Rocket Mortgage Review 2026 Rates Loans Pros and Cons

Rocket Mortgage is the largest retail mortgage lender in the United States. That is not a marketing claim, it is a documented fact based on loan volume data. Rocket Mortgage ranked first in J.D. Power’s 2025 US Mortgage Origination Satisfaction Survey, has closed over 7.5 million loans since its founding, and in 2025 made two major acquisitions, buying real estate platform Redfin and mortgage servicer Mr. Cooper, that significantly expanded its reach. If you have spent five minutes researching mortgages online, you have already encountered Rocket Mortgage. LendingTree

But being the biggest does not automatically mean being the best fit for your specific situation. This Rocket Mortgage review covers what the lender actually offers in 2026, what the real numbers look like on rates and fees, which programs genuinely help buyers save money, and where Rocket falls short compared to competitors. By the end, you will know whether applying with Rocket Mortgage is the right call for you or whether you should keep looking.

What Is Rocket Mortgage and How Does It Work

Rocket Mortgage is a direct non-bank lender headquartered in Detroit, Michigan, licensed in all 50 states and Washington DC. It operates entirely online with no physical branch locations open to the public. The company was founded in 1985 and introduced the first fully digital mortgage experience in 2015, which fundamentally changed how Americans shop for home loans. WalletHub

The application process runs through Rocket’s website or mobile app. You enter your income, assets, employment history, and Social Security number, and the system verifies much of this automatically by connecting to financial institutions and tax records. In many cases, you can get a preapproval decision within minutes and track your loan status in real time from your phone.

One thing to know upfront: getting a formal preapproval with Rocket Mortgage requires a hard credit inquiry, which temporarily lowers your credit score by a few points. Unlike some lenders that offer soft-pull prequalifications that do not affect your score, Rocket’s preapproval process requires a hard inquiry from the start. If you are rate shopping across multiple lenders, try to do all your hard pulls within a 14-day window so credit bureaus count them as a single inquiry. FastExpert

Rocket Mortgage Loan Products: The Full Menu

Rocket Mortgage covers the major loan types that most American buyers need, though it has notable gaps that matter for specific borrower profiles.

Conventional Loans

For a conforming 30-year fixed-rate mortgage, Rocket requires a minimum credit score of 620, a maximum DTI (debt-to-income ratio, meaning your total monthly debt payments divided by gross monthly income) of 50%, and a two-year history of steady verifiable income. Minimum down payment is 3% on standard conventional loans. Rocket offers fixed-rate terms from 8 to 30 years, including custom terms like 22 or 27 years, which is unusual among lenders and useful if you want your mortgage paid off by a specific date, say retirement. Saferate

FHA Loans

Rocket Mortgage closes more FHA loans than any other lender in the country. FHA loans, backed by the Federal Housing Administration, allow buyers with lower credit scores and limited savings to qualify when conventional loans are out of reach. Rocket accepts FHA borrowers with credit scores as low as 500 with a 10% down payment, and 580 or above with 3.5% down. The 500 floor is meaningful because many lenders quietly set their internal FHA minimum at 580 or even 620, turning away borrowers who technically qualify under official FHA guidelines. Rocket honors that 500 floor. HomeplusazFastExpert

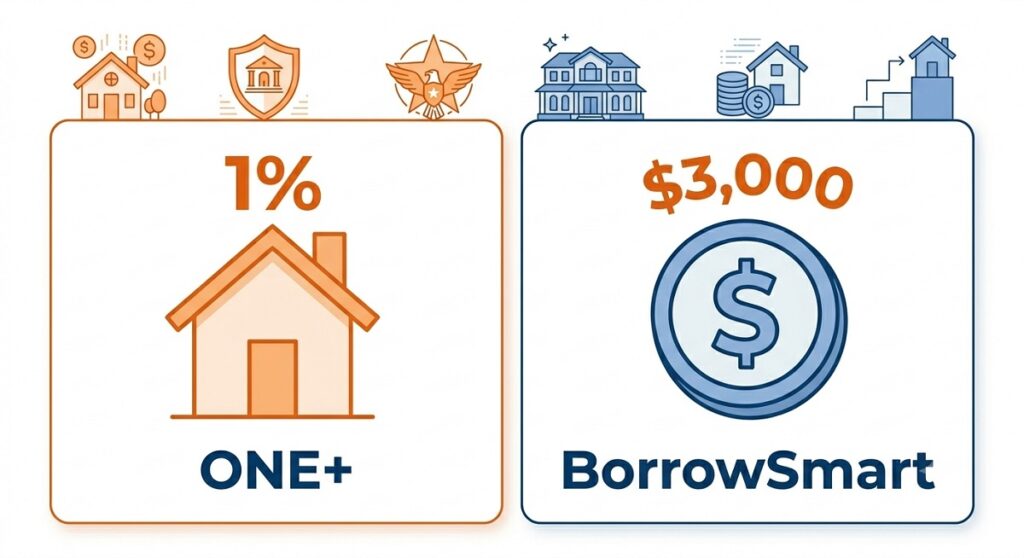

One fee to know: Rocket charges a 1% origination fee on FHA loans, which some competing lenders do not charge. On a $300,000 FHA loan, that equals $3,000 at closing. Factor this into your comparison when getting quotes. FHA.com

