Best Mortgage Lenders for Self Employed Borrowers 2026

Getting a mortgage as a self-employed borrower in 2026 is not as difficult as most people assume. But it is genuinely different, and walking into the wrong lender with the wrong documentation will cost you time, damage your credit score from unnecessary hard pulls, and leave you convinced the system is designed against you. It is not. The system is just designed for W-2 employees, and the lenders that serve self-employed borrowers well are a specific subset that most buyers never find because they start their search in the wrong place.

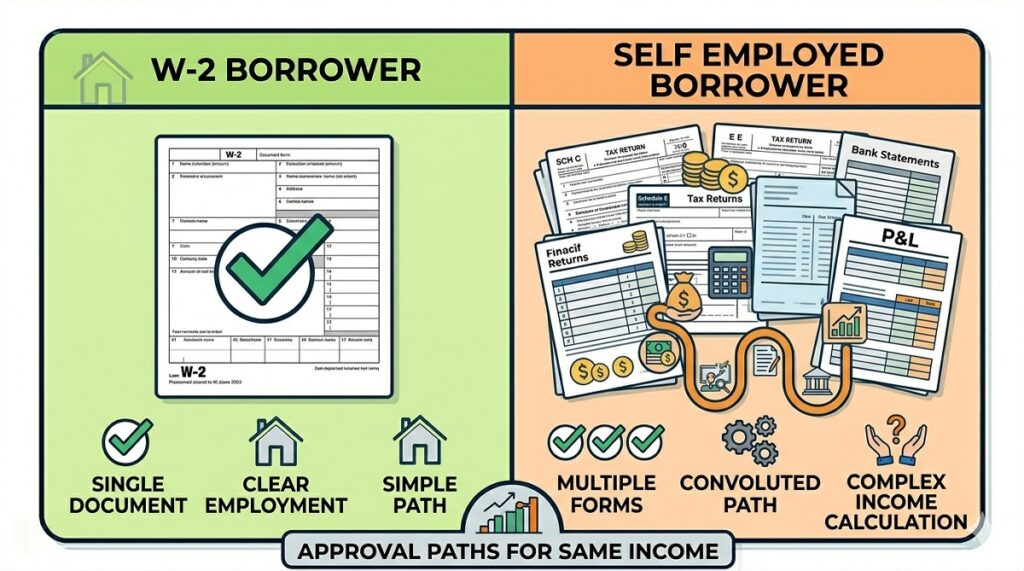

The best mortgage lenders for self employed borrowers are the ones who understand a fundamental truth about your financial situation: your tax return is not your income. Your actual income is what flows through your business and bank accounts. The lenders who get that distinction are the ones who can close your loan. The ones who do not get it will string you along for six weeks, ask for document after document, and ultimately decline you based on your Schedule C taxable income rather than your real cash flow.

I have reviewed the documentation requirements, income calculation methods, specialty loan programs, and lender track records for self-employed borrowers specifically. Here is exactly who to call and what to prepare before you do.

Why Self Employed Borrowers Get Declined and How to Fix It

Before lender recommendations, you need to understand the root cause of the problem. Most self-employed borrowers who get declined are not declined because they cannot afford the loan. They are declined because of how lenders calculate qualifying income under standard guidelines.

Most lenders require at least two years of self-employment, though some accept one year with a related work history or education. Lenders examine income history, cash flow, and business stability more carefully because self-employed earnings can fluctuate. FHA.com

Here is the core problem. You earned $150,000 in gross revenue last year running your business. You legitimately deducted $60,000 in business expenses, including vehicle mileage, home office, equipment, and professional services. Your taxable income on your Schedule C shows $90,000. The lender then adds back certain deductions like depreciation and looks at a two-year average of your Schedule C income. If year one was $80,000 and year two was $90,000, your qualifying income might be $85,000 per year, or $7,083 per month.

