ratio

A Comprehensive Theory-Based Guide for Borrowers, Lenders, and Financial Professionals

INTRODUCTION

When a person decides to purchase a home, one of the most fundamental financial questions they must face is whether they can truly afford the mortgage they are seeking. Lenders, financial institutions, and housing economists have long recognized that income alone is not sufficient to determine a borrower’s creditworthiness. What matters equally if not more is the relationship between a person’s debt obligations and their income. This relationship is formally measured through a concept known as the debt-to-income ratio, commonly referred to as DTI.

In the context of mortgage lending, the debt-to-income ratio is one of the most important underwriting criteria used by banks, mortgage companies, and government-sponsored enterprises. It provides lenders with a standardized way to evaluate whether a borrower has sufficient financial capacity to take on a new housing debt without becoming financially overwhelmed. For borrowers, understanding DTI is equally critical because it directly influences whether their mortgage application will be approved, what interest rate they will receive, and how much home they can realistically afford.

This article provides a thorough theoretical and practical examination of the mortgage debt-to-income ratio. It explores the origins and definition of the concept, how it is calculated, why it matters, what thresholds lenders use, how it interacts with other financial variables, and what strategies borrowers can use to manage and improve their DTI. The goal is to give readers a deep, well-rounded understanding of this essential financial metric.

1. Understanding the Concept of Debt-to-Income Ratio

1.1 Definition and Theoretical Foundation

At its most fundamental level, the debt-to-income ratio is a percentage that expresses the proportion of a borrower’s gross monthly income that goes toward paying recurring monthly debt obligations. The ratio is calculated by dividing total monthly debt payments by total gross monthly income and then multiplying the result by one hundred to express it as a percentage.

The theoretical foundation of DTI lies in the broader field of credit risk assessment. Financial theory holds that any individual has a finite capacity to service debt. If debt obligations consume too large a share of income, the individual is left with insufficient resources to cover daily living expenses, unexpected financial shocks, savings, and other essential expenditures. This increases the probability of default, which is the event lenders most seek to avoid.

DTI functions as a proxy for financial stress. A high ratio indicates that a borrower is already heavily committed to servicing existing debts, leaving little cushion for an additional mortgage payment. A low ratio, on the other hand, suggests that the borrower has significant financial breathing room and is therefore considered a lower-risk lending prospect.

1.2 The Two Types of DTI in Mortgage Lending

Mortgage lenders typically work with two distinct variations of the debt-to-income ratio, each measuring a different dimension of the borrower’s financial commitments.

Front-End DTI (Housing Ratio)

The front-end DTI, sometimes called the housing ratio or the top ratio, measures the percentage of gross monthly income that would be consumed by housing-related expenses alone. These expenses typically include the proposed monthly mortgage payment (principal and interest), property taxes, homeowner’s insurance, and homeowner association fees if applicable. Private mortgage insurance may also be included when the down payment is less than twenty percent of the home’s purchase price.

This ratio helps lenders assess whether the specific housing cost the borrower is taking on is proportionate to their income, independent of all other debt obligations. Most conventional mortgage guidelines consider a front-end DTI of twenty-eight percent or below to be acceptable, though many lenders are willing to approve loans with front-end ratios up to thirty-one or thirty-three percent depending on the overall strength of the borrower’s financial profile.

Back-End DTI (Total Debt Ratio)

The back-end DTI, also known as the total debt ratio or the bottom ratio, measures the percentage of gross monthly income that is consumed by all recurring monthly debt obligations combined. This includes the proposed housing payment plus all other existing debts such as car loans, student loans, credit card minimum payments, personal loans, child support, alimony, and any other financial obligations that appear on the borrower’s credit report.

The back-end DTI is generally considered the more important and comprehensive of the two ratios because it captures the complete picture of the borrower’s debt burden. Lenders typically apply stricter scrutiny to the back-end DTI when making final credit decisions. The conventional threshold for the back-end ratio is often set at thirty-six to forty-three percent, though government-backed loan programs may allow significantly higher ratios under certain conditions.

| DTI Type | What It Measures | Typical Acceptable Limit |

|---|---|---|

| Front-End DTI | Housing expenses only (mortgage, taxes, insurance) | 28% or below |

| Back-End DTI | All monthly debts including housing | 36% to 43% (conventional) |

2. How the Debt-to-Income Ratio Is Calculated

2.1 Identifying Gross Monthly Income

The income figure used in the DTI calculation is always the borrower’s gross monthly income, which is income before any taxes, deductions, or withholdings are subtracted. Lenders verify this figure through documentation such as recent pay stubs, W-2 forms, tax returns, and bank statements, depending on the nature of the borrower’s employment.