VA Loans

Rocket accepts VA loan borrowers with credit scores as low as 580. VA loans require no down payment and no PMI (private mortgage insurance, the monthly fee conventional borrowers pay when they put less than 20% down). On a $350,000 home in 2026, avoiding PMI saves roughly $130 to $200 per month depending on your credit tier. Over five years, that is $7,800 to $12,000 in savings on top of the zero down payment benefit.

Rocket does not offer USDA loans. This is a firm gap. If you are buying in a rural or suburban area that qualifies for USDA financing and you want a zero-down loan without a VA funding fee, you need to go to a different lender. CrossCountry Mortgage, Guild Mortgage, and loanDepot all offer USDA loans where Rocket does not.

Jumbo Loans

Rocket requires a minimum 680 credit score for jumbo loans, which are loans exceeding the 2026 conforming limit of $832,750 for most US counties. Rocket’s jumbo loans go up to $3 million, which covers most buyers in high-cost markets who are not purchasing true luxury properties. If you need above $3 million, you will need a private bank or specialty lender. FHA.com

Home Equity Loans

Rocket’s home equity loan program requires at least a 680 credit score and a minimum loan amount of $45,000. Rocket does not offer HELOCs (home equity lines of credit), only lump-sum home equity loans. If you want a HELOC that allows you to draw money as needed over time rather than receiving a lump sum, Rocket is not the right choice. loanDepot and TD Bank both offer HELOC products where Rocket does not. LendingTree

Bridge Loans

Rocket offers bridge loans that let current homeowners access up to $500,000 in equity from their existing home to cover a down payment and closing costs on a new home, with interest-only payments on a six-month term. The bridge loan gets paid off when your original home sells. This solves one of the most frustrating problems in real estate: needing proceeds from your current home sale to fund the next purchase, but not wanting to sell before you find the right new home. Very few retail lenders offer bridge products at all. FastExpert

Use our free loan eligibility checker to see what loan type and amount you realistically qualify for before requesting any lender’s preapproval.

Rocket Mortgage Specialty Programs: ONE+ BorrowSmart and More

This is where Rocket genuinely separates itself from most national lenders. The specialty programs are real, not just marketing.

ONE+ Mortgage: 1% Down With No PMI

Rocket’s ONE+ program allows qualifying buyers to put just 1% down, with Rocket covering the remaining 2% needed to reach the 3% conventional loan threshold through a grant. ONE+ loans are capped at $350,000 and require a minimum 620 credit score, a DTI under 50%, and household income at or below 80% of the area median income. FHA.com

What makes this genuinely valuable is that Rocket also covers the PMI on ONE+ loans. On a normal 3% down conventional loan, a buyer with a 640 credit score would pay PMI of roughly $100 to $160 per month until they reach 20% equity. ONE+ eliminates that cost entirely. On a $250,000 home, that is $1,200 to $1,920 per year in PMI savings that standard low-down programs do not provide.

The honest limitation is the $350,000 cap. In high-cost metro areas like Austin, Seattle, or much of coastal California, $350,000 does not buy you much. ONE+ is most valuable in markets where median prices fall in the $250,000 to $350,000 range.

BorrowSmart Access: $3,000 Grant for Eligible Metro Buyers

Rocket’s BorrowSmart Access program, based on Freddie Mac’s initiative, provides a $3,000 credit for first-time homebuyers purchasing in eligible counties across ten metro areas: Atlanta, Chicago, Detroit, El Paso, Houston, McAllen, Memphis, Miami, Philadelphia, and St. Louis. To qualify, household income must be at or below 140% of the area median income. Homeplusaz

The $3,000 applies toward your down payment, meaning a buyer in Houston using BorrowSmart Access and putting 3% down on a $250,000 home needs to bring $7,500 of their own funds instead of $10,500. If you are buying in any of these ten cities and meet the income requirements, this is free money. Ask about it specifically when you call Rocket.