On a $400,000 mortgage at 6.5%, your monthly payment is approximately $2,528. Your DTI (debt-to-income ratio, meaning your total monthly debts divided by your gross monthly income) using qualifying income is roughly 35.7%, which should pass lender requirements. But if you also have a car payment of $500 and minimum credit card payments of $300, your back-end DTI jumps to 47%, which pushes you past the 45% ceiling many conventional lenders enforce.

That is how a borrower earning $150,000 in actual cash flow gets declined for a loan they can easily afford. The tax optimization that saved you $15,000 in taxes cost you the mortgage approval.

Most self-employed mortgage lenders require two years of income documentation, but qualifying income is often reduced due to deductions, depreciation, and business expenses. As a result, many self-employed borrowers struggle to qualify under conventional mortgage rules even with strong cash flow. Yelp

The fix depends on your situation. If you are applying 12 or more months from now, consider working with your CPA to show higher taxable income on this year’s return by claiming fewer deductions temporarily. The tax cost of showing $30,000 more income at a 25% effective tax rate is $7,500. The benefit is qualifying for a $400,000 home instead of a $280,000 home. Most buyers who run this calculation decide the trade-off is worth it for one year.

If you need to buy now, the fix is finding a lender who offers bank statement loans or other non-QM alternatives that evaluate your actual deposits rather than your taxable income.

Bank Statement Loans Explained: How Income Gets Calculated

Bank statement loans are the primary tool that solves the self-employed mortgage problem, and understanding exactly how they work prevents surprises during underwriting.

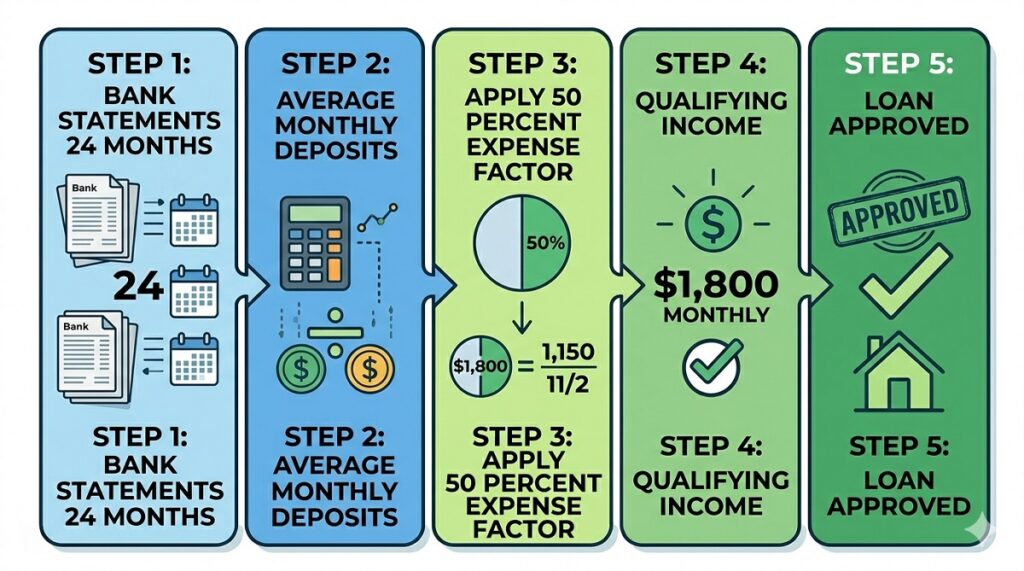

Bank statement loans allow self-employed borrowers to qualify based on cash flow rather than tax returns. Lenders evaluate income by reviewing 12 to 24 months of personal and business bank statements to calculate an average monthly income. FHA.com

The calculation works like this. The lender takes your total deposits across 12 or 24 months of business bank statements and divides by the number of months to get your average monthly gross deposits. They then apply an expense factor, typically 40% to 50%, to account for the business costs that are presumably embedded in those deposits. The resulting number becomes your qualifying monthly income.