For salaried employees, gross monthly income is straightforward to calculate: it is simply the annual salary divided by twelve. For hourly workers, the calculation typically involves multiplying the hourly wage by the average number of hours worked per week and then annualizing that figure. For self-employed individuals, freelancers, or those with variable income, lenders generally calculate average monthly income based on the most recent two years of federal tax returns, often applying depreciation add-backs and other adjustments as permitted under standard underwriting guidelines.

Non-traditional income sources such as rental income, investment dividends, Social Security payments, pension distributions, and alimony received may also be included in the gross income calculation, provided the borrower can document that these income streams are stable and likely to continue for at least three years.

2.2 Identifying Monthly Debt Obligations

The debt side of the DTI equation includes all minimum monthly payments on recurring obligations that appear on the borrower’s credit report. This includes credit card minimum payments, auto loan payments, student loan payments, personal loan payments, and any existing mortgage or home equity loan payments on other properties. It also includes legal obligations such as court-ordered child support and alimony.

It is important to note that lenders use minimum required payments rather than the amounts the borrower actually pays. For example, if a borrower has a credit card with a balance of five thousand dollars and a minimum payment of one hundred dollars but typically pays three hundred dollars each month, the lender will use one hundred dollars in the DTI calculation. This approach standardizes comparisons across different borrowers with different payment behaviors.

Debts that are not considered include utility bills, groceries, health insurance premiums, cell phone bills, and other monthly expenses that do not appear on a credit report. While these costs certainly affect a household’s practical budget, they are not factored into the formal DTI calculation used for mortgage underwriting purposes.

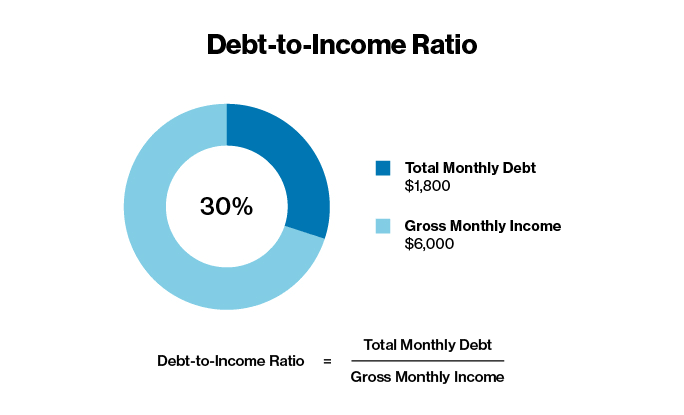

2.3 The Calculation Formula

The formula for calculating back-end DTI is as follows: divide the total of all minimum monthly debt payments (including the proposed new mortgage payment) by the gross monthly income, and multiply by one hundred.

As a practical illustration, consider a borrower who earns a gross monthly salary of seven thousand dollars. This borrower has an existing car loan payment of four hundred dollars, a student loan payment of two hundred and fifty dollars, and credit card minimum payments totaling one hundred and fifty dollars. They are applying for a mortgage with a proposed monthly payment of one thousand eight hundred dollars including taxes and insurance. Their total monthly debt payments are two thousand six hundred dollars. Dividing two thousand six hundred by seven thousand gives approximately 0.371, which means their back-end DTI is approximately thirty-seven point one percent. Under conventional guidelines, this borrower would generally be considered acceptable, though they are approaching the upper range of the standard threshold.

| Income Item | Monthly Amount |

|---|---|

| Gross Monthly Salary | $7,000 |

| Proposed Mortgage Payment (PITI) | $1,800 |

| Car Loan Payment | $400 |

| Student Loan Payment | $250 |

| Credit Card Minimums | $150 |

| Total Monthly Debt | $2,600 |

| Back-End DTI (2,600 / 7,000) | 37.1% |

3. DTI Thresholds Across Different Loan Programs

3.1 Conventional Loans

Conventional mortgage loans are those that are not backed or insured by any government agency. They are originated by private lenders and typically sold to the government-sponsored enterprises Fannie Mae and Freddie Mac, which purchase mortgage loans from lenders and package them into mortgage-backed securities sold to investors. Because conventional loans carry no government guarantee, lenders and the enterprises that purchase them apply relatively strict underwriting standards.

Under conventional loan guidelines, the generally accepted maximum back-end DTI is forty-three to forty-five percent. Fannie Mae’s automated underwriting system, Desktop Underwriter, may approve borrowers with DTI ratios as high as fifty percent if the loan profile is otherwise very strong — for example, if the borrower has a high credit score, substantial assets in reserve, and a significant down payment. However, borrowers approaching the upper limits of these thresholds will typically face stricter scrutiny and may receive less favorable loan terms.