Purchase Plus: $7,500 in Six Major Cities

Rocket’s Purchase Plus program provides $7,500 in credits for first-time homebuyers to use toward mortgage costs in six cities: Atlanta, Baltimore, Chicago, Detroit, Memphis, and Philadelphia. This stacks on top of other assistance in some cases. If you are a first-time buyer in Atlanta earning below the income cap, ask a Rocket loan officer whether Purchase Plus and BorrowSmart Access can be combined before assuming you can only access one. The Truth About Mortgage

RentRewards: Credit for On-Time Rent History

Rocket’s RentRewards program provides eligible borrowers with a closing cost credit of up to $5,000 based on their recent rental payment history. This is aimed specifically at renters who have been consistent and responsible with payments but do not have extensive credit history. The credit reduces your cash due at closing, which is often the bigger barrier for first-time buyers after down payment. Saferate

Redfin Partnership Benefit

In July 2025, Rocket Mortgage acquired Redfin. Buyers who work with a Redfin agent and finance through Rocket Mortgage can choose either a rate that is one percentage point lower for the first year of their mortgage, or a closing cost credit worth 0.75% of the loan amount up to $6,000. On a $400,000 loan, the closing cost credit option equals $3,000 off your out-of-pocket costs at closing. If you were already planning to use Redfin for your home search, the financing benefit makes the Rocket Mortgage pairing a natural fit. Arizona Department of Housing

Use our free mortgage calculator to run the numbers on any Rocket Mortgage quote and see your full monthly payment including taxes and insurance before you commit.

Rocket Mortgage Rates and Fees: The Honest Numbers

Rocket Mortgage does post its starting rates publicly on its website, which puts it ahead of loanDepot and CrossCountry on transparency. Rocket Mortgage’s rates are competitive for some loan types but may not be the lowest available. Individual rates vary based on credit score, down payment, loan type, and home price. The Mortgage Reports

On fees, Rocket charges an origination fee of between 0.5% and 1% of the total loan amount, and recommends planning for total closing costs of 2% to 6% of your loan amount. On a $350,000 loan, the origination fee alone runs $1,750 to $3,500, and total closing costs could reach $7,000 to $21,000 before any credits or assistance programs apply. JVM Lending

Rocket does not charge prepayment penalties, and locks your rate free for up to 45 days. A 15-day rate extension costs 0.25 points ($250 per $100,000 borrowed), and borrowers can extend up to twice. The free 45-day lock is useful in a market where closings can drag due to appraisal or title issues. Many lenders charge for locks beyond 30 days. FHA.com

The practical reality is that Rocket’s rates are mid-pack for prime borrowers. If you have a 760 credit score and a 20% down payment, a mortgage broker working through United Wholesale Mortgage or a local credit union can likely beat Rocket’s rate. Where Rocket’s rates become more competitive is with lower credit scores, specialty programs like ONE+, and borrowers who value the speed and reliability of the process over extracting the absolute lowest possible rate.

Rocket Mortgage Customer Reviews: The Real Picture

Rocket Mortgage holds a 4.3 out of 5 rating on ConsumerAffairs, with many reviewers praising the lender for its smooth and efficient application process, strong communication, professionalism, and convenience. JVM Lending

The CFPB received 647 mortgage-related complaints about Rocket Mortgage in 2025. The company gave a timely response to 645 of those, with 629 closed with explanation and 11 closed with monetary relief. That complaint volume relative to Rocket’s total loan count of several hundred thousand originations annually represents a very low complaint rate. The CFPB data suggests Rocket’s customer service machinery actually functions when problems arise. LendingTree

Positive reviews consistently mention fast closings, responsive loan officers reachable in the evenings and on weekends, and a digital process that is genuinely smooth for straightforward loan files. I have seen buyers close FHA loans in 22 days through Rocket, which in a competitive market can be the difference between winning and losing an offer.

Negative reviews cluster around two recurring issues. First, some borrowers report having to submit the same documents multiple times because different team members handle different stages of the loan process. Second, several reviewers on Bankrate describe the company as pushy, with aggressive follow-up marketing in some cases. FastExpertHUD

The servicing side of Rocket, meaning what happens after your loan closes and you start making payments, actually scores better than the origination side. Rocket Mortgage received the highest score of 685 out of 1,000 points in J.D. Power’s 2025 US Mortgage Servicer Satisfaction Study, well above the industry average of 596. That matters because your relationship with a mortgage lender does not end at closing. You will be making payments for 15 to 30 years. LendingTree

Pending Legal Matters You Should Know About

Any honest Rocket Mortgage review in 2026 has to address these directly.

On January 26, 2026, a group of homebuyers filed a class action lawsuit against Rocket Mortgage and its parent and sister companies. The plaintiffs allege that agents within the Rocket Homes network steered buyers toward Rocket Mortgage for financing in exchange for client leads. This mirrors a December 2024 CFPB lawsuit that was dismissed in early 2025 under new CFPB leadership. Arizona Department of Housing

A separate Department of Justice lawsuit filed in October 2024 alleges appraisal discrimination on the basis of race, and also claims Rocket illegally retaliated against the homeowner who made the original discrimination complaint by canceling her refinance application. As of September 2025, a district court denied Rocket’s motion to dismiss that lawsuit, meaning it is actively proceeding. Arizona Department of Housing

These cases are pending and have not resulted in findings against Rocket Mortgage. But they are publicly documented, and any buyer doing due diligence should know they exist.