Conventional loans use taxable income after write-offs. Non-QM bank statement loans use gross deposits before write-offs. This approach can increase qualifying income by 30% to 50% compared to what your tax return shows. AZ Big Media

A practical example: a freelance graphic designer in Chicago deposits an average of $12,000 per month across 24 months of business bank statements. The lender applies a 50% expense factor, arriving at $6,000 in qualifying monthly income. On a conventional loan using her Schedule C, her qualifying income was only $4,200 per month after deductions. The bank statement approach gives her 43% more qualifying income, which on a 30-year loan at 6.5% translates to roughly $75,000 in additional purchase power.

Credit score minimums for bank statement loans range from 620 to 700 depending on the lender, down payments span 10% to 25%, and statement requirements vary between 12 and 24 months depending on program. Rocket Mortgage

The honest trade-off: bank statement loan rates run approximately 0.25% to 0.50% higher than conventional loan rates, and non-QM rates broadly range from 0.75% to 2.00% above conventional rates depending on credit profile and lender. On a $350,000 loan, a 0.75% rate premium equals roughly $161 per month and over $57,000 across a 30-year term. Many self-employed borrowers accept this premium knowing they can refinance to a conventional loan once two full years of higher taxable income are documented. Alpine MortgageAZ Big Media

Use our mortgage rate comparison tool to see how bank statement loan rates compare to current conventional rates before committing to any specific program.

Other Loan Options Beyond Bank Statements

Bank statement loans are not the only path. Depending on your income structure and assets, one of these alternatives may serve you better.

Profit and Loss Statement Loans

P&L loans work best for self-employed borrowers in service businesses with low overhead who maintain organized CPA-prepared financial statements. The lender uses your net profit as shown on a CPA-certified P&L statement rather than bank deposits, which works well when your net profit is a clean and accurate representation of what you earn. If your business has genuine low overhead costs and your P&L shows strong net income, this path may produce a higher qualifying income than bank statements with a 50% expense factor applied. U.S. News & World Report

DSCR Loans for Real Estate Investors

DSCR stands for debt service coverage ratio, and this loan type is specifically designed for real estate investors who own rental properties. DSCR loans qualify based on property cash flow rather than borrower income. If rental income covers the mortgage payment, approval is possible regardless of the borrower’s personal income documentation. A self-employed buyer purchasing an investment property where the projected rent covers the mortgage payment can qualify for a DSCR loan without submitting a single personal tax return. U.S. News & World Report

Asset Depletion Loans

Asset depletion loans are designed for borrowers with substantial liquid assets, savings, investments, and retirement accounts, but limited or no documented income. Common for retirees and high-net-worth borrowers, asset depletion loans calculate qualifying income by dividing the total liquid assets by the remaining loan term in months. A self-employed business owner who sold a business and is holding $1.5 million in liquid assets but has low reported income for two years can qualify through this method. $1.5 million divided by 360 months equals $4,167 per month in qualifying income without any employment documentation. U.S. News & World Report

1099-Only Loans

Several lenders accept 12 to 24 months of 1099 forms as income documentation for contract workers, consultants, and gig economy workers who receive 1099s rather than W-2s. This sits between full bank statement underwriting and conventional income documentation, and often carries a smaller rate premium than a full bank statement loan.

Best Mortgage Lenders for Self Employed Borrowers 2026 Ranked

Every lender below has been selected based on their actual non-QM product availability, credit score flexibility, income documentation options, and track record with complex self-employed files.

CrossCountry Mortgage: Best Overall for Self Employed Borrowers

CrossCountry Mortgage is the lender I recommend most consistently to self-employed buyers who cannot qualify conventionally, and for good reason. CrossCountry’s FastTrack review speeds up the underwriting process, allowing approved borrowers to close in as few as 10 days. For a self-employed buyer in a competitive market who needs a credible preapproval fast, that timeline matters enormously. FHA.com

CrossCountry accepts credit scores as low as 500 for certain non-traditional mortgages, significantly below the 620 minimum that most non-QM lenders enforce. Combine that with their bank statement loans, DSCR products, and 1099 programs, and CrossCountry covers the widest range of self-employed borrower profiles under one roof. FHA.com

Their loan officers tend to have genuine experience with complex income structures rather than reading from a script. A contractor in Dallas whose income spans 1099 consulting fees, LLC distributions, and rental income from two properties is a file CrossCountry handles regularly. That experience matters when you hit the inevitable underwriting questions.