3.2 FHA Loans

Federal Housing Administration loans are government-backed mortgage products designed to make homeownership accessible to borrowers who may not qualify for conventional financing due to lower credit scores, limited down payment funds, or higher debt levels. The FHA insures these loans against default, which reduces the lender’s risk and allows for more flexible qualifying criteria.

FHA guidelines typically allow a maximum front-end DTI of thirty-one percent and a maximum back-end DTI of forty-three percent. However, borrowers with strong compensating factors — such as a credit score above five hundred eighty, substantial cash reserves, or a history of paying large housing costs successfully may be approved with back-end DTI ratios as high as fifty or even fifty-seven percent through the FHA’s automated underwriting system, known as TOTAL Scorecard.

3.3 VA Loans

VA loans are mortgage products available to eligible military veterans, active-duty service members, and surviving spouses, backed by the United States Department of Veterans Affairs. VA loans are known for their favorable terms, including no down payment requirement and no private mortgage insurance, making them among the most powerful home financing tools available.

The VA does not set a strict maximum DTI, but lenders are generally encouraged to apply a guideline of forty-one percent for the back-end ratio. Borrowers who exceed this threshold are subject to additional scrutiny, and lenders must document that the borrower has sufficient residual income the amount of money left over after all monthly obligations are paid l to cover living expenses. The residual income requirement is one of the most distinctive features of VA loan underwriting and provides an additional safety net beyond the DTI metric.

3.4 USDA Loans

USDA Rural Development loans are government-backed mortgages available for properties located in eligible rural and suburban areas, designed to promote homeownership in less densely populated regions. Like FHA and VA loans, USDA loans carry a government guarantee that allows lenders to extend credit to borrowers who might not meet conventional standards.

USDA guidelines typically use a front-end DTI limit of twenty-nine percent and a back-end DTI limit of forty-one percent. As with other government programs, these limits may be exceeded with documented compensating factors, and the USDA’s automated underwriting system may approve higher ratios for otherwise strong loan files.

| Loan Program | Max Front-End DTI | Max Back-End DTI | Notes |

|---|---|---|---|

| Conventional (Fannie/Freddie) | 28% (guideline) | 43–45% (up to 50% with AUS) | Stricter credit standards overall |

| FHA | 31% | 43% (up to 57% with AUS) | Flexible for lower credit scores |

| VA | No strict limit | 41% (guideline) | Residual income requirement applies |

| USDA | 29% | 41% | Rural/suburban properties only |

4. The Theoretical Significance of DTI in Credit Risk

4.1 DTI as a Predictor of Default

The reason lenders place such emphasis on the debt-to-income ratio is rooted in empirical research on mortgage default behavior. Decades of data collected by lenders, housing agencies, and academic researchers consistently show that the probability of mortgage default increases significantly as the DTI ratio rises. When a borrower’s debt obligations absorb a large fraction of their income, any disruption to that income such as a job loss, medical emergency, or unexpected major expense can quickly render them unable to make their monthly payments.

Mortgage delinquency and foreclosure data from historical crises, including the 2008 financial crisis in the United States, demonstrated clearly that loans originated with high DTI ratios performed substantially worse than loans originated within standard thresholds. This evidence reinforced the importance of DTI as a core underwriting criterion and led to stricter regulatory requirements around ability-to-repay standards.

4.2 DTI in the Context of the Ability-to-Repay Rule

In the aftermath of the 2008 mortgage crisis, the United States federal government enacted the Dodd-Frank Wall Street Reform and Consumer Protection Act, which introduced new requirements for mortgage lenders. Among the most significant provisions was the Ability-to-Repay rule, which requires lenders to make a good-faith determination that a borrower has the financial capacity to repay the mortgage loan before originating it.

The Qualified Mortgage standard, established as part of this regulatory framework, provides lenders with a legal safe harbor protection against lawsuits from borrowers who later default if the loan meets certain criteria. One of the key criteria for Qualified Mortgage status is that the borrower’s back-end DTI must not exceed forty-three percent, though there are exceptions for loans eligible for purchase by government-sponsored enterprises. This regulatory codification of the DTI threshold reflects the government’s recognition of the ratio’s importance as a consumer protection mechanism.