Rocket Mortgage vs Competitors

Against loanDepot: Rocket posts rates online, loanDepot does not. Rocket has a better app and faster closing timeline. loanDepot counters with a Lifetime Guarantee on refinances and a wider specialty loan menu including USDA and FHA 203k renovation loans. For a buyer planning to refinance within three years, loanDepot’s fee waiver may be more valuable than Rocket’s closing speed. For a buyer who needs to close fast in a competitive market, Rocket wins.

Against Fairway Independent Mortgage: Fairway has local loan officers who know state and county assistance programs personally. Rocket has no branch presence and less institutional knowledge of local DPA programs. For buyers using state programs like TDHCA in Texas or Georgia Dream, a Fairway branch officer may provide better guidance. For straightforward buyers who know what loan they want, Rocket’s speed and 24/7 digital access are advantages.

Against a local credit union: A credit union will almost always beat Rocket’s rate for prime borrowers by 0.125% to 0.25%. But credit unions typically take 40 to 60 days to close, do not have 24/7 support, and often cannot match Rocket’s specialty programs for lower-income buyers. The trade-off is entirely about how much rate savings matters versus speed and program access.

Who Should Use Rocket Mortgage in 2026

Rocket Mortgage makes the most sense for a specific kind of buyer.

First-time buyers with limited savings who qualify for ONE+ can get into a home with 1% down and no PMI, which is a genuinely strong combination that few lenders can match.

Buyers in competitive markets who need to close in 22 days or less to win an offer benefit from Rocket’s documented speed advantage. In a situation where three buyers are submitting offers and one has a Rocket approval letter promising 22-day close, that matters to the seller.

FHA buyers with credit scores between 500 and 580 have real options with Rocket where many other lenders would turn them away at the door.

Buyers using Redfin for their home search should get a Rocket quote specifically to see whether the Redfin partnership discount, either the 1% rate reduction in year one or the closing cost credit, tips the math in their favor.

Check our guide on the fastest mortgage lenders to compare Rocket’s 22-day average against other lenders who market speed as a strength, and use our mortgage rate comparison tool to benchmark any Rocket quote against current market rates before you decide.

Who Should NOT Use Rocket Mortgage

Prime borrowers with 740-plus credit scores and 20% down payments will almost always find a lower rate at a wholesale broker, a local credit union, or a lender with a more aggressive pricing model. Rocket’s mid-pack pricing means high-credit borrowers pay a convenience premium that adds up over 30 years.

Buyers who need USDA loans for rural or suburban properties have no path through Rocket. This is a hard gap with no workaround.

Buyers who want a HELOC rather than a lump-sum home equity loan need a different lender. Rocket does not offer HELOCs.

Buyers who prefer sitting across from a loan officer in a physical office will be frustrated. Rocket has no walk-in branches. Everything happens online or by phone.

Buyers purchasing fixer-uppers who need an FHA 203k renovation loan to wrap purchase and renovation costs into one mortgage need to look at loanDepot or another lender that offers this product. Rocket does not.

Before making any final decision, use our DTI calculator to confirm your debt-to-income ratio sits within Rocket’s 50% maximum before you go through the hard credit pull. And run your purchase scenario through our affordability calculator to confirm the price range you are targeting is realistic based on your income, existing debts, and available down payment.

Rocket Mortgage Quick-Reference Summary

Founded: 1985 as Rock Financial, rebranded Rocket Mortgage in 2021. Headquartered in Detroit, Michigan. Licensed in all 50 states and DC. No physical branch locations.

Minimum credit scores: 620 for conventional, 500 to 580 for FHA, 580 for VA, 680 for jumbo, 680 for home equity loans.

Minimum down payments: 1% with ONE+ program, 3% for standard conventional, 3.5% for FHA, 0% for VA.

Origination fee: 0.5% to 1% of the total loan amount.

Rate lock: Free for up to 45 days. Extensions available at 0.25 points per 15-day extension.

Loan types offered: Conventional, FHA, VA, jumbo, home equity loans, bridge loans, cash-out and rate-and-term refinance.

Loan types NOT offered: USDA, HELOC, FHA 203k renovation loans, construction loans.

J.D. Power origination score 2025: Number one ranking in the industry.

J.D. Power servicing score 2025: Number one ranking, 685 out of 1,000 points.

ConsumerAffairs rating: 4.3 out of 5.

BBB rating: A-plus.

Closing time average: 22 days, approximately half the industry average.

: Compare Top Options")

: Compare Top Options")

")