Who CrossCountry works for: Self-employed buyers with credit scores from 500 upward, borrowers with multiple income streams, and anyone who needs to close quickly. Who it does NOT work for: Prime borrowers with clean W-2 equivalent income who could get a sharper conventional rate elsewhere.

Guild Mortgage: Best for Widest Non-QM Product Selection

Guild Mortgage offers a robust variety of non-QM mortgages including bank statement loans, DSCR loans, and interest-only options, which can enable self-employed borrowers to allocate more funds to other expenses early in their mortgage. FHA.com

Guild combines local branch support across dozens of states with a deep non-QM menu, making it one of the few lenders where you can walk into a branch with a complex self-employed file and speak face-to-face with a loan officer who genuinely understands what options exist for your situation. JVM Lending

Guild also uses alternative credit check methods for government-backed loans, which helps self-employed borrowers with thin credit files but strong business cash flow. If your credit history is limited because you have been building a business rather than collecting credit cards, Guild’s approach gives you a real evaluation rather than an automated decline.

Who Guild works for: Self-employed borrowers who want the widest loan menu, local human support, and the flexibility to use multiple non-QM products depending on which produces the strongest qualifying income. Who it does NOT work for: Borrowers who want a fully online, no-branch experience.

First National Bank of America: Best for High DTI Self Employed Buyers

Most lenders will not approve borrowers with a DTI higher than 45% to 50%. First National Bank of America accepts DTIs up to 60%, making it an excellent option for small business owners who are often highly leveraged. FHA.com

For self-employed buyers who carry business debt in addition to personal debt, the 60% DTI ceiling is a genuine lifeline. A business owner with $3,200 in monthly personal debts and a gross monthly income of $8,000 sits at a 40% DTI on personal obligations alone. Add a $1,800 mortgage payment and the total DTI hits 62.5%, which disqualifies them at virtually every mainstream lender. First National Bank of America has a path where most others have a wall.

FNBA’s Alt-A Premier non-QM mortgage makes up to $3 million available to borrowers with debt-to-income ratios of 60%, requires no cash reserves, and allows gift funds toward the down payment. FHA.com

Who FNBA works for: Self-employed buyers with high existing debt relative to income, business owners with complex balance sheets, and borrowers needing larger loan amounts who cannot qualify at conventional DTI caps. Who it does NOT work for: Buyers who need the most competitive possible rate on a straightforward file.

Angel Oak Mortgage Solutions: Best Non-QM Specialist

Angel Oak Mortgage Solutions is one of the largest non-QM lenders nationally and has built its entire operation around borrowers who do not fit conventional boxes. Where big retail lenders treat non-QM as a side product, Angel Oak treats it as the core business. That institutional focus produces loan officers, underwriters, and processes specifically designed for self-employed borrowers rather than retrofitted from W-2 workflows. HUD

Angel Oak offers bank statement loans on 12 or 24 months of statements, asset depletion loans, 1099-only loans, and DSCR products for investors. Their underwriters are accustomed to seeing complex business structures and are less likely to ask for redundant documentation or miss standard alternative income documentation.

Who Angel Oak works for: Self-employed buyers who have had files declined at mainstream lenders and need a specialist who handles nothing but non-QM. Who it does NOT work for: First-time buyers who want hand-holding through a simple conventional purchase process.

Carrington Mortgage Services: Best for Credit Challenged Self Employed Buyers

Carrington specializes in self-employed mortgage borrowers who fall outside traditional credit and income standards. They offer bank statement loans, 1099 programs, and flexible underwriting for borrowers with recent credit challenges. Carrington is often used when other lenders decline a file due to credit score or documentation concerns. JVM Lending

If your self-employment journey included a rough patch, a late payment, or a period of reduced income that dinged your credit, Carrington is one of the few non-QM lenders that will look at the full picture rather than disqualifying you on a single data point. Their underwriters are experienced with the income volatility that naturally accompanies building a business, and they evaluate trajectory, not just the worst quarter in your history.