4.3 Limitations of DTI as a Standalone Metric

While the debt-to-income ratio is a powerful and widely used tool, financial theorists and practitioners recognize that it has important limitations as a standalone measure of creditworthiness. DTI measures the proportion of income committed to debt but does not capture the absolute size of the income or the borrower’s wealth. A borrower earning twenty thousand dollars per month with a forty percent DTI has eight thousand dollars in remaining monthly cash flow, while a borrower earning four thousand dollars per month with a forty percent DTI has only two thousand four hundred dollars remaining, a very different financial reality despite identical DTI ratios.

Furthermore, DTI does not account for the stability or sustainability of the income. A borrower with a thirty-five percent DTI based on variable commission income faces fundamentally different risk than a borrower with the same DTI based on stable government employment. For this reason, lenders never evaluate DTI in isolation but always assess it alongside credit scores, employment history, cash reserves, loan-to-value ratios, and overall asset profiles.

5. How DTI Interacts with Other Key Mortgage Variables

5.1 DTI and Credit Score

The relationship between DTI and credit score is one of the most important interactions in mortgage underwriting. Credit scores measure a borrower’s historical behavior in managing credit obligations, while DTI measures the current capacity to service new debt. Together, they provide a more complete picture of risk than either metric alone.

In practice, a borrower with an excellent credit score may be approved for a mortgage at a higher DTI than would normally be permitted, because the strong credit history suggests a demonstrated commitment to making payments on time even under financial pressure. Conversely, a borrower with a marginal credit score who also has a high DTI faces compounded risk factors that make approval much more difficult. Lenders often think of these metrics as a sliding scale: strength in one area can compensate for weakness in another, but only up to a point.

5.2 DTI and Loan-to-Value Ratio

The loan-to-value ratio measures the size of the mortgage loan relative to the appraised value of the property. A borrower who makes a large down payment has a lower loan-to-value ratio, which means the lender has a larger equity cushion in the event of default and subsequent foreclosure. This reduces the lender’s potential loss and therefore reduces overall risk.

When a borrower has a high DTI but a low loan-to-value ratio meaning they are making a substantial down payment lenders may view the overall risk profile as acceptable because the equity in the property provides significant protection. The reverse situation, however, is particularly concerning: a borrower with both a high DTI and a high loan-to-value ratio represents a compounding of risk factors that most lenders will not accommodate without extraordinary compensating circumstances.

5.3 DTI and Cash Reserves

Cash reserves refer to assets that the borrower has available beyond the funds needed for the down payment and closing costs. Reserves provide a financial buffer that can allow the borrower to continue making mortgage payments for several months even if their primary income is interrupted. Lenders typically measure reserves in terms of how many months of total mortgage payments the borrower could cover from their liquid assets.

For borrowers with elevated DTI ratios, demonstrating substantial cash reserves is one of the most effective compensating factors. A borrower whose DTI is somewhat above the standard guideline but who has twelve or more months of mortgage payments in liquid reserves is viewed very differently from a borrower with the same DTI and minimal savings. Reserves signal financial prudence and provide a concrete safety net against default.

6. Strategies for Managing and Improving Your DTI

6.1 Reducing Existing Debt

The most direct way to improve a DTI ratio is to reduce the monthly debt obligations that are being compared to income. Paying down existing debts particularly those with high minimum monthly payments directly lowers the numerator of the DTI calculation. Borrowers who are preparing to apply for a mortgage should prioritize paying off smaller debts in full, starting with those that carry the highest minimum monthly payments relative to their outstanding balances, since eliminating these accounts has the greatest immediate impact on DTI.

It is worth noting that paying down credit card balances below fifty percent of the credit limit has the additional benefit of improving the borrower’s credit utilization ratio, which is a significant component of credit score calculation. This dual benefit of lower DTI and higher credit score makes credit card paydown a particularly high-value strategy for mortgage preparation.

6.2 Increasing Income

Increasing gross monthly income increases the denominator of the DTI calculation, which reduces the ratio even if debt levels remain unchanged. Borrowers who are anticipating a mortgage application may explore opportunities to increase income through salary negotiation, promotion, taking on additional employment, developing freelance or consulting income, or converting informal income sources into documented ones.

Lenders require that income used in the DTI calculation be stable and likely to continue. A recent raise or new job with higher salary may qualify immediately if the borrower provides an offer letter and documentation. Self-employment or freelance income, however, typically requires a two-year history before lenders will consider it, which means prospective borrowers relying on non-traditional income sources should plan their mortgage application timeline accordingly.

6.3 Choosing a Less Expensive Property

The proposed mortgage payment is itself a component of the DTI calculation. Choosing a less expensive property and therefore requiring a smaller mortgage directly reduces the proposed housing payment, which lowers both the front-end and back-end DTI simultaneously. While this may require accepting a home that is smaller or located in a different area than initially desired, it is a practical and effective way to bring DTI within acceptable limits.