Who Carrington works for: Self-employed buyers with credit scores in the 580 to 640 range, borrowers with past credit events including short sale or medical collection history, and anyone whose file other lenders have bounced. Who it does NOT work for: Prime credit borrowers who could get a better rate at a lower-cost lender.

Rocket Mortgage: Best for Self Employed Buyers Who Qualify Conventionally

If your business is organized, your tax returns are filed, and your income is solid enough to qualify conventionally, Rocket is the fastest way to get a loan for self-employed borrowers. Rocket’s digital platform handles self-employed income documentation through a structured upload process that is faster than most competitors for straightforward files. Propertyprosatlanta

Rocket does require two full years of personal and business tax returns, a year-to-date profit and loss statement, and business bank statements in many cases. But if your two-year average Schedule C income produces adequate qualifying income without needing bank statement workarounds, Rocket’s speed advantage and strong customer service make them worth a quote.

The honest limitation: Rocket does not offer true bank statement loan products or non-QM alternatives. If your taxable income does not support the purchase price you are targeting, Rocket is not your answer regardless of how strong your actual cash flow is.

Who Rocket works for: Self-employed buyers whose documented taxable income supports conventional qualification and who prioritize a fast, clean digital experience. Who it does NOT work for: Anyone who needs alternative income documentation or non-QM underwriting.

Use our free loan eligibility checker to see which loan types and amounts you realistically qualify for based on your income profile before approaching any of these lenders.

Documents Every Self Employed Borrower Should Prepare Before Applying

Walking into a lender conversation unprepared wastes weeks. Here is what you need ready before your first call regardless of which lender you choose.

For a conventional loan using tax returns: two years of personal tax returns including all schedules, two years of business tax returns if you operate as an S-corp or partnership, a year-to-date profit and loss statement prepared or reviewed by your CPA, three months of business bank statements, and two months of personal bank statements.

For a bank statement loan: 12 to 24 months of business bank statements showing consistent deposits, a business license or CPA letter confirming you have been self-employed for at least two years, a simple profit and loss statement, and documentation showing the business account is genuinely yours and not commingled with personal funds.

Keep your business and personal finances strictly separate. Commingling funds, such as paying personal expenses with the business card or depositing business revenue into personal accounts, is a red flag for underwriters and can disqualify deposits from being counted as qualifying income. Propertyprosatlanta

One practical step that many self-employed buyers overlook: get a letter from your CPA on letterhead confirming your self-employment status, the nature of your business, and the number of years you have been operating. This single document answers questions that underwriters ask repeatedly and speeds up the review process at every lender.

Most non-QM programs in 2026 require a minimum 620 to 640 credit score. Check your score before applying and give yourself three to six months to improve it if it is sitting below 660, because the rate difference between a 640 and a 700 score on a non-QM loan can run 0.50% to 1.0%, translating to $100 to $200 per month on a $350,000 loan. U.S. News & World Report

The Write-Off Trap: When Tax Strategy Hurts Your Mortgage

This is the single biggest mistake I see self-employed buyers make, and it costs them years of delayed homeownership.

Many self-employed borrowers struggle to qualify under conventional mortgage rules even with strong cash flow because qualifying income is often reduced due to deductions, depreciation, and business expenses. Yelp

The write-off trap works like this: your business earns $200,000 in gross revenue. Your CPA, doing their job correctly, identifies $110,000 in legitimate business deductions to minimize your tax liability. Your Schedule C shows $90,000 in net income. Your lender calculates a two-year average. Year one showed $75,000 and year two showed $90,000, so qualifying income is $82,500. On a $450,000 home at current rates, this income level produces a DTI above 50% at most lenders. You get declined.

The tax you saved by claiming $110,000 in deductions was approximately $27,500 at a 25% effective rate. The home you could not buy because of those deductions was worth potentially $150,000 to $200,000 more than what your qualifying income supports. The math does not favor aggressive deduction strategies in the year or two before a home purchase.

This does not mean you should stop taking legitimate deductions permanently. It means that if you are planning to buy a home in the next two years, have a specific conversation with your CPA about which deductions are worth claiming now and which could be deferred. Some deductions, like depreciation, can be added back by lenders during income analysis. Others simply reduce your qualifying income with no workaround.

Our guide on private mortgage lenders covers additional non-traditional lending options if conventional and non-QM programs still leave gaps in your qualification picture.

How to Shop Lenders as a Self Employed Borrower

Rate shopping as a self-employed borrower requires a different strategy than shopping as a W-2 employee. Here is why and what to do differently.

First, understand that every hard credit pull from a lender triggers a temporary score reduction. If you apply with five lenders over five weeks, each running a separate hard pull, your score may drop 10 to 15 points during the process. The credit bureaus do treat multiple mortgage inquiries within a 14-day window as a single inquiry, so compress your shopping into two weeks to minimize the score impact.

Second, get Loan Estimates in writing before making any decision. A Loan Estimate is a standardized three-page federal document that every lender must provide within three business days of application. It shows your quoted rate, estimated monthly payment, closing costs, and loan terms in a format that is directly comparable across lenders.

Third, ask specifically about income calculation methodology before any lender pulls your credit. Ask: how do you calculate qualifying income for a self-employed borrower using my business structure? Do you offer bank statement loans? What expense factor do you apply? What is the minimum credit score for your bank statement program? These questions separate lenders who know their products from those reading from a generic script.

Mortgage brokers who specialize in non-QM products can be the best approach for self-employed borrowers because brokers have access to multiple bank statement loan providers and can compare rates and terms across lenders simultaneously. A broker who closes 15 bank statement loans per month knows the current pricing, program changes, and underwriting quirks across multiple lenders. A retail loan officer at a single lender knows only what their employer offers. WalletHub

Use our DTI calculator to calculate your real debt-to-income ratio using both your taxable income and your bank deposit income, so you know which figure to present to each lender and which program your number supports before any conversations begin.

Who Should NOT Use Non-QM Bank Statement Loans

Non-QM loans are not automatically the right answer for every self-employed borrower. Being honest about this saves money.

If your two-year average taxable income supports conventional qualification, a conventional loan almost always produces a lower rate than a bank statement loan. The 0.50% to 1.50% rate premium on non-QM loans is real and compounds over 30 years. On a $400,000 loan, a 1% rate premium equals $222 per month and nearly $80,000 over the loan life. If you qualify conventionally, that premium is an unnecessary cost.

If you have been self-employed for less than two years, most bank statement lenders will not work with you regardless. You must be self-employed for at least two years to qualify for most bank statement loan programs. A borrower who went independent 18 months ago typically needs to wait out the remaining six months or look at a co-borrower with W-2 income to accelerate qualification. LendingTree

If your business bank deposits are inconsistent, with large swings from month to month that a lender’s averaging methodology turns into inadequate qualifying income, a bank statement loan may not solve your problem even though it was designed to. Some businesses with lumpy revenue, project-based income, or seasonal patterns struggle with bank statement qualification just as they struggle with tax return qualification.

Before settling on any path, use our affordability calculator to model how different qualifying income figures change your realistic purchase price, and use our mortgage calculator to see the exact monthly payment at conventional versus non-QM rates so the cost of the rate premium is fully visible before you decide.

DISCLAIMER BLOCK

This article is for informational purposes only and does not constitute financial or legal advice. Mortgage rates, loan program requirements, credit score thresholds, and income calculation methods change frequently and vary by lender. All dollar examples are estimates based on assumed rates and standard program parameters. Always consult a licensed mortgage professional and a qualified tax advisor before making decisions about your home purchase or income documentation strategy.

: Compare Top Options")

: Compare Top Options")