Borrowers should work backward from their DTI target to determine the maximum mortgage payment they can qualify for and then calculate the maximum purchase price that payment supports at current interest rates. This exercise provides a realistic budget framework before beginning the home search process.

6.4 Making a Larger Down Payment

A larger down payment reduces the loan amount, which in turn reduces the monthly mortgage payment and therefore lowers the proposed DTI. Additionally, if the larger down payment brings the loan-to-value ratio below eighty percent, the borrower may be able to eliminate private mortgage insurance, which further reduces the monthly housing payment included in the front-end DTI calculation.

The challenge with this strategy is that accumulating a larger down payment takes time and may require delaying the home purchase. However, the financial benefits of a lower DTI, better loan terms, and potentially a lower interest rate can outweigh the cost of waiting, particularly in markets where home prices are rising rapidly.

6.5 Avoiding New Debt Before Applying

One of the most important pieces of advice for prospective mortgage borrowers is to avoid taking on any new debt in the months leading up to a mortgage application. Every new credit obligation whether it is a car loan, a furniture purchase on installment, or even a new credit card adds to the monthly debt obligations that lenders will count in the DTI calculation.

Lenders pull credit reports and verify debt information at multiple points during the mortgage process, including immediately before closing. A borrower who acquires new debt after receiving a mortgage pre-approval but before the loan closes may find that their DTI has risen above the qualifying threshold, potentially causing the loan to be denied at the final stage. Maintaining financial stability and avoiding new obligations throughout the entire mortgage process is therefore a critical strategic priority.

7. DTI in the Broader Housing Market Context

7.1 DTI and Housing Affordability

The aggregate debt-to-income ratios of mortgage borrowers across an economy serve as a meaningful indicator of housing affordability at the market level. When average DTI ratios among new mortgage borrowers are rising, it suggests that home prices are increasing faster than incomes, forcing buyers to commit larger shares of their earnings to housing costs. This dynamic can signal an overheated housing market and increases systemic risk in the financial system.

Housing economists and policy analysts track DTI trends alongside other affordability metrics such as the price-to-income ratio, the price-to-rent ratio, and monthly mortgage payment affordability indices. A sustained period of rising borrower DTI ratios, particularly when combined with declining lending standards and increased use of flexible loan products, has historically preceded periods of market correction and elevated default activity.

7.2 Regulatory and Policy Implications

The importance of DTI in mortgage underwriting has led governments and financial regulators around the world to incorporate it into housing finance policy. In addition to the United States Qualified Mortgage framework mentioned earlier, many European countries have adopted formal DTI limits as part of macroprudential financial regulation. Ireland, for example, has implemented binding DTI caps on new mortgage lending to prevent excessive household leverage and reduce systemic risk in its banking sector.

These regulatory approaches reflect a broad consensus among policymakers and financial stability experts that unconstrained growth in household mortgage debt relative to income poses significant risks not only to individual borrowers but to the entire economy. The 2008 global financial crisis demonstrated in the most painful terms possible what can happen when mortgage lending is extended without adequate attention to borrowers’ debt service capacity.

Conclusion

The mortgage debt-to-income ratio is far more than a technical underwriting metric. It represents a fundamental principle of sound credit management: that debt obligations must be proportionate to the income available to service them. For individual borrowers, understanding DTI provides clarity about what they can realistically afford, how to prepare their finances before applying for a mortgage, and what steps to take if their current ratio is too high to qualify for the loan they desire.

For lenders and financial institutions, DTI is an indispensable tool for managing credit risk, ensuring regulatory compliance, and protecting both their capital and the long-term financial well-being of their borrowers. For policymakers, aggregate DTI trends offer important signals about the health of the housing market and the appropriateness of existing lending standards.

The two components of DTI front-end and back-end ratios capture different dimensions of housing affordability and overall debt burden. The thresholds applied by different loan programs reflect both empirical research on default risk and policy judgments about how to balance access to homeownership with the need for responsible lending. And the interaction of DTI with other variables such as credit score, loan-to-value ratio, and cash reserves illustrates why mortgage underwriting is a holistic process rather than a simple checklist.

Whether you are a first-time homebuyer trying to understand what lenders are looking for, a financial professional advising clients on mortgage readiness, or a policy analyst studying housing market dynamics, the debt-to-income ratio stands as one of the most important numbers in the entire mortgage lending ecosystem. Mastering its definition, calculation, implications, and management strategies equips you with essential knowledge for navigating the complex and consequential world of home financing.